Spreads on high-yield bonds are tight, and the fundamentals of high-yield look strong. Taking (credit) risks has clearly paid off this year.

As of the end of September 2024, the Morningstar Global High Yield Bond Index recorded a positive year-to-date return of 7 percent in euros. The asset class remains popular among European investors, mainly due to the attractive initial yields. The ICE BofA Euro High Yield Option-Adjusted Spread, which measures compensation for credit risk in high-yield bonds, has been on a downward trend since October 2023 (493 basis points) when bonds were buoyed by expectations that the Federal Reserve would cut rates in 2024. Another low point was reached in early June (313 basis points), and the spread closed the third quarter at 342 basis points.

In the US, the spread even fell below 300 basis points in October. The effective yield on the ICE BofA US High Yield Index at the end of last month was 6.7 percent, significantly lower than the 9.4 percent at the end of October 2023. The strong market performance was led by lower-rated bonds. The ICE BofA CCC and Lower US High Yield Credit Index posted a return of 12.6 percent in euros over the first nine months of this year.

Optimism prevails

Our discussions with fund managers in the US show that most remain optimistic about the fundamentals of this asset class, but are cautious about the rich valuations and historically low spreads. These tight spreads have been a clear tailwind for returns over the past year, but there is likely little room for further tightening, meaning investors may be relying more on coupons and declining interest rates.

The risk of defaults remains relatively low compared to historical averages. JPMorgan expects default rates of 2 percent and 3 percent in 2024 and 2025, respectively, compared to a 25-year average of 3.4 percent.

Leveraged loan market grows strongly in the US

Another noteworthy trend is the continued popularity of leveraged loans in the US. These loans, like high-yield bonds, are debt instruments with low credit ratings, often issued to finance leveraged buyouts (LBOs). Many of these loans pay a variable interest rate and are managed and structured by financial institutions, often banks.

Since 2014, the leveraged loan market has doubled in size and is now almost equal to the size of the US high-yield bond market, which has stagnated over the same period. This has created two large liquid markets for investors to explore. The high-yield market is now made up of more than half BB-rated credits, the highest within high-yield bonds, whereas in 2007 this figure was below 40 percent. The US leveraged loan market, on the other hand, is riskier, with about two-thirds of its credits rated B.

Fund Radar

The strategies that prominently appear on Morningstar’s radar are those that fund analysts believe have strong management teams and robust investment processes, or which are attributed these qualities based on an algorithm that evaluates funds under the same framework. In this article, we highlight an actively managed high-yield fund that meets these criteria and in which Morningstar analysts have high conviction.

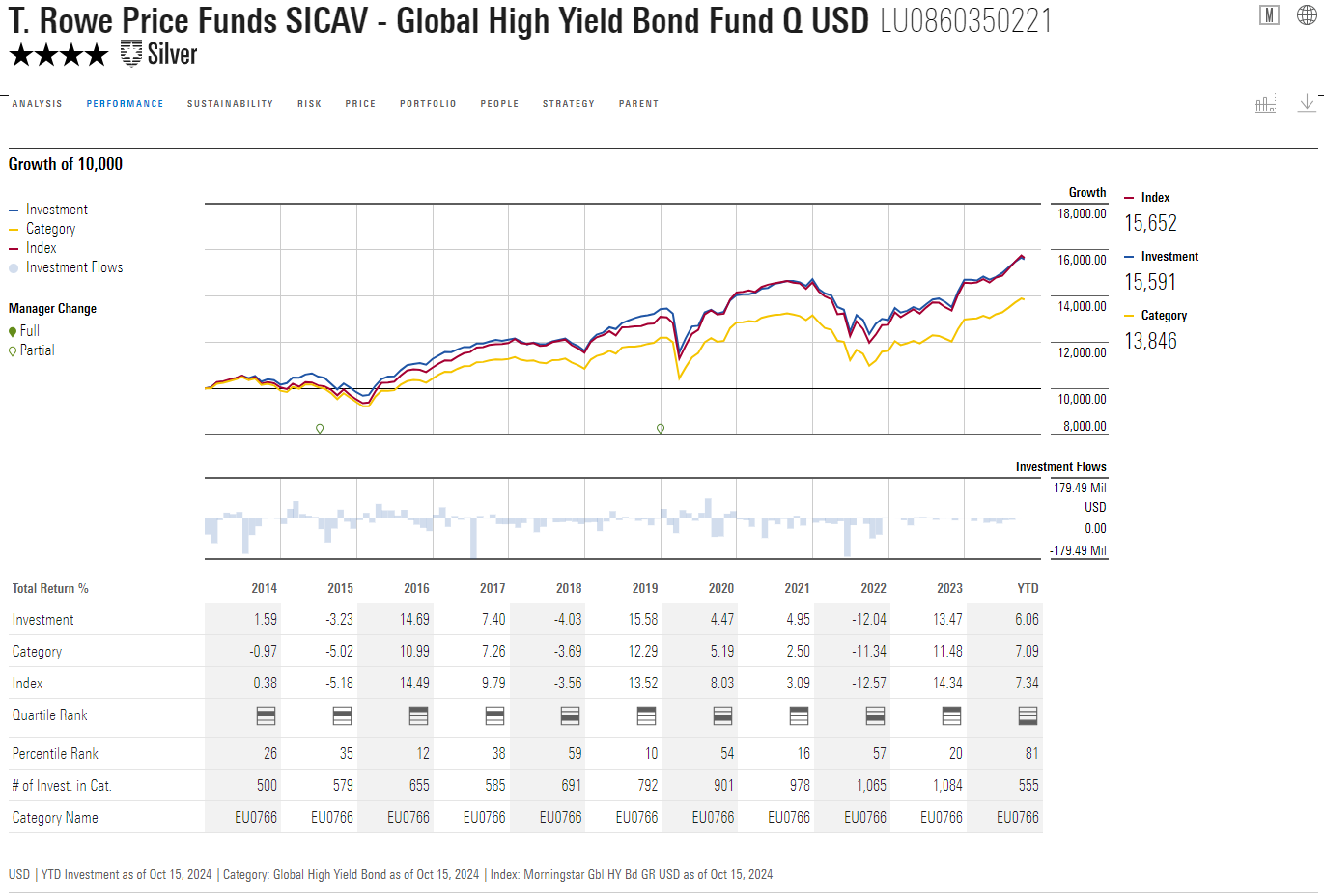

The strong credit team and consistent process make the T. Rowe Price Global High Yield Bond an attractive option for investors seeking exposure to global high-yield bonds. Morningstar analysts rate the fund as Above Average for People and Process.

Michael Della Vedova and Rodney Rayburn have led this strategy since 2015 and 2019, respectively. While Rayburn has limited experience managing a high-yield strategy, his background in distressed companies and special situations, along with the approach and quality of the broader team, gives us confidence. Della Vedova joined T. Rowe Price in 2009 and has managed the European high-yield strategy since September 2011. The two managers are well supported by an additional six high-yield portfolio managers and eighteen dedicated credit analysts.

The strategy combines credit selection with top-down macro analysis, with the fund’s strength lying in its bottom-up security selection. The managers draw on issuer and sector ideas from the analyst team to shape the portfolio. A typical feature of this strategy is an overweight in high-yield issuers with BB and B ratings, while non-US high-yield bonds have periodically accounted for a third of assets since 2015. Unlike many global high-yield peers, the fund can invest in equities, although historically these have accounted for only a few percent of assets.

The strategy has a solid long-term track record compared to its rivals, thanks to its positive credit selection.

Thomas De Fauw is a manager research analyst at Morningstar. Morningstar analyses and rates investment funds based on quantitative and qualitative research. Morningstar is part of the expert panel at Investment Officer.