Local currency bonds have lagged this year, but expected interest rate cuts by the Fed have investors in emerging markets hoping for better times.

Investors hope that lower US interest rates, combined with a “soft landing” where the US economy avoids a recession (which would otherwise have dragged down developing countries), will help bring money back into the markets for emerging market debt (EMD).

In such a scenario, central bankers from emerging markets gain more room to cut their own interest rates. Moreover, many emerging markets were quicker to raise interest rates than developed economies when global inflation rose. As a result, they are in a better position now that the Fed is poised to ease monetary policy.

Nevertheless, emerging market debt, expressed in local currencies, has disappointed so far. The Morningstar Emerging Markets (EM) Government Bond Local Currency Index posted a 4 percent return over the first nine months of this year, compared to 5.6 percent for the Morningstar EM Sovereign Bond Index, which tracks emerging market bonds in hard currencies. In the year to August, European investors withdrew nearly 5.5 billion euro from funds in the Morningstar category of global emerging-market bonds in local currencies, while those in hard currencies saw around 1 billion euro in inflows.

While few doubt the attractiveness of valuations within this asset class, country-specific risks continue to concern investors. For example, Brazilian government bonds took a hit due to market concerns over the budget plans of the Lula administration, and Mexican bonds fell after constitutional changes that investors believe could undermine the rule of law.

India

India has overtaken China in the free-float version of the MSCI All-Country World Index, which tracks global equities available for purchase on the open market. The weighting of both countries remains small, at less than 3 percent, and the index is dominated by US equities.

India is also gaining a more prominent position in the bond market. Midway through this year, JPMorgan added Indian government bonds to the widely followed JPM GBI-EM Global Diversified Index. India’s weight in this local currency index will gradually increase by 1 percent per month until it reaches a maximum of 10 percent in April 2025, similar to China, Indonesia, and Mexico.

The inclusion of India has been a topic of discussion among index providers for years. Likely, the exclusion of Russia and Egypt played a role in this decision, according to my colleague Elbie Louw. Active managers initially hoped to benefit from the automatic purchases by passive investors, but managers did not blindly invest in Indian bonds. They remain cautious in assessing India’s interest rate and currency exposure compared to the rest of the investable universe.

Fund Radar

The strategies that prominently appear on Morningstar’s radar are deemed by fund analysts to have a strong management team and a robust investment process, or they receive these qualifications based on an algorithm that assesses investment funds using the same framework. In this article, we highlight an emerging-market local currency bond fund that meets these criteria and where Morningstar analysts maintain confidence despite the challenges of 2023.

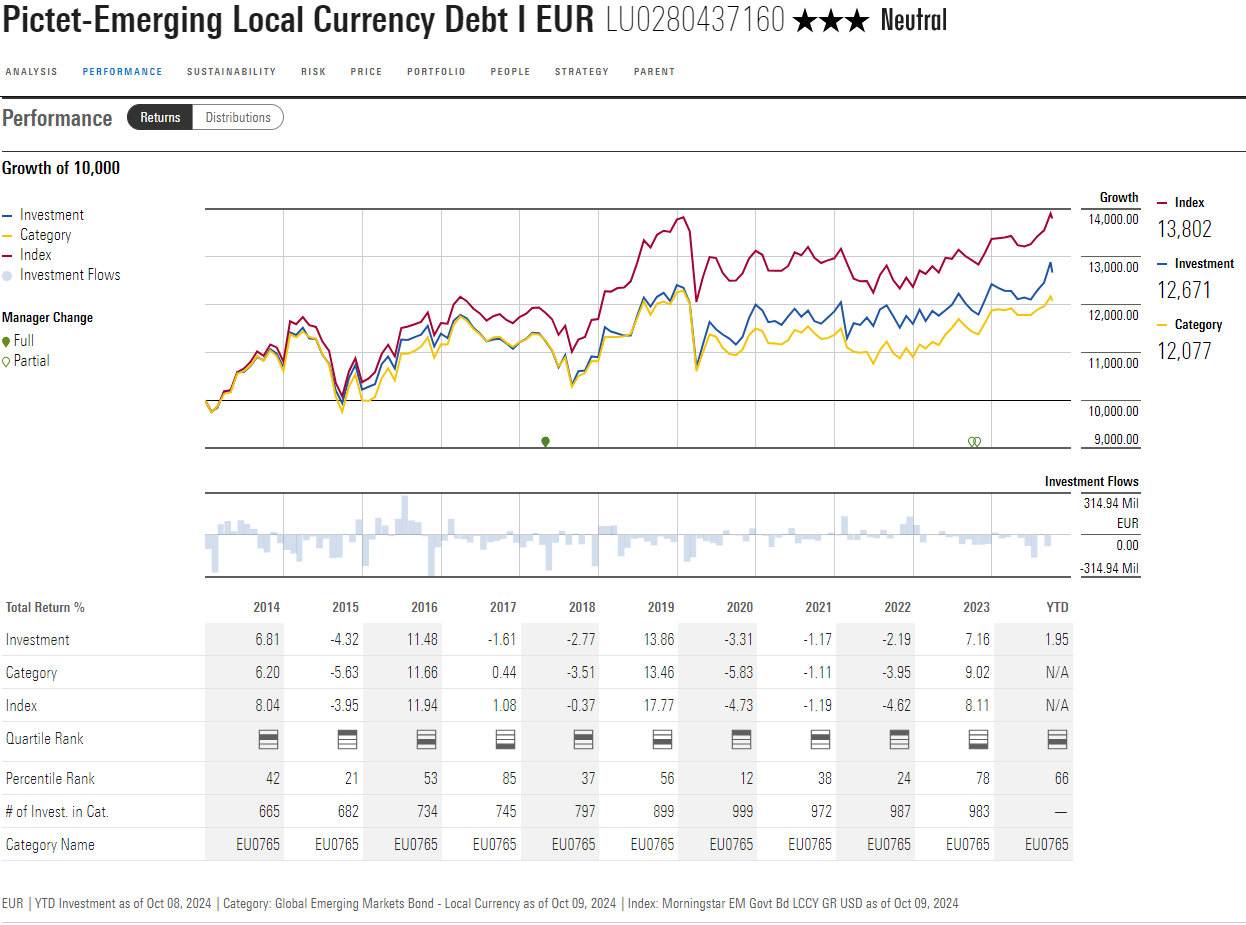

Pictet-Emerging Local Currency Debt is led by Alper Gocer, an EMD veteran with over twenty years of investment experience. In October 2023, Gocer was appointed head of emerging markets debt, succeeding Mary-Thérèse Barton, who was promoted to CIO of fixed income at Pictet. Barton stepped back from her role as co-manager on this strategy, and Adriana Cristea, Carrie Liaw, and Ali Bogra Yigitbasioglu took over her responsibilities. Each has contributed to this strategy over the past five years. Despite recent changes, the stability and expertise of this team warrant an Above Average People rating.

This strategy aims to outperform the JPM GBI Emerging Markets Global Diversified Index benchmark by 1 to 3 percentage points per year and has the flexibility to invest up to 30 percent of the portfolio in securities outside the benchmark (primarily debt and currencies from developed markets). The investment process combines the team’s top-down macro insights with bottom-up views on individual countries.

Performance in 2023 has been disappointing, as the fund was overweight in duration while interest rates continued to rise and the global economy performed better than expected. The long-term track record is more promising, and since Gocer joined in 2018, the fund has navigated various investment environments successfully.

Thomas De Fauw is a manager research analyst at Morningstar. Morningstar analyses and rates investment funds based on quantitative and qualitative research. Morningstar is part of the expert panel of Investment Officer.