By AXA IM Senior Investment Analyst, William Mahoney

The unprecedented monetary and fiscal stimulus put in place by governments and policymakers worldwide has supported bond markets for much of 2020 and 2021, but fixed income investors have faced challenging, volatile times nonetheless.

We have previously identified that within equities, removing stocks with poor performance around environmental, social and governance (ESG) factors delivered a markedly better performance than the benchmark index in 2020.

Our research also suggests that ESG screening may be able to help provide a buffer for fixed income portfolios and could add significant downside risk protection for returns. Importantly, it also appears that applying such screening – as investors increasingly want to invest responsibly alongside their financial objectives – does not impact the potential ability for fixed income portfolios to outperform the broader market.

Our analysis of the ICE BofA Global Corporate Index in 2020 found that excluding bond issuers with a poor ESG profile allowed a simulated portfolio to perform in line with the market, while a simulated portfolio consisting purely of ESG leaders – bond issuers with the best ESG profiles, according to our methodology outlined below – outperformed the market by 65 basis points (bps) over the year.

Below, we outline how our findings suggested that ESG-focused investors, on average, may have been able to cushion their portfolios from downside risk and generate higher returns during a tumultuous year.

Excluding poor ESG performers appeared to mitigate downside risk

At AXA IM we employ a screening policy across the vast majority of our assets under management and exclude companies that fall into certain categories. In our view, a key part of responsible investing is avoiding issuers with high ESG-related risks.

These include controversial weapons, climate risk, ecosystem protection and deforestation, as well as soft commodities, where we aim to avoid short-term financial instruments which may contribute to price inflation in staples such as wheat, rice, or soy. We call these our Sectorial policies.

In addition, our ESG Standards policy has additional exclusions based on severe controversies, white phosphorous, tobacco and low ESG quality.

Alongside these exclusions, we also applied our proprietary ESG scoring methodology to the ICE BofA Global Corporate Index (G0BC) and removed securities that scored below two out of 10. Overall, these actions removed approximately 7% of the benchmark universe.

We assessed performance on a month-by-month basis using excess returns data at security level, as well as monthly rebalancing at sector level to ensure that weight, spread duration and average spread of each allocation closely matched that of the market, to remove credit beta bias.

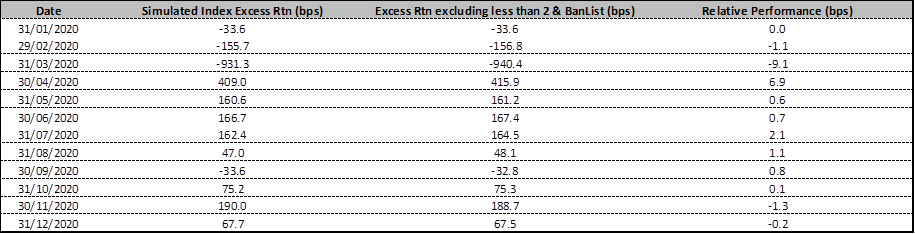

Our analysis found that the performance of this simulated portfolio throughout 2020 was closely aligned to that of the benchmark universe, with less than one basis point difference in return profile over the full year (see Exhibit 1). The largest monthly difference of 9bps was in March 2020 – a particularly challenging month for fixed income, when the 10-year US Treasury yield hit a record low and the Federal Reserve slashed US interest rates and announced a series of emerging lending programmes to buy corporate debt.

Exhibit 1: Eligible universe returns versus ICE BofA Global Corporate Index over one year

(Source: Bloomberg/ICE data in US dollar terms)

(Source: Bloomberg/ICE data in US dollar terms)

ESG leaders outperformed significantly

We then looked to ESG leaders. We took the ICE BofA Global Corporate Index as before, applied our AXA IM Exclusions and Standards policies and filtered for securities scoring seven or higher according to our ESG Scoring methodology. This removed about 75% of the benchmark universe, leaving only the issuers that we would consider leaders in responsible investing.

Once again, we assessed performance on a month-by-month basis using excess returns data at security level. We rebalanced portfolios monthly at sector level, ensuring that weight, spread duration and average spread of each allocation were tilted to align with the benchmark as closely as was reasonably possible, with spread duration typically +/-0.1 years and average spread +/- 5bps. For certain sectors – notably autos and leisure, given the limited number of securities in scope – the thresholds were larger. The overall portfolio spread duration and average spread were again closely matched at +/- 0.05 years and +/-0.5bps.

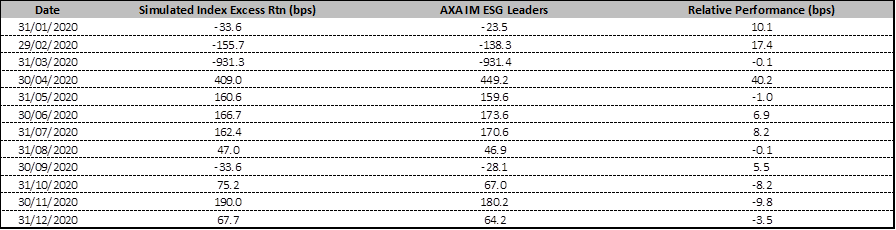

Our analysis of 2020 showed that the simulated portfolio outperformed the benchmark by 65bps over the year, with the greatest monthly outperformance in April when bond markets recovered following central bank intervention.

Exhibit 2: ESG leaders returns versus ICE BofA Global Corporate Index over one year

(Source: Bloomberg/ICE data in US dollar terms)

(Source: Bloomberg/ICE data in US dollar terms)

Addressing global challenges while aiming to create sustainable value

While effort was made to remove the embedded biases within our scoring methodology, it is still possible that the process used to align sector profiles meant that we tilted our portfolios to longer-dated, high-spread names to compensate for the excluded credit beta; and with the credit curve flattening through 2020, longer-dated names would be expected to outperform.

It may also be the case that high ESG scores act in part as a signal of strong management and effective long-term strategy, as much as they do for ESG quality.

While this data shows performance in 2020, no two years are the same, and past performance should never be used as an indicator of future returns. From analysing the excess performance of the universe after exclusions, compared to the benchmark, we can conclude that applying ESG and responsible investing screening to our portfolios does not appear to impact the ability to outperform the broader market, and at the same time could add significant protection against ESG and responsible investing related risks.

Fundamentally, we believe ESG analysis in fixed income as well as equities – and using this analysis in our investment process and decisions – can not only allow clients to align their portfolios with investment solutions that address global challenges, but also aim to create sustainable value for investors.

|

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. |

|

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision. |

|

The ESG data used in the investment process are based on ESG methodologies which rely in part on third party data, and in some cases are internally developed. They are subjective and may change over time. Despite several initiatives, the lack of harmonised definitions can make ESG criteria heterogeneous. As such, the different investment strategies that use ESG criteria and ESG reporting are difficult to compare with each other. Strategies that incorporate ESG criteria and those that incorporate sustainable development criteria may use ESG data that appear similar but which should be distinguished because their calculation method may be different. |

|

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ |