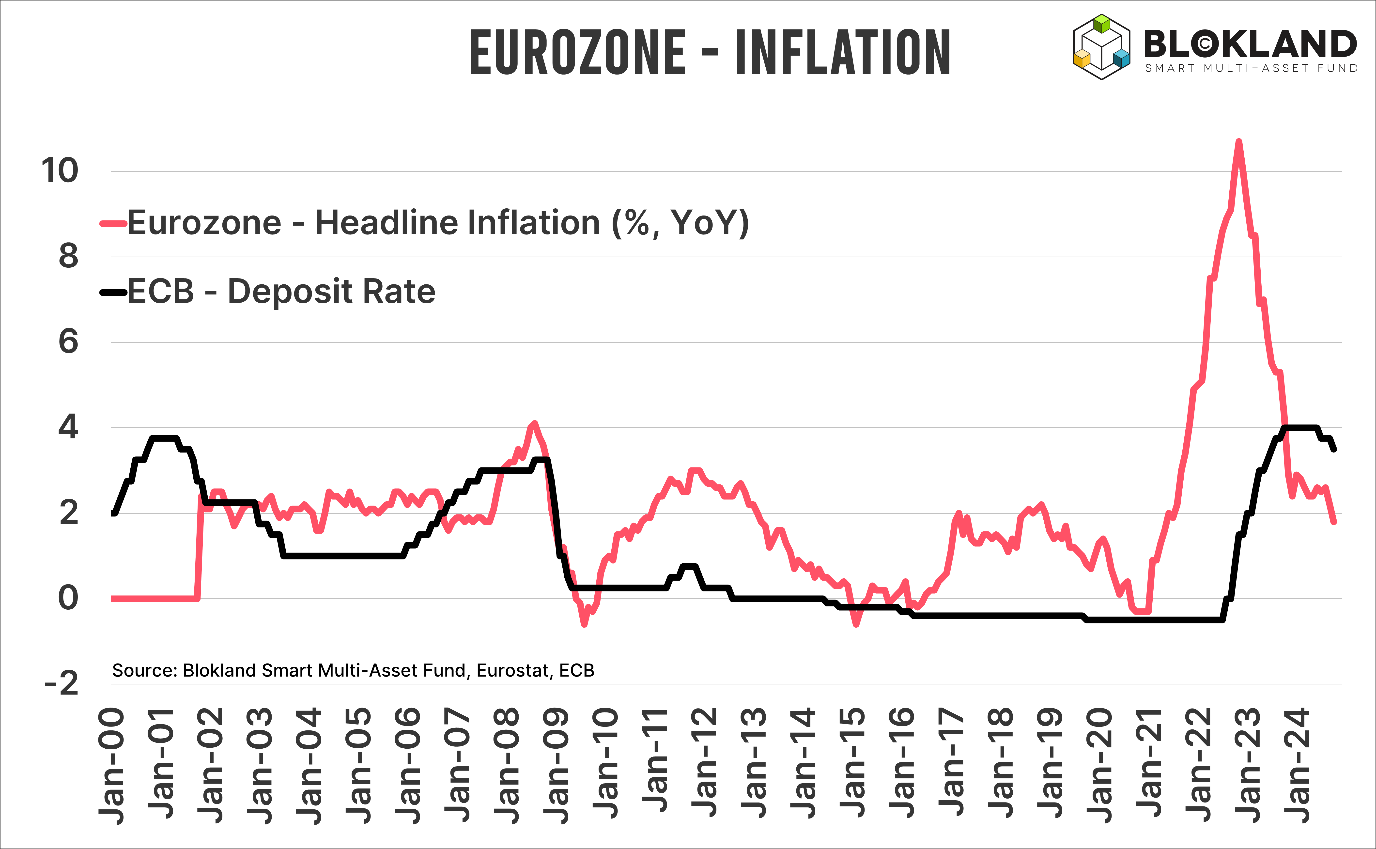

Inflation in the Eurozone has fallen to 1.8 percent. This marks the first time since June 2021 that inflation in September dropped below the ECB’s target of 2 percent. Despite many experts claiming that the central bank interest rate can’t be lowered much this time, the ECB now has plenty of reasons with this latest inflation figure to significantly cut interest rates.

The 1.8 percent inflation is high compared to the core countries. In Germany, France, Spain, and Italy, inflation was lower than the Eurozone average, with Italy even below 1 percent. With this latest series of inflation figures, the path is now open for a series of interest rate cuts, potentially bringing the rate below 2 percent, rather than the 3 percent that, among others, DNB president Klaas Knot is considering.

Deflation fears

On 27 May this year, ECB chief economist Philip Lane gave a noteworthy speech in Dublin about inflation, in which he said: “keeping rates overly restrictive for too long could push inflation below target over the medium term”.

Although the speech was filled with ‘data dependency’ — a popular term among central bankers to avoid being pinned down on policy — this statement is telling. Even after the highest inflation in decades, central bankers care only about the rate of price change, not the price level itself, with deflation as the ultimate taboo.

Misery

Inflation below 2 percent isn’t the only reason for a series of interest rate cuts. It is expected that Germany will lower its GDP growth forecast to zero. The country is struggling with poor energy and employment policies combined with (too) strict budgetary discipline. The result is predictable: you are no longer a part of the economic game.

In fact, Germany seems to be destroying its own industry, with the automotive industry being a prime example. Volkswagen has already issued two profit warnings, and developments at other German car manufacturers are far from rosy. The share prices of all major German car producers have recently dropped by more than 20 percent, partly due to fierce competition from Chinese manufacturers.

Debt growth

Dissatisfaction in Germany is growing by the day, and it seems inevitable that Germany will eventually cave in and pump debt into the economy to create any form of growth. With surrounding countries like Italy, which have significantly higher debt levels, it’s certainly convenient if the interest rate tool can be fully utilised to prevent new discussions about debt sustainability.

Conclusion

The combination of low economic growth and low inflation throws the door wide open for the ECB to significantly cut interest rates. I expect that at the slightest setback, the ECB will use the above arguments to adjust interest rate expectations.

The ECB does have an excellent track record of “policy mistakes” — just think of that one extra rate hike in July 2008 — so it’s entirely possible that the ECB will once again be overtaken by events before taking action. But it seems evident to me that the rate will not remain at 3 percent or just below. Sleep tight!

Jeroen Blokland analyses striking, current charts on financial markets and macroeconomics in his newsletter The Market Routine. He is also the manager of the Blokland Smart Multi-Asset Fund.