The euro saw a 20-year low against the US dollar in 2022. With the ECB catching up with the Federal Reserve, investors are counting on a comeback for the European currency. Currency specialists, however, are divided.

Unprecedented inflation levels steered central banks towards unprecedented rate hikes last year, with the Federal Reserve leading the way. The US central bank’s lead in interest rate policy pushed the euro below the dollar in 2022 for the first time in 20 years. A painful twist for investors with exposure to the European currency.

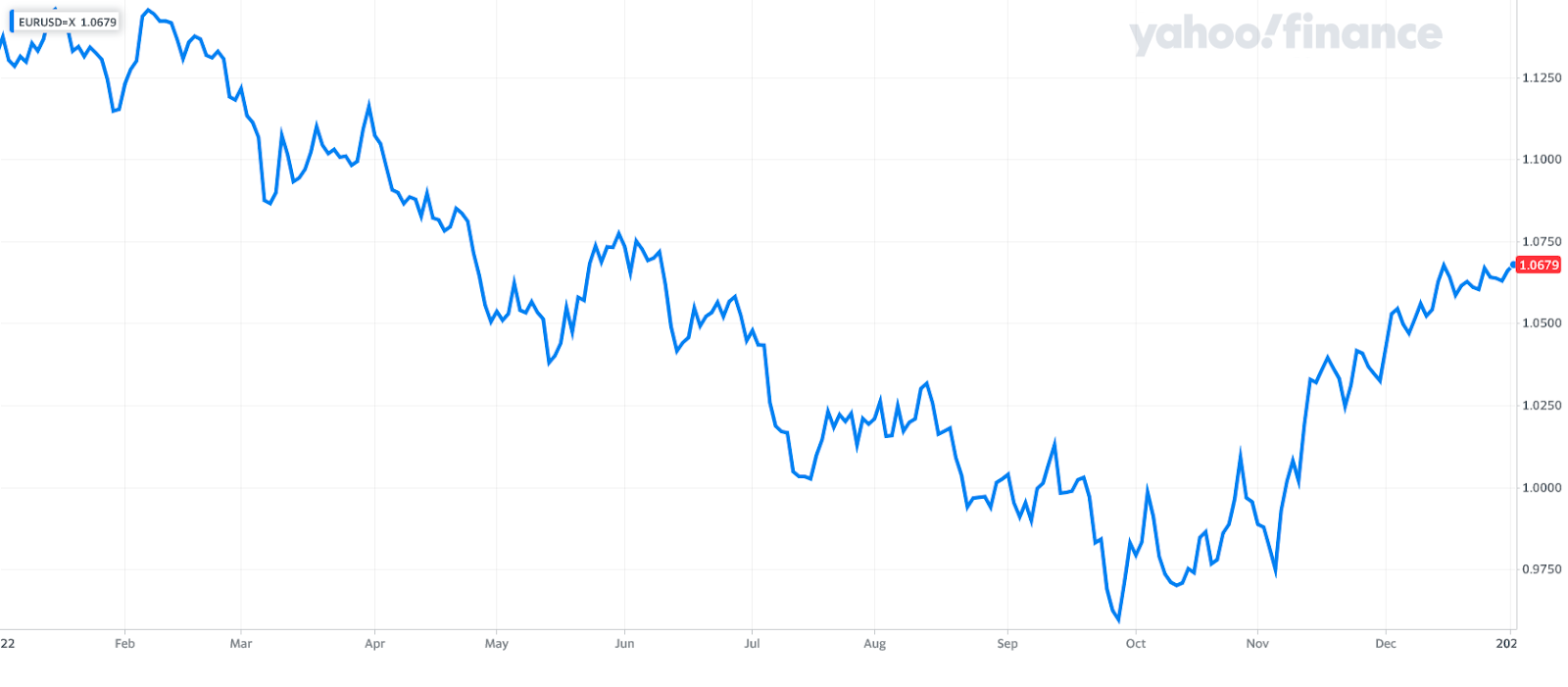

With the market starting to bet on a Fed pivot, and the European Central Bank indicating it is “far from finished” with raising interest rates, the end of the euro malaise appears to be over. The euro recovered from a 2022 low of $0.95358, closing the year at $1.06994. The euro eventually lost of 6.1 per cent from a year ago.

Euro vs dollar during 2022

According to Societe Generale SA strategist Kit Juckes, the dollar sell-off “was mainly generated by a sense of optimism that the world is healing,” he said in a note to clients. The euro’s rise further indicates investors’ confidence in the eurozone’s resilience as the energy crisis appears to be not too bad for now. However, currency strategists are not quite buying into that optimism yet.

A survey by Bank of America Global Research shows that a record number of fund managers think the dollar is overvalued. “Inflation, the US dollar and Fed hawkishness will all peak in the first half of 2023,” the bank said. However, Reuters polls among 66 currency strategists in December suggested that the dollar will maintain its current level for about a year.

According to the news agency, many currency strategists expect the tightening of global central banks’ monetary policies to hurt growth and reinforce the dollar’s safe-haven appeal once again.

Job market ‘stubbornly tight’

According to Thomas De Caluwé, currency analyst at Argentex, things are slowly starting to look good for the euro, but he, like Juckes, warns of a major factor that could throw a spanner in the works for the euro-dollar recovery: a US economic recession.

Currency movements are closely related to inflation levels. In all Western economies, inflation fell during the last quarter of 2022. With this, the Fed’s and ECB’s initiated path seems to be effective. The effect was particularly noticeable in America, with price pressures easing to 7.1 per cent in November, the lowest point of the year. Falling inflation is leading to the end of the strong dollar for now, sending the euro towards a remarkable recovery.

Argentex’s De Caluwé is cautiously optimistic, but argues that the jobs market remains “stubbornly tight”, putting upward pressure on salaries. “Analysts expect average hourly wages to have increased by 5 per cent in the month of December, which obviously does not square with the inflation target of 2 per cent,” he said.

“What exactly the Fed committee members think about this, we may find out on Wednesday. This is because that is when the minutes of the previous meeting will be released. These may give more guidance on what impact the waning price pressures will have on future policy. If it continues to drag on, the market’s focus is likely to start turning to interest rate cuts, and the question of ‘when and by how much’ will become the main dollar driver.”

ECB only halfway done

Meanwhile, price pressure in the Eurozone is also clearly easing. De Caluwé expects the December data to show an inflation rate below 10 per cent. That would be the first time since October.

‘This does not alter the fact that price pressures for certain individual eurozone countries (such as Italy and Germany) are at alarmingly high levels. Unemployment figures and export data from Germany this week give an insight into the health of Europe’s largest economy,’ says De Caluwé.

He finds it striking that although the European Central Bank preached throughout 2022 that interest rates would not climb higher than around 2.5 per cent because of a deteriorating economic outlook, the bank seems to be tightening harder at the last minute.

ECB President Christine Lagarde, in her last speech of the year, indicated that the ECB is behind the Fed, “and there is a lot of catching up to do”, even if this would mean continuing to raise interest rates during a recession, says De Caluwé. Klaas Knot told journalists at the Financial Times last week that the ECB thinks it has only just reached the halfway point of its tightening cycle and that it is still a “long game”