Pharmaceutical companies were once known for their strong growth potential, but slowing revenue growth, lower valuations, and higher dividend yields have given them a more mixed profile in recent years. However, over the past three years, Novo Nordisk and Eli Lilly have stood out by reclaiming their growth status.

The Morningstar Pharmaceuticals and Healthcare Equity category includes various industry groups such as biotechnology firms, healthcare insurance providers, and medical equipment manufacturers. However, pharmaceutical companies dominate, accounting for 42 percent of the Morningstar Global Health Index as of the end of August 2024.

A decade ago, the industry was considered a growth sector, with pharmaceutical companies typically experiencing above-average revenue growth and enjoying high profit margins, leading to correspondingly high stock valuations. The Morningstar Global Health Index was consistently classified in the growth column of the Morningstar Style Box. But since 2014, this has gradually changed. While profit margins remained relatively stable, many companies faced slowing revenue growth, largely due to a decline in the introduction of new medicines.

This put pressure on valuations. However, cash flows from existing products continued to flow, allowing most pharmaceutical companies to offer attractive dividends of 3 percent to 5 percent. As a result, the sector increasingly lost its growth profile, pushing the healthcare index more into the “blend” column of the Style Box.

Rediscovering the growth path

Recently, a divergence has emerged within the industry, with two companies clearly rediscovering their growth trajectory—primarily driven by a single class of drugs known as glucagon-like peptide-1 (GLP-1) therapies. Both Denmark’s Novo Nordisk and the US’s Eli Lilly successfully brought their GLP-1 drugs to market, originally developed to treat diabetes but later proven effective for obesity treatment.

This latter use turned these drugs into blockbuster products, as people began using them for weightloss, even in the absence of obesity. The surge in demand was so great that at one point, Novo Nordisk ran out of stock and was temporarily unable to meet demand.

This has paid off handsomely for investors of both companies. While the Morningstar Global Health Index rose 7 percent over the three years to the end of August 2024, compared with an 8 percent rise for the global equities index, Morningstar Global TME Index, Novo Nordisk and Eli Lilly shares surged by 45 percent and 59 percent, respectively.

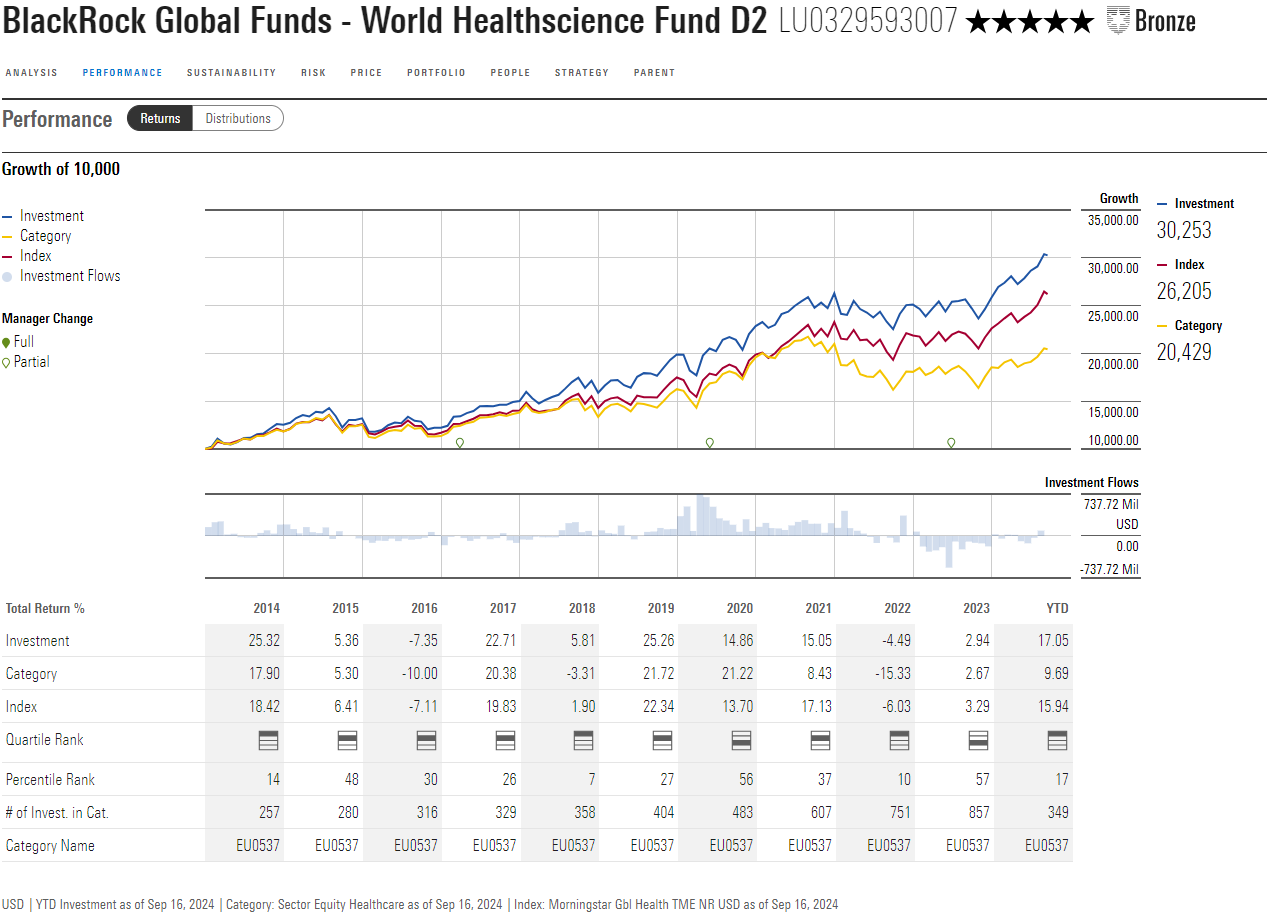

Blackrock world healthscience

Strategies that prominently appear on Morningstar’s radar are deemed to have solid management teams and robust investment processes based on qualitative analysis from the fund analysts, or through an algorithm that assesses funds using the same framework. In this edition, we spotlight BGF World Healthscience, which Morningstar analysts rate Above Average on the People Pillar and Average on the Process Pillar, resulting in a Bronze Morningstar Medalist Rating.

The experienced lead manager, Erin Xie, has been at the helm of this strategy since April 2011. She also heads Blackrock’s health science team, which includes co-manager Xiang Liu and six analysts with an average of 18 years’ experience in either investing or the medical field. This level of expertise is invaluable, given the technical nature of the sector, helping the team understand the science behind treatments, clinical trials, and product innovations.

Xie applies a bottom-up approach, but stock research and selection are influenced by a market outlook and sector analysis that considers factors such as the political and regulatory environment. The team then conducts an in-depth stock analysis, with the specific method depending on the type of company. For product-related industries such as biotechnology, medical devices, and pharmaceuticals, this involves a thorough evaluation of product pipelines and portfolios. The strategy is highly benchmark-aware, typically maintaining a modest active share of 30 percent to 40 percent (currently around 25 percent) relative to its benchmark, the MSCI World Health Care Index.

The portfolio is well-diversified, with approximately 90 positions. However, there is notable concentration in the top 10 holdings, which collectively make up around 45 percent of the portfolio. Novo Nordisk and Eli Lilly each hold a weight of just over 6 percent, significantly contributing to the fund’s performance. Other strong performers this year include UCB (109 percent), Lonza Group (57 percent), and Daiichi Sankyo (53 percent).

Ronald van Genderen is a Senior Manager Research Analyst at Morningstar. Morningstar conducts quantitative and qualitative research and analysis on investment funds. Morningstar is part of the expert panel at Investment Officer.