The first quarter of 2026 was marked by a sudden shift in market sentiment. After a start to the year driven by geographical and sectoral reallocations that continued to favour risky assets, March saw the markets shift towards an environment dominated by energy, geopolitics and a reassessment of inflationary risks.

In January and February, the momentum remained positive. Capital flows shifted towards emerging markets, Europe, Japan and, more broadly, developed markets outside the US, against a backdrop of growing doubts about the artificial intelligence cycle, a weakening dollar and political uncertainty in the US. However, this situation was undermined towards the end of the period by rising tensions in the Middle East, which gradually reignited risk aversion and geopolitical premiums.

The tipping point came in March with a major external shock: the blockade of the Strait of Hormuz. The event abruptly reshuffled the deck in the energy market and, by extension, in expectations regarding inflation and monetary policy. The price of Brent crude rose by 63.3% over the month to reach $102.50 at the end of March, a movement of historic proportions. In response, interest rate expectations were significantly revised: the consensus shifted from a scenario of monetary easing at the start of the year to expectations of two to three rate hikes by the ECB, and from zero to one hike by the Fed. This shift in policy led to a rise in volatility, tightening of long-term rates and a general repricing of risk. The 10-year Bund and Treasury yields have risen sharply (Bund ~3.1%; US 10-year ~4.3% at the end of March¹), whilst the dollar has regained its status as a safe-haven asset. A notable feature of this period of stress: gold has fallen since early March, weighed down by the strength of the dollar and by technical selling aimed at covering other losses. China, which has remained relatively low-key since the outbreak of the conflict, appears to be coming out on top for the time being, whilst the United States faces growing discredit, with the Middle Kingdom emerging as a pole of relative stability on the international stage.

Against this backdrop, equity markets ended the quarter down. At the end of March, the MSCI ACWI was down 3.2% year-to-date, a trend shared across the major regions. Europe fell by 4.6% (Euro Stoxx 50), weighed down by a sharp decline in March, whilst the United States fell by 4.4% (S&P 500)1. Emerging markets also corrected towards the end of the period, but remained close to break-even for the quarter (0.5% for the MSCI Emerging Markets)¹.

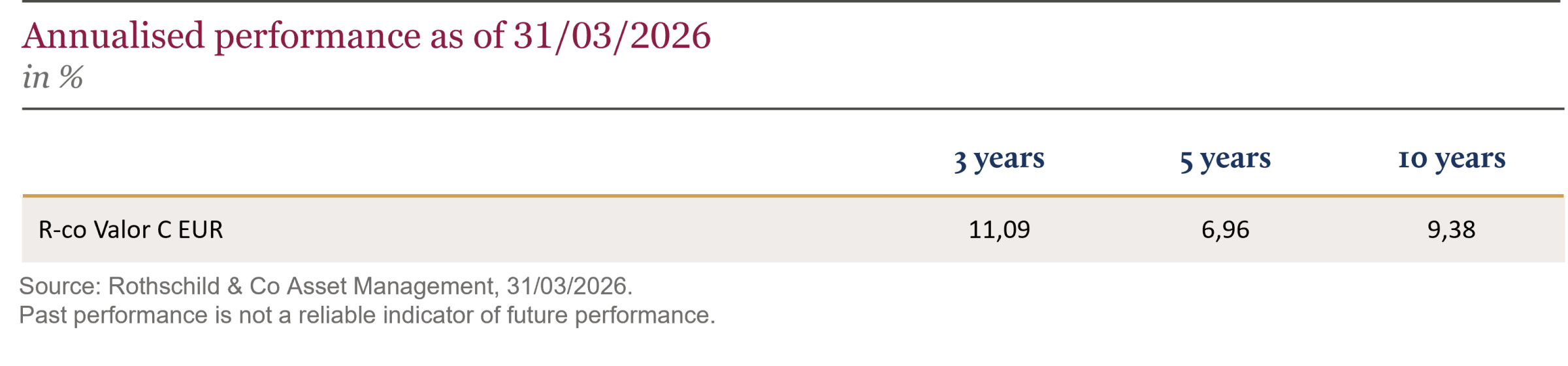

R-co Valor fell by 4.3% over the quarter (Class C EUR shares). The period unfolded in two phases: a fairly positive start to the year, followed by the March correction, which was exacerbated by particularly sharp sector rotations. Over the period as a whole, technology and luxury goods were the main drag on performance. Technology suffered mainly due to its emerging-market component, whilst luxury was penalised by LVMH and Richemont, against a backdrop of deteriorating global demand prospects. Geographically, Asia ex-Japan was the worst-performing region. Conversely, commodities, driven by mining and energy, supported performance, against a backdrop of more favourable metal and energy prices. Industrials, particularly North American ones, also stood out, with companies such as Honeywell and Bombardier leading the way.

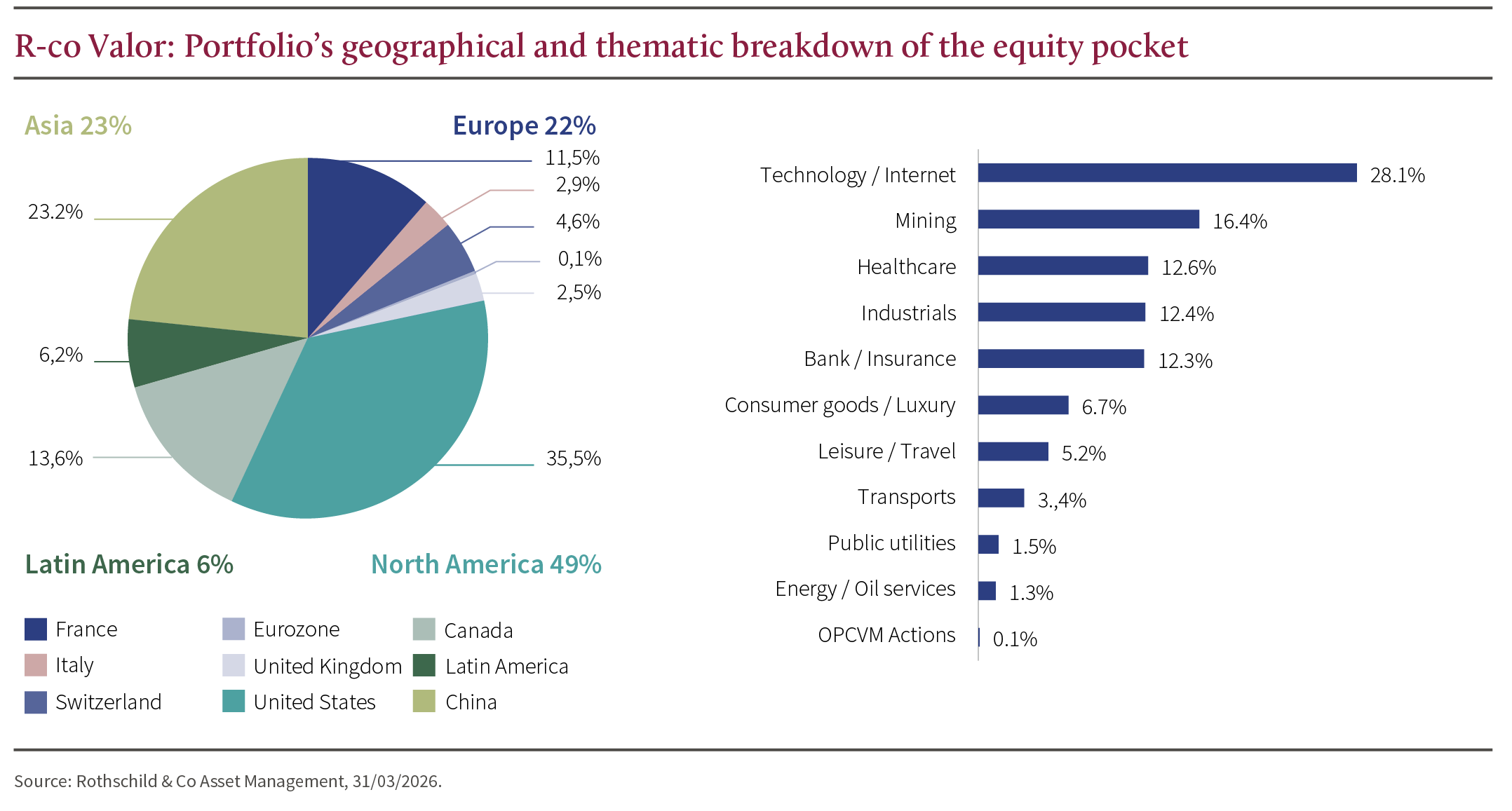

R-co Valor

R-co Valor’s equity exposure was increased during the quarter, from 72% at the start of January to 76%(2). This shift was achieved in two ways: 1/ through active management of existing positions. Exposure was increased in companies deemed to be oversold, particularly in Europe, with purchases made in Capgemini, Richemont, LVMH and Ferrari. Several positions were also increased in emerging markets, notably Grab, Alibaba, Kingdee, MercadoLibre, Tencent and Xiaomi. Adjustments were also made in North America within the healthcare sector with Thermo Fisher, Medtronic and BioMarin, as well as in the copper sector via Ivanhoe Mines and Freeport McMoRan. The latter two had been partially reduced in the first half of the year. 2/ by adding new companies to the portfolio. Lonza, a Swiss CDMO (Contract Development and Manufacturing Organisation) in the healthcare sector, was added to the portfolio to capitalise on the sector’s growth and the increasing trend towards outsourcing pharmaceutical production. A new position in the gold sector was also established via NovaGold, a developer of a mining project in Alaska. Finally, HDFC Bank, a leading Indian bank, was added to strengthen exposure to emerging markets, against a backdrop of valuations in India becoming attractive once again. At the same time, some positions were reduced, mainly with a view to taking profits. A number of mining stocks were therefore reduced at the start of the year, notably Newmont and Ivanhoe, as well as certain healthcare stocks such as Pfizer and Roche. More broadly, exposure to North American companies was adjusted, with reductions in Morgan Stanley, Bombardier and AES.

The portion not invested in equities remained allocated to money market instruments, comprising money market funds and European government bonds with maturities of less than one year.

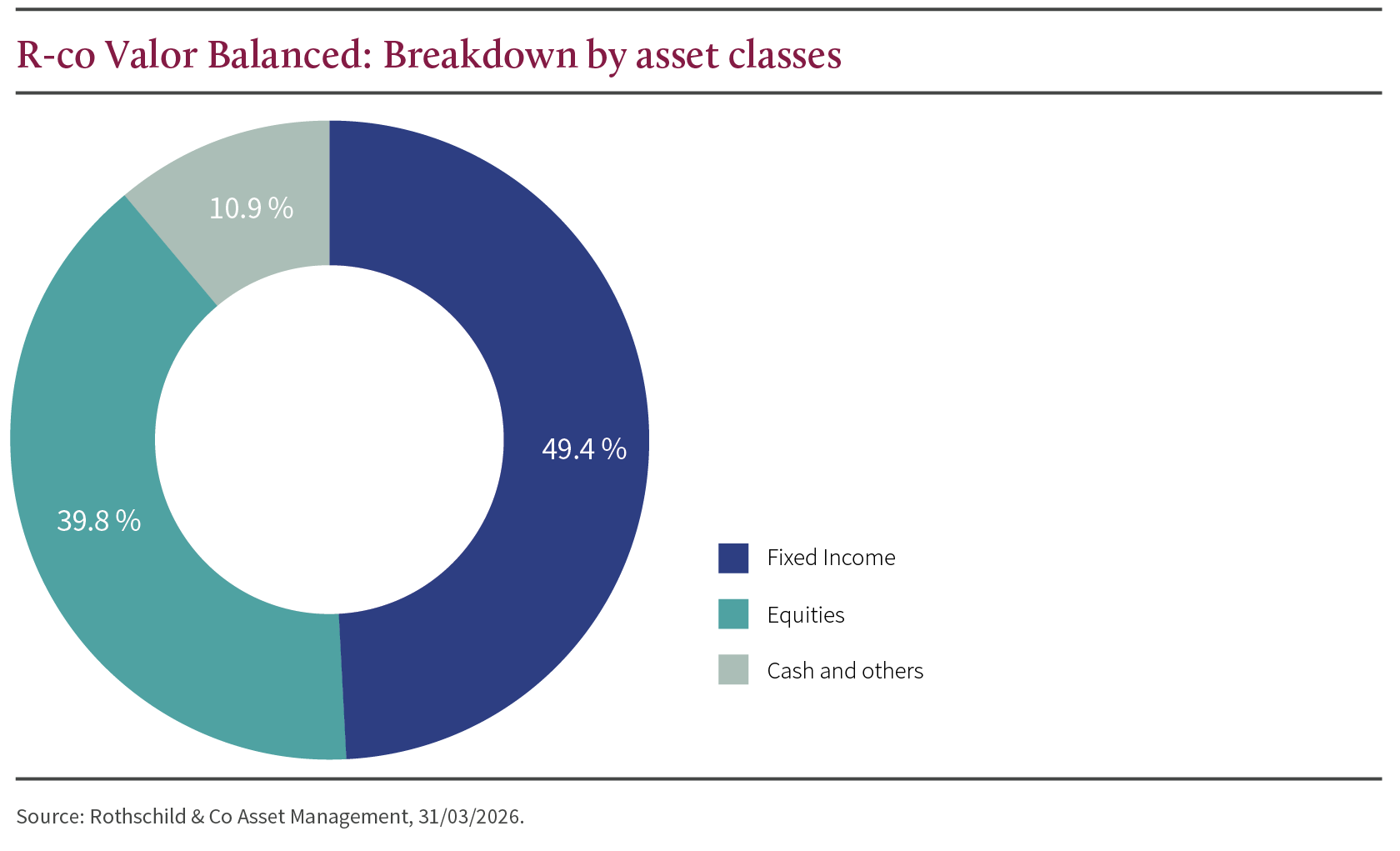

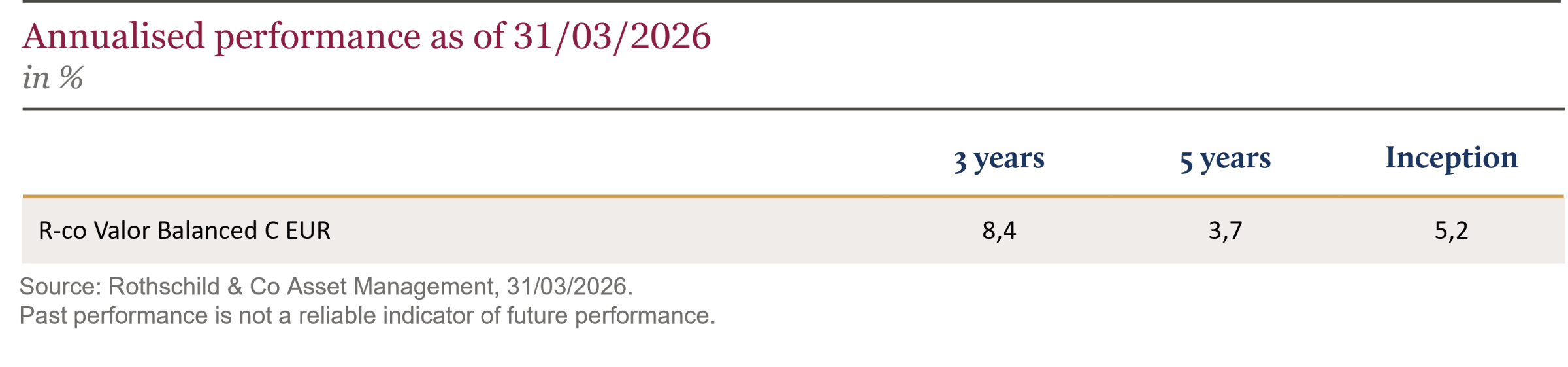

R-co Valor Balanced

R-co Valor Balanced has a 40% equity exposure, with bonds accounting for 49% of the portfolio, and the remainder invested in money market instruments and similar assets (2). The fund is down 2.8% year-to-date (Class C EUR), driven mainly by its equity component, but also, to a lesser extent, by its bond component (2).

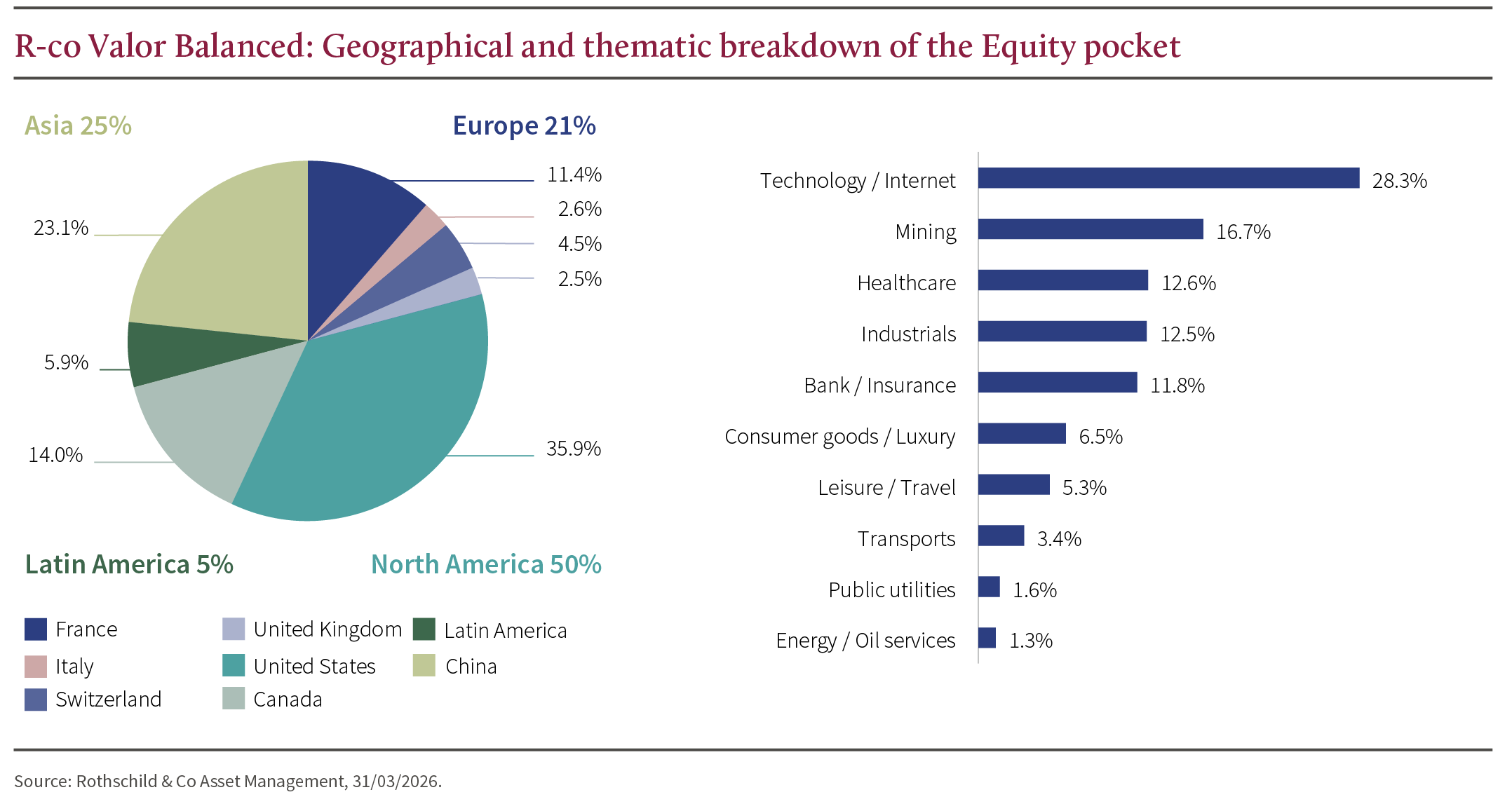

Equity Pocket

The equity allocation of R-co Valor Balanced mirrors that of R-co Valor. The adjustments made and the positioning are identical

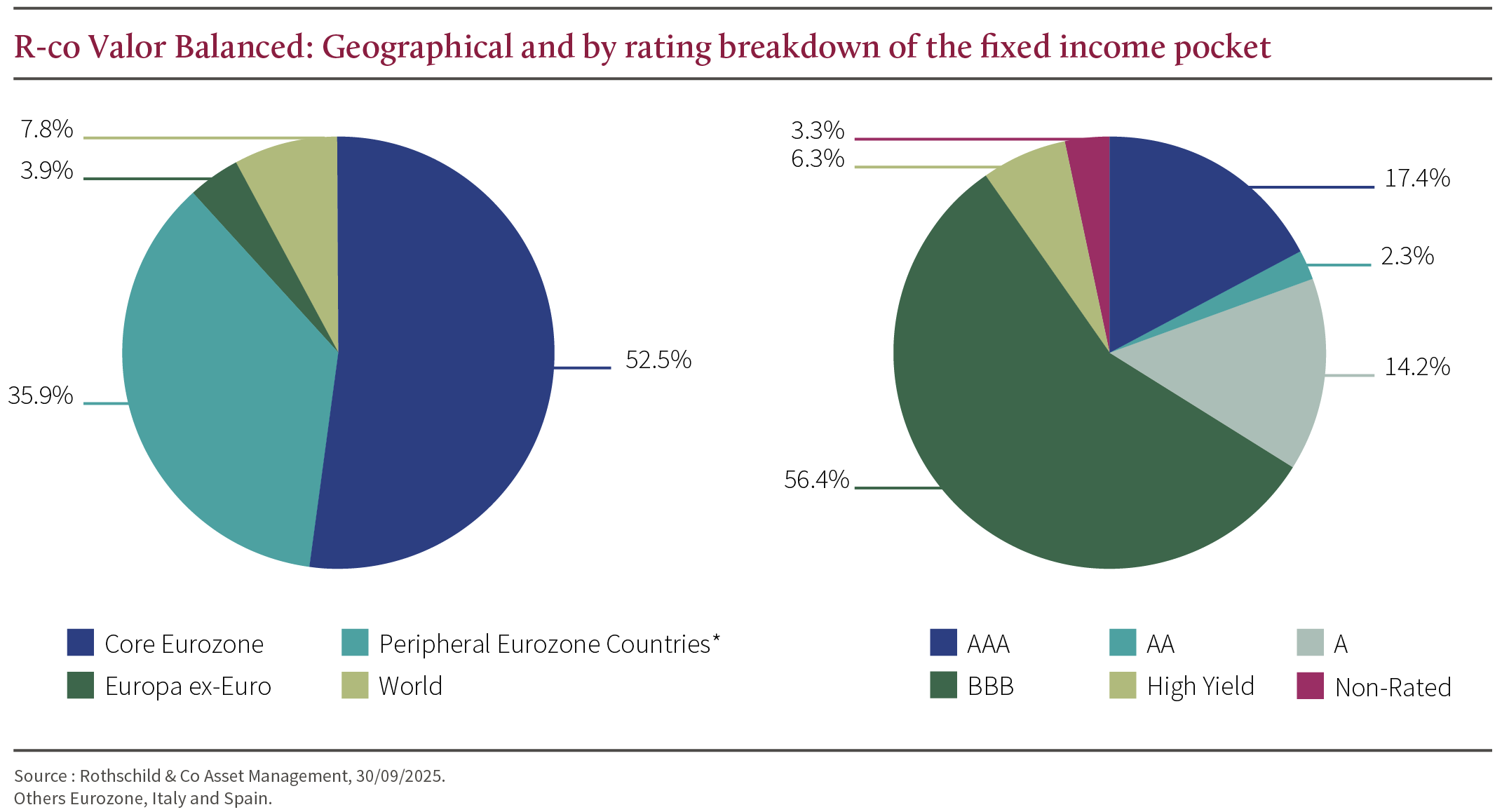

Fixed Income pocket

Throughout the quarter, the fixed-income markets were characterised by high volatility, alternating between upward pressure driven by inflation expectations and flight-to-safety movements, before ending March with a sharp rise in yields in both the United States and Europe. Government bond yields thus rose sharply throughout March, led by short-term maturities, as investors significantly scaled back their expectations of short-term rate cuts. Ten-year government bond yields also rose sharply in the US and Germany. The Bund reached its highest level since 2011 at 3.1% at the end of March, whilst the US 10-year yield ended the month at 4.3% (1). Against this backdrop, euro-denominated credit markets experienced a correction over the quarter, with a negative return of 1% for Investment Grade (3) and 1.7% (1) for High Yield (4).

Within the bond portfolio of R-co Valor Balanced, exposure has been increased to 49%². Over the first two months, the fund took advantage of a particularly active period in terms of new issues to establish a position in the primary market. Financial securities were therefore favoured. Certain segments of high-quality European credit, particularly financial subordinated debt, continue to offer attractive entry points, supported by solid fundamentals and a significant strengthening of capital. In March, primary market activity contracted sharply, with financial issuance in Europe hitting a six-year low, reflecting risk aversion linked to geopolitical tensions in the Middle East. Within the fund, new positions were therefore mainly established in the secondary market and, here too, primarily involved investment-grade financial bonds offering attractive carry. The fund’s sensitivity was increased to 4.72, mainly through positions in futures on the Schatz (2-year German government bond), one of the segments of the yield curve that moved the most over the period. This approach allowed for a rapid adjustment of sensitivity without drawing on the liquidity buffer and without increasing credit risk.

Outlook

The lesson of the quarter is clear: when energy and geopolitics take centre stage, macroeconomic visibility deteriorates rapidly. March marked a turning point, putting not only the equity markets but, above all, the prevailing macroeconomic assumptions to the test. The expected slowdown in inflation and the scenario of monetary easing, which were widely accepted at the start of the year, were called into question within a matter of days. For the coming months, three variables deserve particular attention. Firstly, the transmission of the energy shock (inflation, margins, consumption) and its potential to spread beyond oil. Secondly, the reaction of central banks, whose flexibility is once again key in a world where supply shocks may resurface. Finally, the earnings season, which continues to provide a stabilising influence as long as it confirms the strength of fundamentals, even in an environment of tighter costs and interest rates. Consensus expectations are also particularly high in the United States, with expected earnings growth of +17% for 2026 (1).

Visibility remains limited for all market participants. Against this backdrop, our approach is based on a proven discipline, a clear framework and the ability to act when the markets offer genuine entry points. The conflict has not led to any disruption in asset allocation, as our approach remains firmly focused on the long term. The moves made are primarily aimed at reinforcing convictions that have come under pressure, particularly in emerging markets and in high-quality companies in Europe. It now appears appropriate to resume buying in certain segments where profit-taking had taken place a few weeks earlier. In a market dominated by emotion and volatility, the objective remains to maintain a rational view of the cycle and to invest when the correction is likely to create value.

For more information, visit Rothschild & Co AM website.

(1) Source: Bloomberg, 31 March 2026.

(2) Source: Rothschild & Co Asset Management, 31 March 2026.

(3) Debt securities issued by companies or governments with a credit rating between AAA and BBB- on the Standard & Poor’s scale.

(4) High-yield bonds are issued by companies or governments with a high credit risk. Their credit rating is below BBB- on the Standard & Poor’s scale.