If there is one thing that characterizes the investment world, it is that it is full of clichés, parrots, and an enormous reluctance to change. It is sometimes laughable how market experts produce the same one-liners for twenty years or bury you under their “market wisdom.”

But I cannot shake the feeling that investing actually is changing. As a multi-asset-trained investor, I was raised with the idea that, with the right macro lens—granted, you are often wrong—you can more or less determine which asset class should perform well over the next six or twelve months.

This way of thinking is widely reflected across the industry: huge numbers of economists—generally not the best investors, by the way—macro strategists, and model builders try to determine the right portfolio allocation. I immersed myself in it for years. And to be honest, we got quite far.

Political experts

Where I used to start the day by scanning the macro fields via the well-known WECO command on my Bloomberg terminal, I now almost always begin with “Top News.”

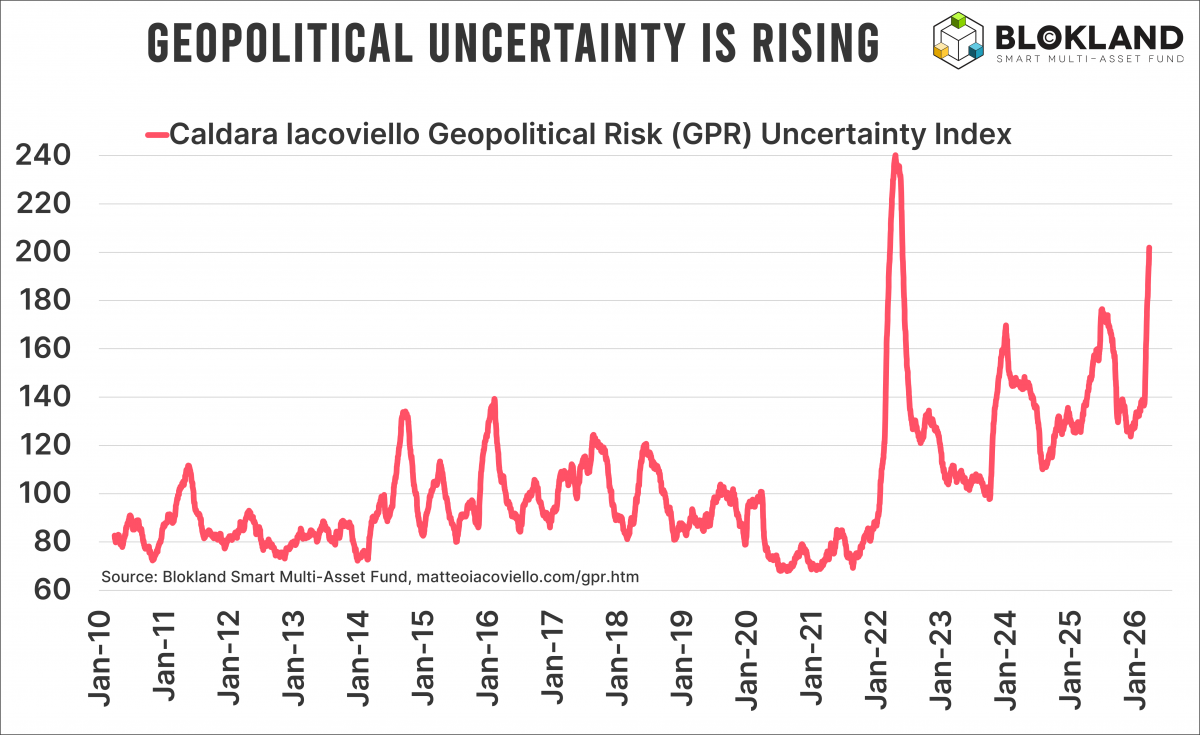

That timeline has been dominated in recent years by virus outbreaks, failed US regional banks, massive budget deficits, tariff wars, and—far and away number one—geopolitical tensions that may or may not escalate into military conflicts.

Because let’s be honest: what is the value of the latest reported inflation figure if Trump announces new tariffs the next day? Or if the oil price suddenly explodes because missiles are flying back and forth in the Middle East? How should you assess a decline in job growth in the United States while borders are closing and people are being deported en masse? What does a change in the once-leading Ifo index still tell us, other than that German industry is being hollowed out from within by excessive climate policy and bureaucracy?

In recent years, you are better off being a political expert with knowledge of geopolitical relationships than a classic macro investor.

Central banks

Of course, not all macro data has become irrelevant. Central banks remain decisive. But something is changing there as well.

The chair of the Fed is being sued for allegedly spending too much money on a renovation (although in the Netherlands renovations typically end up costing twice as much as planned). Trump constantly talks about firing him. And for the past few months, there has been someone on the FOMC who consistently presses the “cut” button.

Here we go again

Perhaps I am starting to sound like a broken record. And with the recent decline in the gold price, many critics are once again daring to crawl out from under their rocks. But if the world is clearly changing, shouldn’t our investments change with it? If we need to look at markets from a different perspective, isn’t it logical that the outcome will also be different? Does a passive stock-bond portfolio still suffice?

The direct attacks on the current Fed chair, the series of French prime ministers who have fallen because budgets were not in order, and the endless money creation as a necessary lubricant to keep a debt-driven economy afloat… Combined with higher and more volatile inflation as a result of geopolitical tensions, where oil often acts as the pressure valve, this raises the question of how many bonds are still needed and whether there should be more room for commodities.

Rebalancing

And do you really think that India—and especially China—will feel inclined to cooperate “nicely” with the United States after these conflicts? Right now, a handful of ships are sailing through the Strait of Hormuz, provided that settlement ultimately takes place in yuan rather than dollars.

It seems evident that China, followed by key trading partners, is doing everything it can to distance itself from dollar hegemony. In my book The Great Rebalancing, there is a chart showing that when the share of the dollar in global currency reserves declines, the gold price typically rises. No one is paying attention to that now. But that does not mean the relationship has disappeared.

We are seeing the loss of purchasing power in bonds, a positive correlation between stocks and bonds that was long considered unthinkable, a money supply that continues to grow structurally, an economic and political climate that is becoming increasingly polarized, inflation that is more erratic and higher than we were used to, energy uncertainty that will not simply disappear, and monetary policy that is being deployed ever more aggressively to keep the system afloat. At the same time, asset classes that were once marketed as superior through glossy brochures have proven to be less robust than those glossy brochures suggested. Hint: the name of those asset classes starts with “private.”

Something will have to change in the investment world. Right?

Jeroen Blokland analyzes striking, up-to-date charts on financial markets and the macro economy. He is also manager of the Blokland Smart Multi-Asset Fund, a fund that invests in stocks, gold, and bitcoin.