Donald Trump’s comeback in American politics is a reality. With a strong mandate from voters and a Republican-controlled Congress, he now has more leeway than in his previous term. Bond investors have reacted cautiously to last week’s election outcome.

A Trump administration spells overtime for journalists. However, unlike his 2016 election, this time he may be better prepared, despite rumors of concentration issues for the now 78-year-old. Much will be written about his trade policies, immigration plans, and domestic agenda, but here we focus on the potential impact on the world’s largest debt market: U.S. dollar bonds.

Skepticism among bond investors

After the election, stocks rose, particularly small caps, but U.S. financing costs also increased. The yield on U.S. government bonds, a key measure for investors, rose to nearly 4.5 percent for ten-year bonds, up from 3.8 percent at the end of September. At the same time, the dollar rose 1-2 percent against the yen and euro shortly after the election outcome. European investors must now consider whether to continue hedging currency risk as the costs of doing so have risen. The EUR/USD currently sits around 1.06, down from almost 1.09 on November 5.

Bond investors remain skeptical of Trump’s promise to curb inflation while simultaneously implementing tax cuts and pushing for lower interest rates. These objectives are difficult to reconcile, as aggressive tax cuts and deregulation may boost economic growth and consumption but also pose inflation risks. This, in turn, could lead to higher interest rates—unless the central bank deviates from its price stability mandate.

Such a scenario seems unlikely, as Trump cannot simply remove Powell, whom he appointed as Federal Reserve Chair in 2018. Powell’s term ends in May 2026, and Pimco believes his position is secure until then. The asset manager also has no doubts about the Fed’s independence.

Inflation

Trump has also spoken about cuts to the federal workforce, but economists expect his overall policies will likely lead to even larger budget deficits, which could be inflationary. Additionally, higher import tariffs are expected to drive up consumer goods prices. Even the mass deportation plan could disrupt the labor market to the extent that it ultimately drives up wage costs.

It would indeed be ironic if the very policies that helped Trump win the election later became problematic during his second term as president.

Fund Radar

The strategies prominently appearing on Morningstar’s radar are backed by fund analysts› qualitative assessment of a strong management team and a robust investment process, or receive these qualifications based on an algorithm that evaluates investment funds using the same framework.

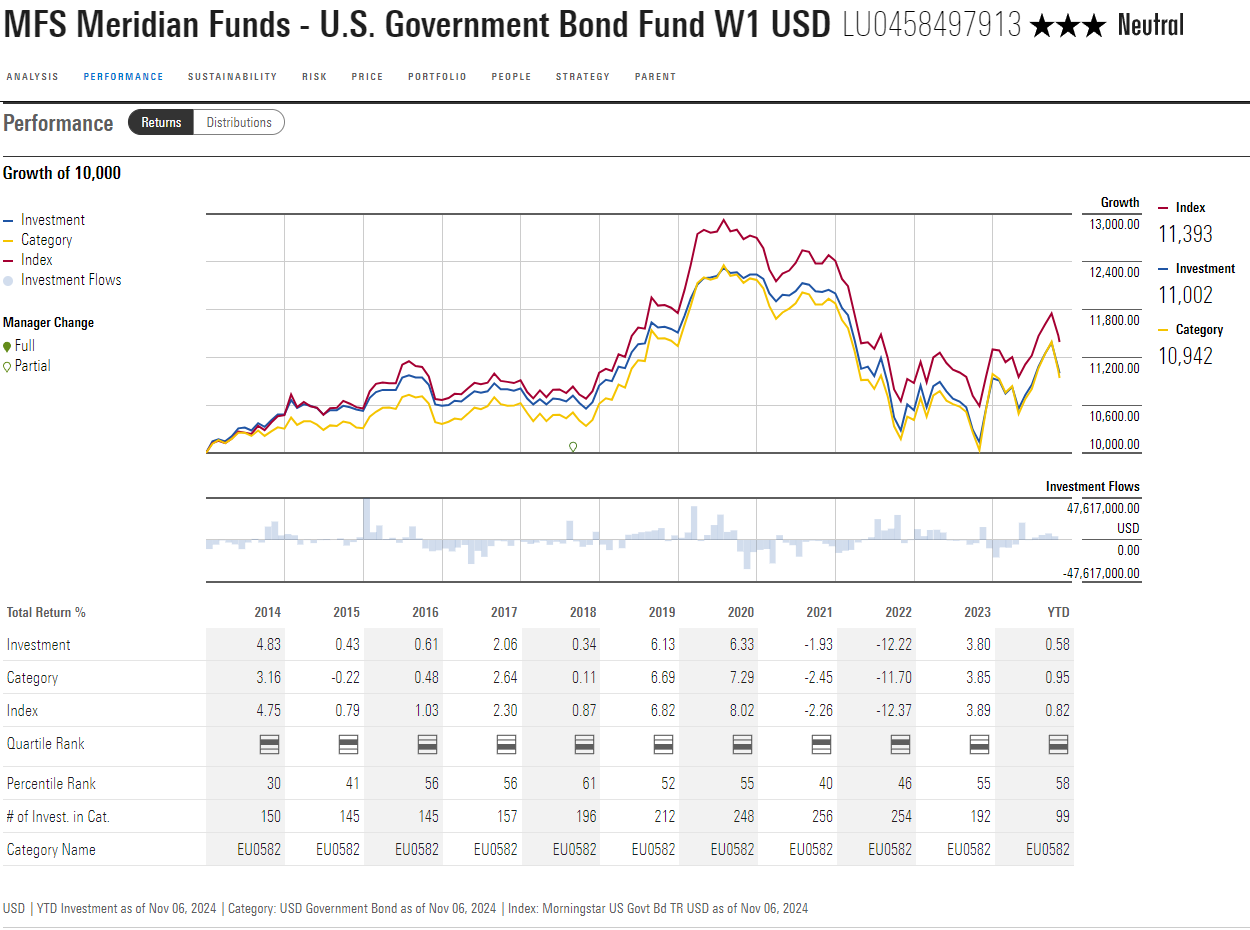

This article highlights a fund within the USD Government Bond Morningstar category, where managers have outperformed expectations (though not always relative to costs). This example demonstrates the cost disadvantage faced by many active funds in this category.

MFS Meridian US Government Bond employs a solid investment approach for the U.S. government bond and mortgage-backed securities market, though the team is small compared to its competitors. Portfolio managers Geoffrey Schechter and Jake Stone have co-managed this strategy since 2018. Schechter, a veteran at MFS, has led this strategy since 2006. Stone left Wellington for MFS in 2018, bringing six years of experience as an MBS analyst. This expertise is valuable to the strategy.

In May 2024, Schechter announced his retirement for September 2025. There are no plans to replace him, and we believe Stone is well-positioned to manage the portfolio independently. Still, this remains one of the smaller U.S. government bond teams: Stone relies on an MBS analyst and five securitized credit analysts who focus on mortgages, (R)MBS, and other securitized credit.

This strategy is benchmarked against the Bloomberg US Government/Mortgage Index and primarily invests in a mix of U.S. government bonds and MBS. Earlier this year, Morningstar analysts raised the Process rating from Average to Above Average, as Stone has, over five years with MFS, worked with qualitative analysts to develop tools that can model the duration and convexity of securities, assess their relative value, analyze portfolio-level risks, and identify trends in the broader mortgage market. These tools, along with the small exposure (up to 10 percent of assets) to securities outside the benchmark, give the process an edge over most peers in the category.

However, Morningstar remains convinced that the potential for outperformance in this market is limited. Although the managers have beaten the market before fees each year since their partnership in September 2018, the fund trails the benchmark once costs are taken into account.

Thomas De Fauw is a manager research analyst at Morningstar. Morningstar analyzes and evaluates investment funds based on quantitative and qualitative research. Morningstar is part of the Investment Officer expert panel.