I have been watching the financial markets with some amazement for the past few weeks. A US president threatening the eradication of an entire society, while equity markets remain largely unchanged. Then a fresh TACO triggers a recovery rally of several percent, even though there is nothing more than a two-week ceasefire and ongoing uncertainty. For anyone looking even slightly ahead, a clear bump appears that we will all have to get over.

A swift end to the conflict, which one can only hope will now truly materialize, does not mean everything will simply return to normal. There is at least one crucial factor that you can already be almost certain will cause problems: inflation.

That higher energy prices lead to higher inflation is no surprise, but the data that recently appeared on my screen confirmed what I had already suspected: inflation is likely to come in higher than many expect.

What companies pay

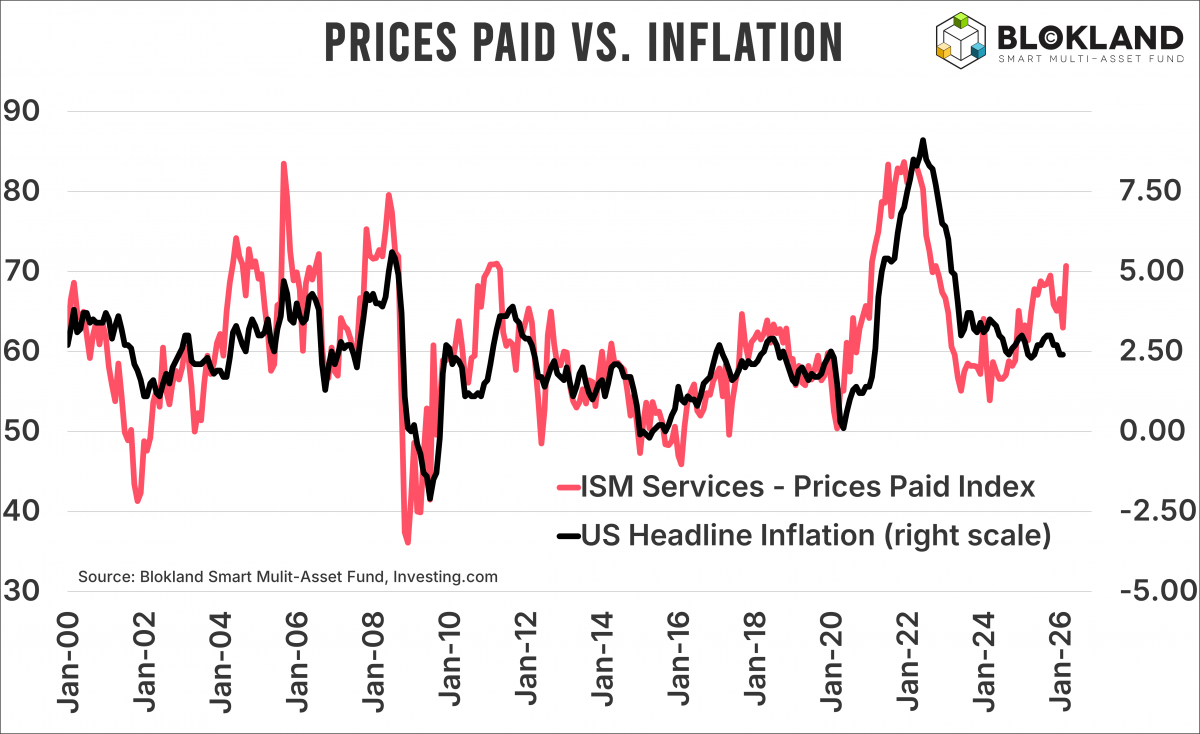

Below is a chart showing the subindex for prices paid of the ISM Services Index on the left axis and US inflation on the right axis. Although ISM Services (unjustly) still tends to be the neglected counterpart compared to ISM Manufacturing, the relationship between the two macro indicators is, to put it mildly, strong. And clearly stronger than the relationship between the ISM Manufacturing price index and US inflation.

That subindex for ISM Services prices rose to 70.7 in May, the highest level since October 2022. At that time, US inflation stood at a staggering 8.2 percent, driven by massive Covid stimulus, disrupted supply chains, and, not to forget, central banks on fairytale island stubbornly insisting that inflation was temporary.

Nevertheless, the picture becomes rather uncomfortable when you align the two lines neatly. With a reading above 70, US inflation could easily move toward 5 percent. Apart from a few extremes, there are very few investors, consumers, and central bankers taking such a high inflation rate into account.

Social unrest?

That ISM index is not the only indicator pointing to higher prices. If you compare the price of nitrogen-based fertilizers, largely determined by the price of natural gas, with global food prices, the picture becomes more than uncomfortable. It is almost certain that food prices, which were already rising before the war, will continue to increase.

Historically, that is a proven recipe for social unrest. When people have less to eat, they start doing extreme things, which is hard to blame them for. With geopolitical tensions extremely high and polarization at extreme levels, it is not something you want to dwell on for too long.

The money machine

Then there is the money supply. Financial markets already required an enormous amount of liquidity. This is partly due to all the debt that now, after Covid, has to be rolled over at higher interest rates. Given everything happening in private debt (and equity), maintaining ample liquidity is no small feat.

Central banks have now stopped shrinking their balance sheets, and the growth of the global money supply is accelerating. At the same time, various governments are choosing to support their citizens through energy subsidies, while the American war will undoubtedly show up in the budget deficit.

Although inflation is nowadays almost universally equated with the rise of an arbitrary index of a basket of goods and services, the term historically referred to money growth. The more that was expanded, the higher inflation would be.

The inflation investor

In my column two weeks ago, I wrote about the end of the traditional macro investor. Those who still focus exclusively on published macro data are missing a large part of the forces currently driving markets.

With uncertain, yet nonetheless higher, inflation ahead, investors will once again have to learn a new technique within just a few years: that of inflation protection.

The days when one could confidently present purely nominal returns and maintain that investing in inflation-sensitive instruments such as bonds carried little risk are truly far behind us. Fortunately, more and more investors are recognizing this and acting accordingly.

Jeroen Blokland analyzes striking, current charts on financial markets and macroeconomics. He is also manager of the Blokland Smart Multi-Asset Fund, a fund that invests in equities, gold, and bitcoin.