A new (American) recession remains a hot topic. And it’s understandable because a significant series of interest rate hikes by the Federal Reserve, coupled with an inverted yield curve, typically leads to economic trouble. You’d need a well-supported “this time is different” argument to claim there’s no chance of a recession.

Now, I won’t go as far as saying that there won’t be a recession. I simply don’t know. What I do know is that one of the key recession indicators is, at least, not currently pointing towards an impending downturn.

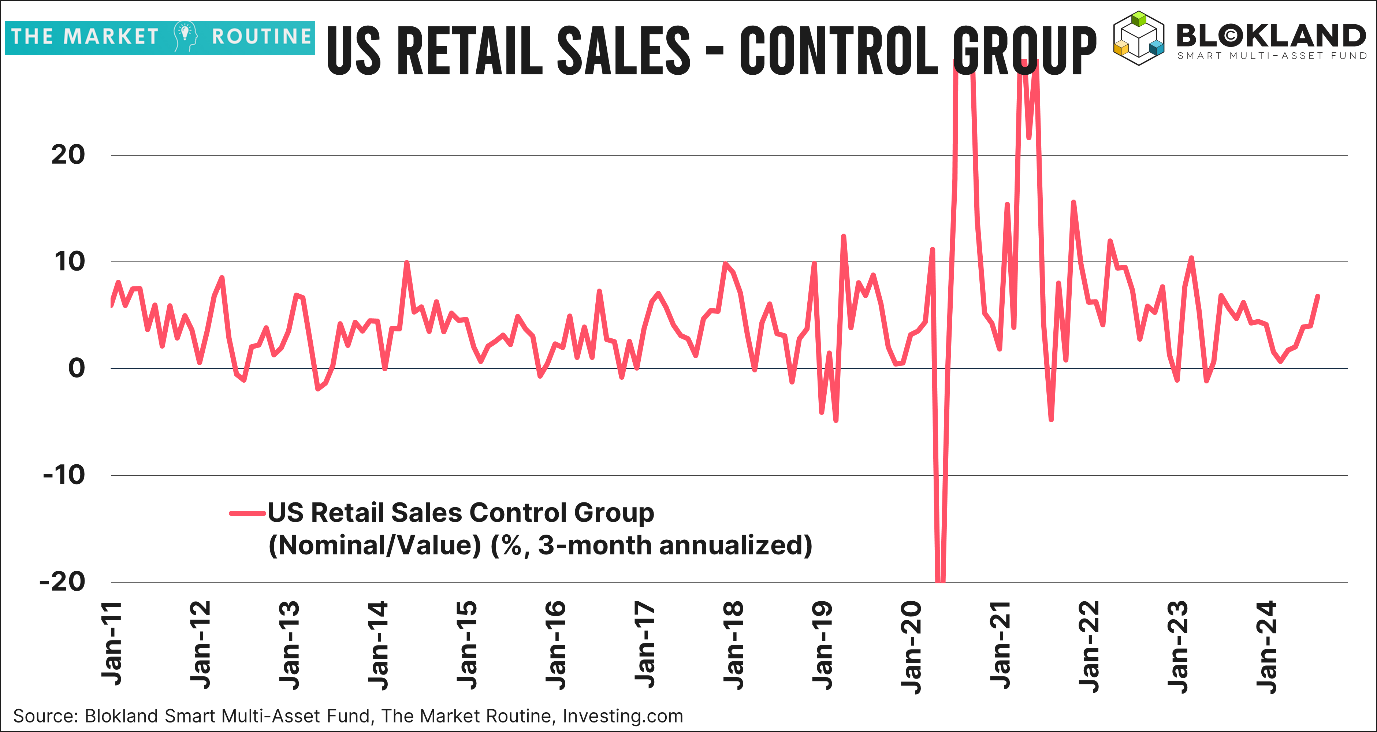

The chart below shows U.S. retail sales. My focus is primarily on the so-called control group, which excludes volatile components like auto dealers, building materials, food services, and petrol stations. Sales in this control group grew much more slowly than total retail sales, but over the past three months, they’ve increased by an annualised rate of 6.8%.

That’s hardly what you’d expect if consumer behaviour was driving a recession. And even the somewhat smug question of “but what about adjusting for inflation?” doesn’t detract from the robust trend in consumer spending. Over the past three months, prices have barely risen. After some hesitation at the start of the year, when the media were full of scary charts showing that excess savings were really depleted, Americans have stubbornly continued to spend.

Wealth!

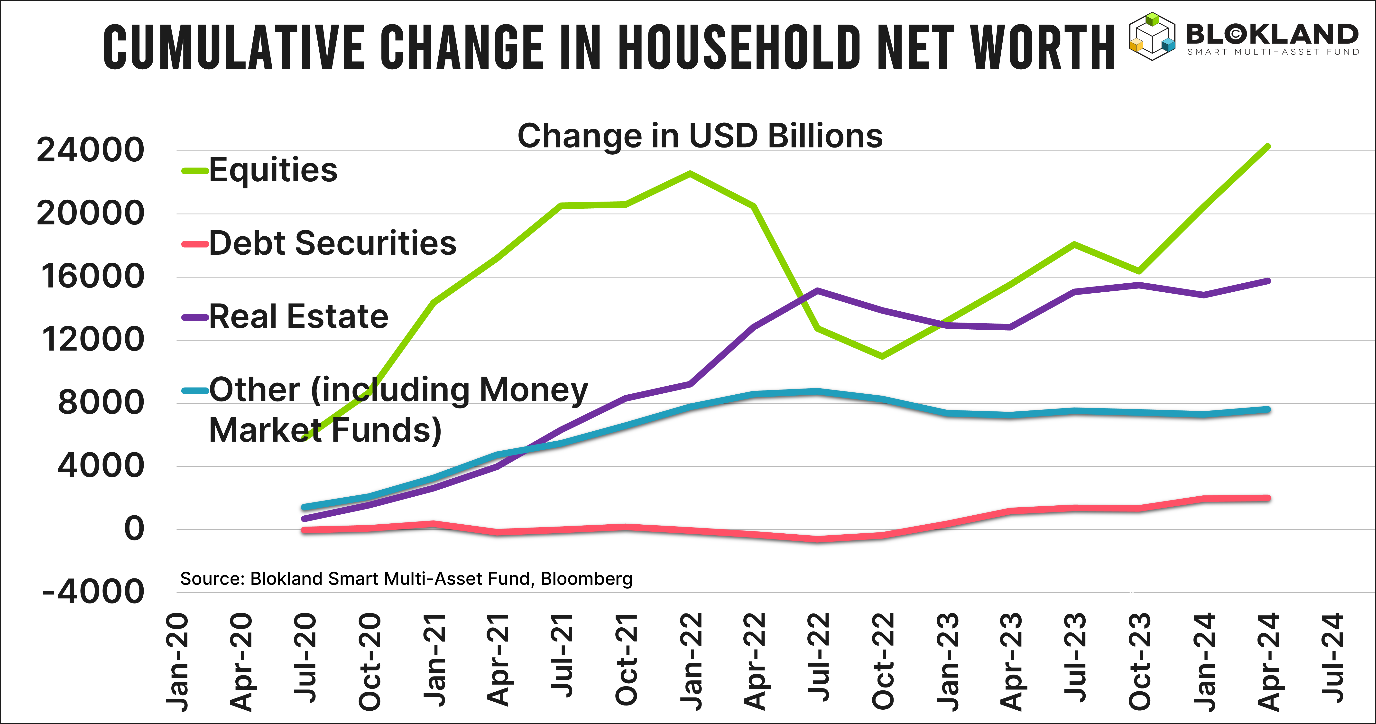

And consumers have a lot to spend. Firstly because of personal income—excluding government subsidies, which is the income measure used by the NBER that determines recessions—continues to rise steadily. But mainly because the average American’s wealth is sky-high. That “average” caveat is, unfortunately, necessary, but overall, Americans have become billions of dollars richer thanks to their stocks, real estate, and, to a lesser extent, money market funds.

Oh, and if you’re still in the camp that believes higher interest income is keeping the U.S. economy afloat, you’re mistaken. Firstly, because stocks and real estate, as the chart clearly shows, contribute much more to (changes in) wealth. Secondly, because interest payments are also a significant expense on the liability side of the balance sheet, which can’t be said for stocks.

Unemployment Recession?

What remains as a macro recession trigger is unemployment. But since Claudia Sahm abandoned her rule—that a recession follows if the three-month moving average unemployment rate rises by more than 0.5% from its lowest point in the past twelve months—a recession driven by unemployment may not be immediately likely either. Though it seems wise to keep a close eye on it.

Take Risks!

Suppose that recession doesn’t materialise, and this monetary tightening cycle does indeed get labelled as “this time IS different”? In that case, I wouldn’t be too pessimistic about stocks and other riskier asset classes that thrive on liquidity. Interest rates get cut, bond sales are scaled back, and meanwhile, China tries to revive its economy with lower rates and yet more debt—because, of course, that’s always part of the equation.

But now ofcourse we will see that tomorrow we enter a new recession…

Jeroen Blokland analyses eye-catching, topical charts on financial markets and macroeconomics in his newsletter, The Market Routine. He also manages the Blokland Smart Multi-Asset Fund.