For more than a century, it has been “very unwise” for investors to position themselves against the United States, according to professor Paul Marsh of London Business School. The US is likely to remain dominant in terms of market size in the future, but its outperformance may well be coming to an end, he argues.

Today, US equities account for nearly two thirds of global market capitalization, and the world’s largest bond market sits in the same jurisdiction. Yet structural weight does not guarantee superior returns going forward.

“If you look at the 62 percent share of the global equity market, and then at the closest rivals — with Japan currently the second largest, followed by China and the UK — they are so far behind that American dominance would only be seriously dented if we saw terrible returns from the US and wonderful returns from the rest of the world for the next 10 to 20 years,” Marsh said in answer to a question by Investment Officer.

“If you look at the 62 percent share of the global equity market, and then at the closest rivals — with Japan currently the second largest, followed by China and the UK — they are so far behind that American dominance would only be seriously dented if we saw terrible returns from the US and wonderful returns from the rest of the world for the next 10 to 20 years,” Marsh said in answer to a question by Investment Officer.

Marsh, emeritus professor of finance at London Business School, was speaking on Tuesday at the presentation of the UBS Global Investment Returns Yearbook 2026. His conclusion: the US is likely to remain structurally dominant for a long time. But over the next 20 years, he expects US returns to be broadly in line with the rest of the world. Not lower, but not higher either.

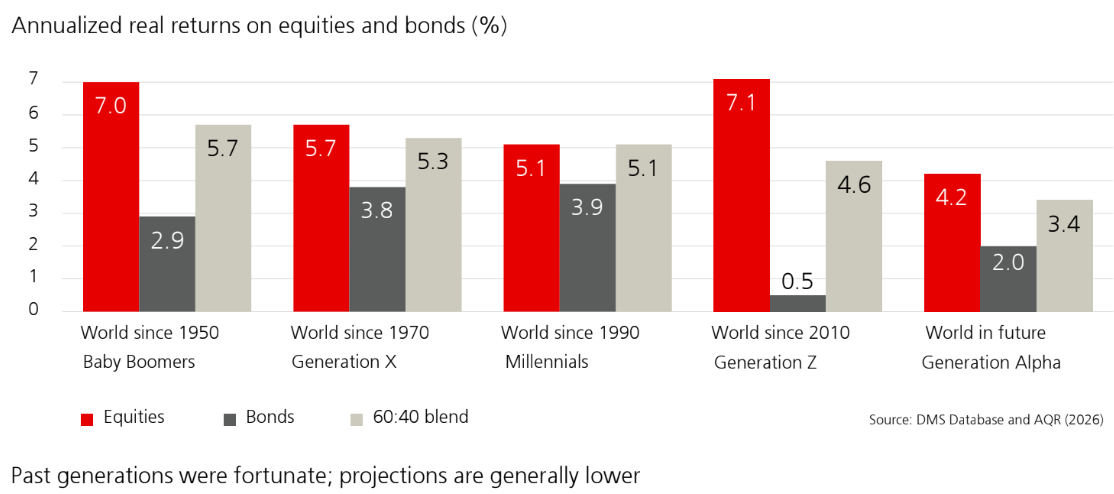

The generational lens makes that shift more tangible. The study picked 1950 for calculating average investment returns for the Baby boomer generation, which amounted to 7.0 percent. Generation X saw 5.7 percent. Millennials, with returns measured since 1990, realized 5.1 percent. Even Generation Z, starting in 2010, has so far enjoyed 7.1 percent, albeit over a short and unusually policy-supported cycle.

Restrained outlook for Generation Alpha

For the next cohort, Generation Alpha, the projection is more restrained: 4.2 percent real returns for global equities, 2.0 percent for bonds and 3.4 percent for a 60:40 portfolio. If that outlook materializes, the investment environment facing this generation will look structurally different from the one that shaped wealth accumulation over the past half century. Compounding will still work, but more slowly, Marsh said. Balanced portfolios would deliver positive real returns, yet likely without the powerful equity tailwinds that defined earlier decades.

Return experience across generations and a projection

Source: UBS Investment Returns Yearbook 2026.

The yearbook, compiled by Marsh together with Mike Staunton of London Business School and Elroy Dimson of Cambridge University, draws on a database stretching back to 1900 and spanning 90 countries. Across 126 years of data, it provides one of the most comprehensive long-run records of financial market performance available to investors.

The historical evidence underscores why US markets command their current position. Since 1900, US equities delivered a 6.6 percent annualized real return, compared with 1.6 percent for bonds and 0.5 percent for Treasury bills.

The dataset also captures episodes of permanent loss. Russia recorded total market wipeouts in 1917 and again in 2022. China did so in 1949 before later re-entering the global index. German bonds were destroyed during the hyperinflation of 1922 to 1923. Long-run investing has rewarded patience, but not without existential risk, it shows.

US outperformance

Against that backdrop, US outperformance stands out. Over the past century, the United States moved from a peripheral market to the central pillar of global capital markets. Strong returns combined with sustained equity issuance lifted its share of global market value, even as its relative share of global GDP declined from mid-century highs.

“In relative return terms, the US has a great deal going for it,” Marsh said. “It has a strong capitalist culture, excellent businesses and many structural advantages. There are good reasons why it has done so well historically.”

“At some point, however, those strengths have to be fully priced into markets. The view my colleagues and I typically take is that markets, on average, get things right.”

“So prospectively, from here on, we would expect US returns over the next 20 years to be broadly similar to returns from the rest of the world. Not lower, as they have been over the last 14 months, nor higher, as they have been over much of history.”

Equities top asset class since 1900

The broader findings of the yearbook show that equities have been the top-performing liquid asset class since 1900. Developed markets outperformed emerging markets over the full period, although emerging markets led during more recent decades.

Inflation remains central to long-run outcomes. US inflation has averaged 2.9 percent per year since 1900, meaning that 1 dollar in 1900 has the purchasing power of 38 dollars today. Equities historically generated positive real returns, while bonds proved more vulnerable during inflationary shocks.

The yearbook also highlights currency exposure as a structural risk factor. Currency movements added roughly 6 percentage points to portfolio volatility on average, with a proportionally greater impact on fixed income portfolios than on equities.