Flexible allocation funds typically have broad latitude to adjust their asset allocation. Additionally, their managers have the freedom to add alternative asset classes to the mix, with gold being a well-known option.

Although the traditional mix of equities and bonds remains a solid foundation, interest in (small) allocations to real assets, currencies, and derivatives is steadily growing. Less liquid assets such as infrastructure are also gaining popularity. Moreover, dynamic and sometimes complex allocation strategies are drawing attention from investors. However, it’s worth noting that market timing remains a refined art mastered by few.

Morningstar’s flexible allocation category includes a diverse group of funds that have a largely unrestricted mandate to invest in various asset types. These strategies often allow more leeway to adjust weightings toward equities, bonds, and alternatives, and they utilise tactical allocation and derivatives.

Insurance or relic?

Among non-traditional asset classes, gold has long been an essential component of diversified portfolios. A prime example of this is the permanent portfolio, which encourages American investors to allocate a quarter of their portfolio to US equities, US government bonds, cash, and gold.

While not every fund manager embraces the precious metal, some advocate for it fervently. Proponents view gold as a valuable differentiator and a means of portfolio protection. Critics, on the other hand, argue that gold does not generate cash flow, is volatile, and represents a relic from bygone times.

Gold in a bull market

The gold price, quoted in US dollars per ounce, stood around 2,780 on Thursday morning, marking an increase of nearly 35 percent since the end of last year. This rise is remarkable, especially given the recent limited interest in gold ETFs and the weak performance of gold mining companies.

A key driver behind this rally appears to be the demand for physical gold by central banks in emerging markets. Sanctions against Russia and its oligarchs due to the war in Ukraine have led many parties to rethink the composition of their reserves. Gold has functioned as a store of value for hundreds of years and can also be held outside the financial system.

In BRICS countries, there is a noticeable shift from purchasing US dollar government bonds to buying gold by central banks. While this doesn’t directly threaten the dollar’s status as a reserve currency, such small shifts can impact the gold price itself.

Fund Radar

The strategies prominently featured on Morningstar’s radar are rated highly by the fund analysts for strong management teams and robust investment processes, or they receive these qualifications based on an algorithm that assesses funds within the same framework. In this article, we spotlight an allocation fund that maximises the use of its flexible mandate with an above-average exposure to gold.

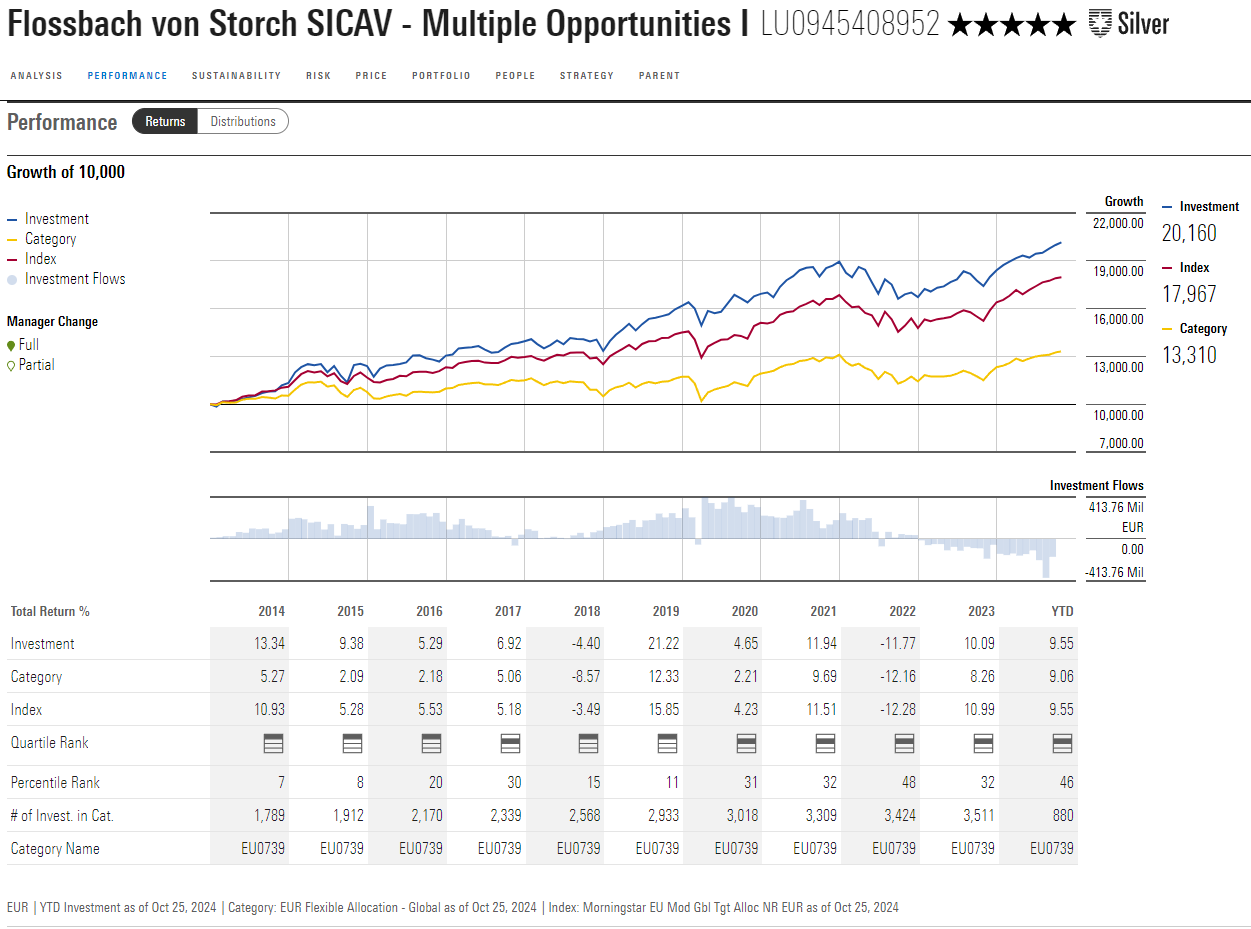

FvS SICAV Multiple Opportunities follows a flexible approach, grounded in thorough fundamental research. Morningstar analysts award it a Process rating of High and a People rating of Above Average.

Bert Flossbach and Kurt von Storch founded Flossbach von Storch (FvS) in Cologne in 1998. Since the launch of this strategy in October 2007, Flossbach has remained at the helm. He collaborates with other experienced investors who form the firm’s strategy team, developing the house vision and framework for the top-down positioning of the strategy. Bottom-up security analysis is conducted by the broader investment team, which has been expanded over the years to accommodate asset growth.

The manager can invest in equities, bonds, convertible bonds, precious metals (primarily gold), and cash. The allocation fund has significant leeway to adjust its equity allocation, with a wide range of 25 percent to 100 percent. The equity exposure dropped to 29 percent during the coronavirus-induced sell-off in March 2020, while it peaked at 82 percent in 2021. As of the end of September, the allocation stood at around 68 percent, with a focus on mega-cap stocks. When the fund was smaller, small caps had a greater impact. The equity portfolio is rooted in quality stocks, but the manager is willing to accept lower quality if there is strong valuation support.

The fund invests a maximum of 25 percent in gold, directly or indirectly via exchange-traded products. Exposure averaged 10.5 percent, recently around 12 percent, significantly higher than the 2-3 percent tactical allocation seen in other mixed funds.

Since its inception, the strategy has demonstrated a strong track record by losing less than its peers in down markets and generating strong returns in rising markets. This success is largely due to the above-average equity exposure (a historical average of 64 percent compared to 43 percent for the Morningstar EUR flexible allocation category). The fund also outperformed the category index, a feat that many of its peers have struggled to achieve.

Thomas De Fauw is a manager research analyst at Morningstar. Morningstar analyses and rates investment funds based on quantitative and qualitative research. Morningstar is part of the expert panel of Investment Officer.