Yes, they’re back again. With rising interest rates firmly on investors’ minds worldwide, the doom-mongers are crawling out from under their rocks to once again predict the bursting of the ‘extremely expensive’ tech bubble. But I have my doubts.

Before I largely dismantle the main argument of these doom-mongers, let me be clear. In recent years, we’ve seen multiple instances where markets begin to crack when interest rates in the United States and the United Kingdom approach 5 percent (in the weaker Eurozone, that threshold is closer to 4 percent). And with the US 10-year yield just below 4.8 percent at the time of writing, a new test appears to be in the making.

Internet bubble 2.0

But that’s quite different from ‘concluding’ based on current valuations that the tech bubble must now burst. Not least because none of these perennial pessimists even attempts to provide an objective definition of what a stock market bubble actually is.

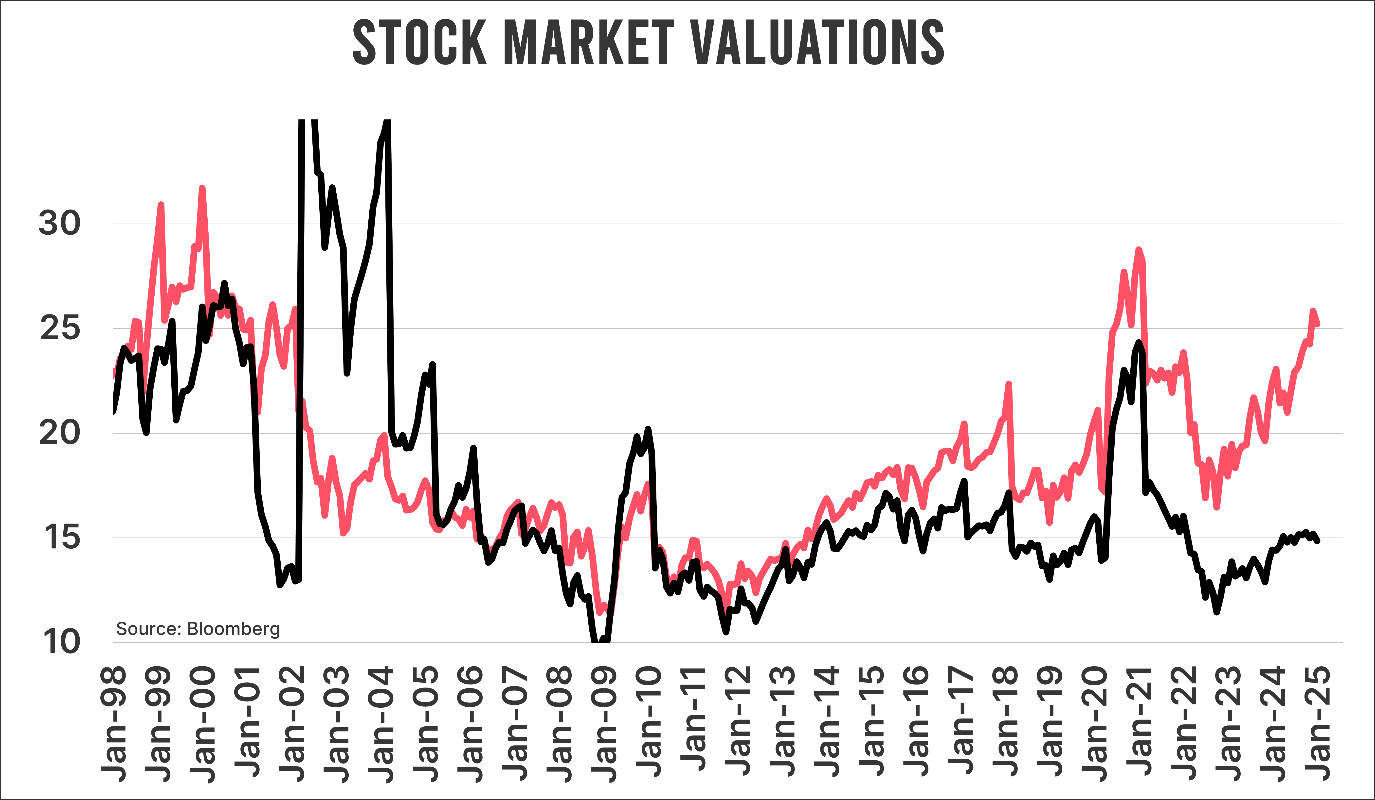

The chart below displays the price-to-earnings ratios (P/E) of the MSCI USA Index and the MSCI WORLD ex USA Index. Naturally, American equities are the epicentre of many bubble spotters, which is why I’ve given them a separate line. However, since the world, despite the colossal weight of US stocks in the index, is still somewhat larger than the United States, I’ve also included the P/E ratios of equities in the rest of the world.

A few things stand out. First: while US equities are far from cheap, they were slightly more expensive in 1999 – right before the ‘bubble’ burst. The average P/E ratio of US equities that year was 27.8, compared to an average of 23.2 over the past twelve months. That’s a significant 20 percent difference.

What’s particularly striking is the valuation of equities in the rest of the world. At the end of 2024, the P/E ratio stood at a modest 14.9, compared to a peak of 26 in 1999. That’s quite a difference. For those now tempted to log into their brokerage account and load up on European and Japanese stocks: remember the old investment adage that things are often ‘cheap for a reason.’

Look at interest rates

But the comparison doesn’t end there. Technology companies, with their sometimes exponential revenue growth – a trend that the average linear-thinking individual, whether a professional investor or not, struggles to properly assess – are highly sensitive to interest rates. From this perspective, the recent pressure on tech stock prices is hardly surprising.

That said, interest rates were significantly higher during the actual bubble. In early 2000, the US 10-year yield climbed to 6.78 percent, precisely 2 percentage points higher than today. The average interest rate in 1999 was 5.64 percent, compared to 4.20 percent in 2024.

Conclusion

Taking the interest rate difference between then and now into account, I believe it’s clear that current valuations are far from the ‘spectacular’ levels seen leading up to the bursting of the dot-com bubble.

The rise in interest rates is undoubtedly worrying, especially since it’s driven by renewed inflationary pressures. We saw in 2022 how this can affect stocks and even more so bonds. But I don’t think inflation will again reach such extreme levels. The argument that current valuations will act as a catalyst for a severe correction seems rather thin to me.

Jeroen Blokland analyses striking and topical charts about financial markets and macroeconomics in his newsletter, The Market Routine. He is also the manager of the Blokland Smart Multi-Asset Fund, which invests in equities, gold, and bitcoin.