I recently came across an interesting study about the Fama-French factors, those widely used risk factors that underpin how we evaluate investment performance. The findings should matter to every (institutional) investor.

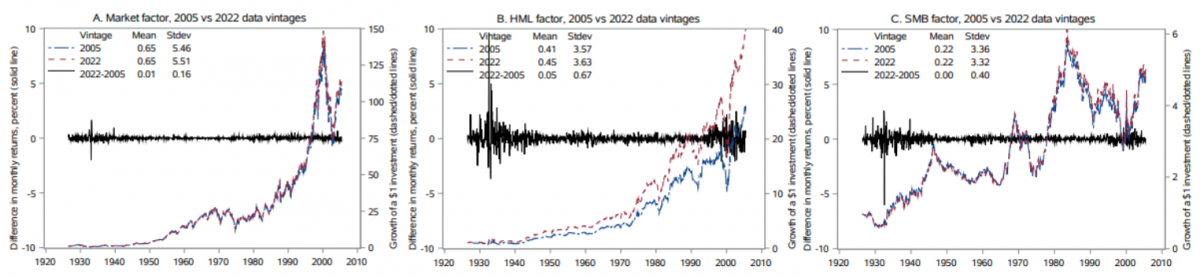

The researchers downloaded historical versions of these factors going back to 2005 and made a shocking discovery: the return of the same historical month can differ substantially depending on when the data was downloaded. For the value factor (HML), 98 percent of observations changed between just the 2005 and 2006 versions. The average annual return increased by 0.6 percent between the 2005 and 2022 versions—a huge shift for supposedly historical data.

What causes these changes? Mainly methodological revisions in how the factors are constructed, not corrections in the underlying stock data. The researchers demonstrated this by building their own factors using a fixed methodology. Data updates explained less than half of the variation in the early period and virtually nothing thereafter.

Figure 1: The return of factors from different vintages

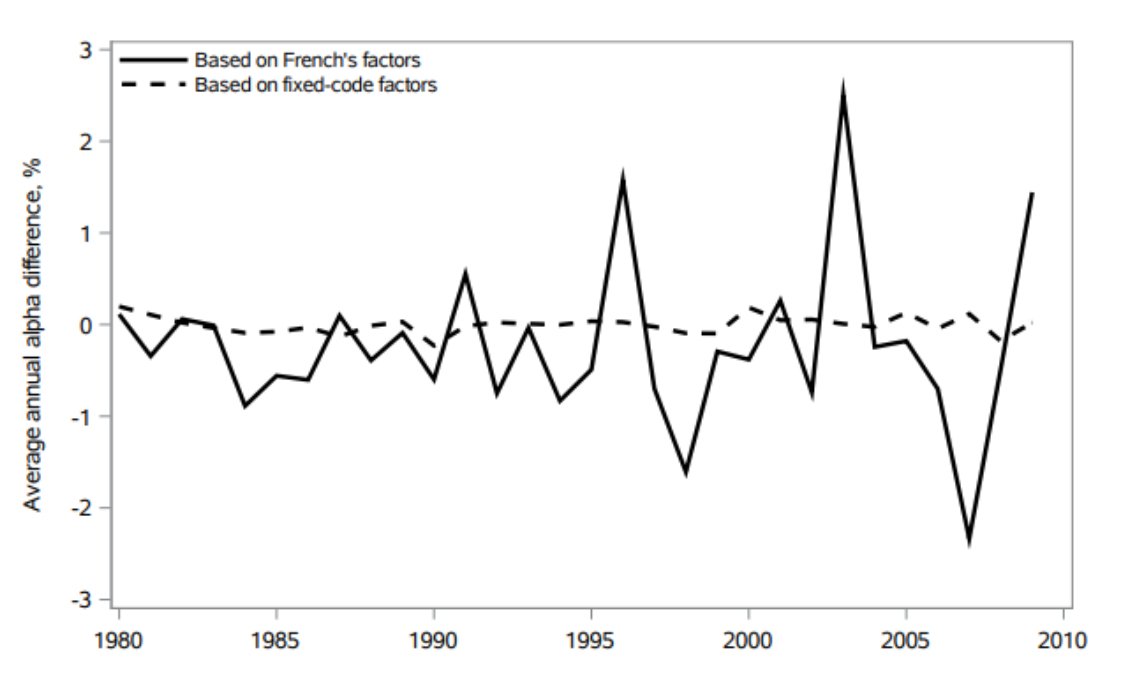

This has enormous implications for performance evaluation. When the authors recalculated fund alphas using different factor versions, more than half of the annual estimates changed by more than 1 percent. The average alpha for the entire fund industry fluctuated by more than 1 percent in some years, purely from switching factor vintages. In 2007, the industry went from apparent outperformance to underperformance depending solely on which factor version was used.

Figure 2: The difference in mutual fund alpha

Individual stock betas—crucial for cost of capital calculations—also shifted dramatically. For more than a quarter of stocks, the value factor loading changed by more than 0.1. For corporate finance decisions worth millions of euro, that is not noise; that is a serious problem.

Even “significant” anomalies are not immune. Among marginal strategies (t-statistics between 2.0 and 2.5), 28 percent lost their statistical significance purely due to factor vintage changes. This affects both what gets published and which strategies get implemented.

The troubling part? The authors found no consistent evidence that newer factor versions actually perform better. The factors do not improve, they simply change. Each revision creates a new historical reality and undermines the replicability of decades of research.

What should institutional investors do? First, document which factor vintages you use and test robustness across versions. Second, consider the authors’ fixed-code factors, which maintain methodological consistency. Third, follow the advice of Berk and Van Binsbergen to use tradable assets such as index funds instead of constructed portfolios where possible.

The academic finance community treats these factors as foundational. We build careers on findings that depend on them. But foundations should not shift beneath our feet. When historical data keeps changing, we are not standing on solid ground, we are standing on quicksand.

History should not be a moving target.

Gertjan Verdickt is assistant professor in finance at the University of Auckland and columnist at Investment Officer.