Soaring oil prices, solid job growth, and a seemingly unhurried Powell have forced markets to significantly scale back expectations regarding Federal Reserve rate cuts. However, Powell and his colleagues will be in for a lot of trouble if they don’t cut rates at each of the upcoming meetings.

At the time of writing, investors see around a 13 percent chance that there will be no rate cut at all in November, versus an 87 percent chance of a quarter-point cut. Barely two weeks ago, it was a fifty-fifty split between a quarter-point cut and another jumbo 0.50 percent cut.

This means that, for the first time in months, there is a (slightly) positive discrepancy between what markets expect and what the Fed is likely to do. In my view, it seems highly unlikely that the central bank will pause.

Job growth

First, while job growth came in at a much higher-than-expected 254,000 in September, further cooling seems a matter of time. Job openings, temporary employment, and the ISM Employment figures are some leading indicators that support this view.

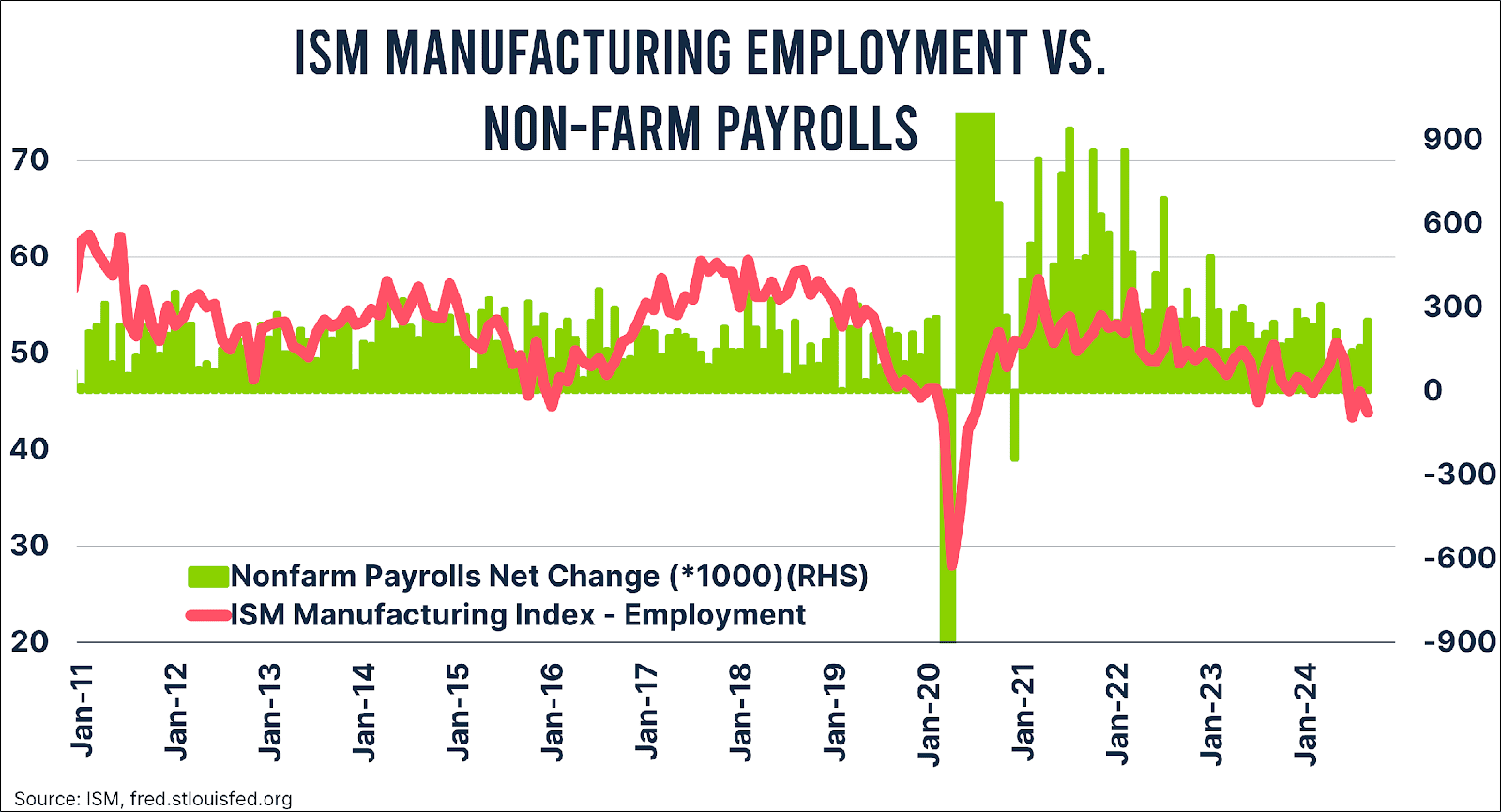

Below is the ISM Manufacturing Employment Index compared to job growth. The former has dropped to a concerning level of 43.9, where job growth historically tends to disappear like snow in the sun. And for those who argue “but it’s all about the services sector”: the ISM Services Employment Index sits at an uninspiring 48.1. With the Federal Reserve now signalling both verbally and in writing that it is focusing more on the employment part of its dual mandate, not cutting rates would be strange.

The donkey?

Moreover, the Fed would be making the same mistake twice if it doesn’t lower rates. In July, Powell and his team forgot to cut rates, which put them in an awkward position. They had to watch for over six weeks as employment worsened and geopolitical tensions increased, with their hands tied. As a result, they became a plaything for financial markets.

I don’t think Powell and his associates want to go through that again. With a 25 point cut, you keep all options open.

Debt sustainability

Then there’s the issue of debt sustainability. The Committee for a Responsible Federal Budget has calculated that both Harris and Trump will further worsen the US budget.

Brace yourself: the committee expects that, in Harris’s case, the debt-to-GDP ratio will rise to 133 percent over the next ten years, and under Trump, it could reach 142 percent. These are percentage points “worse” than the already dubious path outlined by the Congressional Budget Office, which forecasts 125 percent of GDP. That 142 percent would put you in “Italian-sounding” debt territory.

I can already hear the MMT enthusiasts proclaiming that since the United States is a sovereign nation with its own currency, bankruptcy is impossible. Worse yet, they argue that all those new bonds are a fantastic asset for someone’s balance sheet.

Indeed, the US won’t go bankrupt, and with the dollar, Harris or Trump will hold the world’s reserve currency. But that doesn’t mean there’s nothing wrong. Interest costs are rising, doubts about debt sustainability are growing, and the key question is: who wants all those bonds on their balance sheet?

To stay ahead of all these tough questions, it’s certainly helpful if the central bank continues cutting rates. Therefore, I expect the Fed to keep cutting, at least until we reach the level where the next discussion begins: what exactly is the neutral rate?

Jeroen Blokland analyses charts on financial markets and macroeconomics in his newsletter The Market Routine. He also manages the Blokland Smart Multi-Asset Fund.