Since Trump’s reelection as president of the United States, the world has been on edge. Geopolitical tensions dominate the markets, and the role of the dollar is once again under discussion. Still, I find it difficult to translate that into the idea that this is the moment for the euro to step out of the greenback’s shadow. There are simply too many loose ends.

One of the most frequently cited arguments for a weaker dollar is US government debt. It is enormous and, through rising interest expenses and the ever-increasing likelihood that the Federal Reserve will have to run the printing press at full capacity, it would lead to a loss of value for the world’s most important currency.

For clarity: US government debt really is huge. And to prevent it from dragging down the entire system, extreme measures will be required. But to conclude that the euro must automatically rise against the dollar is, at the very least, creative.

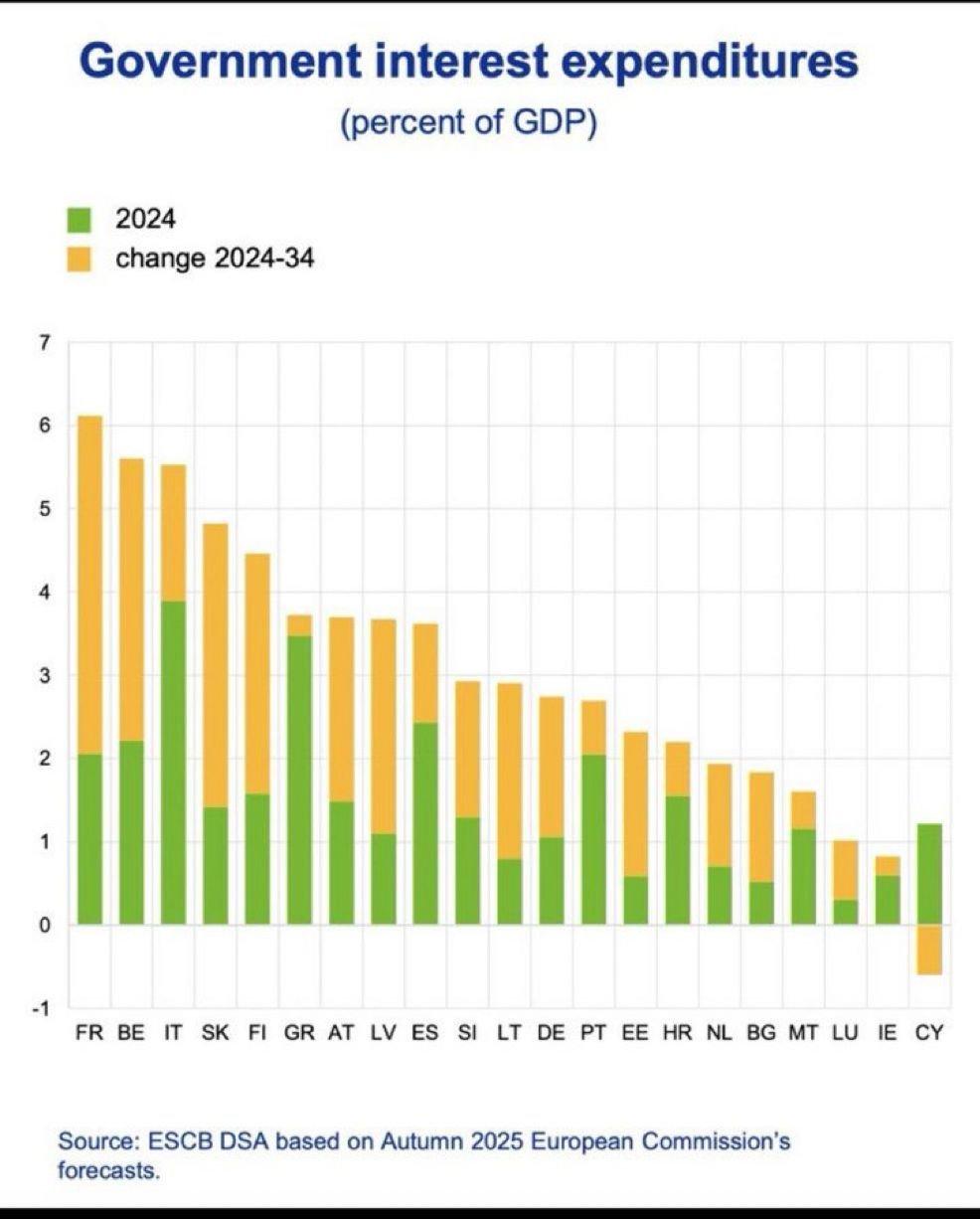

Take a look at the chart below. It shows how much interest expenses, measured as a percent of GDP, are expected to increase over the next ten years in various eurozone countries.

France ranks at the top, not entirely unexpectedly. The French welfare state is one of the most expensive in Europe. What do you expect with an effective retirement age of around 62, along with structurally high budget deficits and towering debt as a result? At current interest rate levels, which are by no means exceptionally high, French interest expenses are rising from roughly 2 percent to more than 6 percent of GDP.

In other words, with a current structural budget deficit of about 5 percent of GDP, France would move toward 9 percent, assuming nothing else changes.

The weakest link

The usual response is that the figures for the eurozone as a whole are less dramatic than those for France. That is correct. But it is also entirely irrelevant.

The European sovereign debt crisis painfully demonstrated that within a monetary union, the weakest link is decisive. If that were not the case, the Greeks would by now simply be paying for their groceries in drachmas again. And the Italians in lira.

The question is not whether France will run into trouble, but when. And at that moment, all policy, including that of the ECB, will be primarily directed at France.

Moreover, US interest expenses are rising less rapidly than those of France. In ten years, they are estimated at 4.6 percent of GDP in the US. Substantial, but less severe than in France. In addition, US debt is financed at shorter maturities, meaning that rate cuts by the Federal Reserve translate relatively quickly into lower interest costs. The reasoning that rising interest expenses automatically lead to a weaker dollar against the euro therefore does not hold up.

The euro is expensive

Beyond debt dynamics, the stronger growth potential of the United States would argue for a stronger, rather than a weaker, dollar. Especially because the euro is less cheap than the simple euro-dollar exchange rate suggests.

Many investors look exclusively at the euro-dollar rate to determine whether the euro is “cheap” or “expensive.” But they miss the broader picture. If you look at the trade-weighted euro, the value of the euro against a broad group of trading partners, the euro is currently more expensive than at any time since its introduction in 1999.

You would not reach that conclusion by looking only at the euro-dollar rate. The dollar is expensive. But the euro is even more expensive. If you were to project the trade-weighted value of the euro onto the euro-dollar exchange rate in a chart, you would arrive at a rate of roughly 1.60 to bring the lines into alignment.

American exceptionalism

Does this mean the euro can only fall against the dollar? I consider that likelihood significant, with one clear nuance: the premium for American exceptionalism.

As the world’s reserve currency, the dollar enjoys unique privileges. The dollar is the primary currency in central bank reserves, dominant in international trade, and the standard unit of account for commodities. That status implies a premium. If the United States were to lose that exceptional position, it is plausible that the dollar would forfeit part of that premium. No one knows exactly how large that premium is, but there is room here for a broad weakening of the dollar.

The same dynamic applies to gold. The larger the share of gold in central bank reserves at the expense of the dollar, the higher the gold price expressed in dollars.

But with the opening of this column fresh in mind, it sounds more plausible to me that all fiat currencies will ultimately lose ground against gold before the euro will become structurally stronger than the dollar. It seems only a matter of time before the euro falls.

Jeroen Blokland analyzes striking, timely charts on the financial markets and macroeconomics. He is also manager of the Blokland Smart Multi-Asset Fund, a fund that invests in equities, gold, and bitcoin.