For over ten years, I’ve been writing articles for investors, economists, and anyone with even the slightest interest in the financial markets. Extremely negative stories, stories about the issues of the day, or stories with sensational headlines tend to do particularly well. Although I’m occasionally lumped into the first category, I’m usually not very good at writing those kinds of stories. But today I have a topic that tops the charts every day: Artificial Intelligence.

Everyone uses AI these days—whether it’s to improve texts (or simply have them written entirely), to create beautiful images, or of course to ask a vast number of questions. Who even “googles” anymore?

Those were also my main forms of “collaboration” with AI. But over the past few weeks, I’ve started taking a more ambitious approach—and with results, I’d say.

For example, we built a database of everyone who has ever come into contact with my investment fund and who might still be interested in participating. We created an HTML tool that allows investors to determine, based on objective data, how much impact inflation has had on their savings and wealth. Using that same objective data, we developed an optimization model showing that bitcoin and gold do belong in the optimal mix, while there is no longer any place for bonds. And we used AI to write a complete video script about central banks, the role of money in our debt-driven economy, and how scarce assets play a crucial role in protecting wealth.

And I still consider myself something of an AI amateur, with plenty of room for improvement.

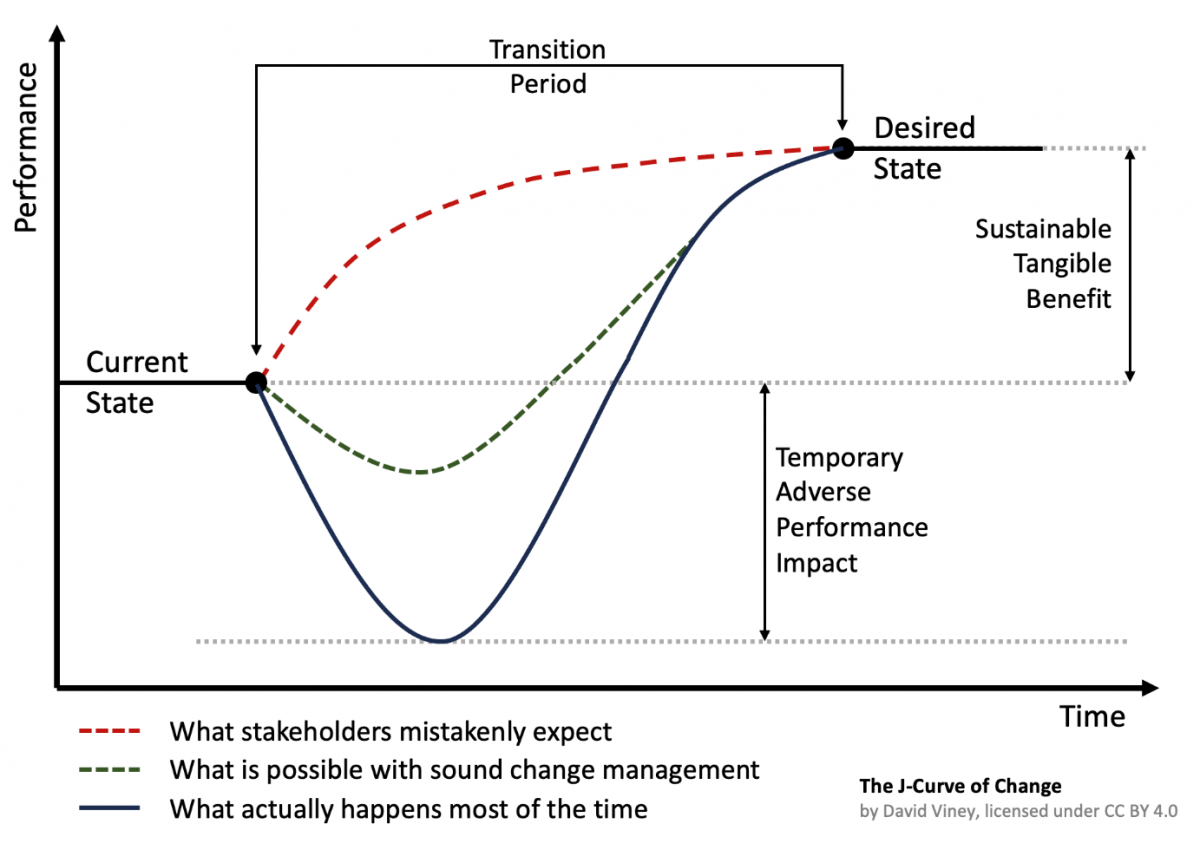

The J-curve

These experiences remind me of the work of Erik Brynjolfsson, a professor at Stanford University and a prominent figure in my book The Great Rebalancing, which argues that technological progress—and AI in particular—will drive an unprecedented boom in productivity.

One of his key points is that it always takes longer than many people expect before the real benefits of progress can be realized. Simply because people—and the organizations they work for—need time to process all these changes and possibilities. To make optimal use of AI, companies—and their employees—must adapt. And that takes time.

This means that productivity growth may actually decline temporarily before accelerating exponentially, driven by the integration of new technology.

This principle is clearly illustrated by the J-curve of David Viney, a leading figure in digital and technological transformation. Even with a realistic process of change, productivity will in most cases decline at first before reaching a higher level.

Low-Hanging Fruit

As I’ve pointed out before, there is also a school of thought that is somewhat less enthusiastic about the potential of AI. Tyler Cowen, a professor at George Mason University, for example, argues that the low-hanging fruit has already been picked.

Key drivers of growth—such as the availability of free and unused land, access to quality education, and broadly applicable industrial breakthroughs—are largely behind us.

As impressive as today’s AI capabilities may seem, current technological developments do not compare to the glory days of unchecked, technology-driven growth of the past—think, for example, of the Industrial Revolution.

U-Turn

That said, there is also a very real risk. And I don’t mean that everyone will lose their jobs tomorrow. I’m in the camp that believes AI—or any major new breakthrough—will ultimately create new jobs, some of which we can’t even imagine yet.

My concern lies in the combination of massive investments in AI and an aging population. One reason productivity growth declined for so long—or even turned negative—is aging. Older workers tend to work more slowly and are less adept at adopting new technologies.

With an aging workforce—and increasingly, outright labor shortages in fields like education, primary care, skilled trades, and transportation—the likelihood of the J-curve effect diminishes. And so does the likelihood that all these investments will ultimately pay off.

That’s especially uncertain given that AI’s benefits will not be evenly distributed across companies. Much like the internet, there will be a select group of winners and a large number of losers. The debt being accumulated today will eventually come onto investors’ radar if sufficient profits fail to materialize.

All things considered, I’ve shifted slightly toward the J-curve theory. That’s not exactly comforting, given that the decline and aging of the workforce are putting significant pressure on potential GDP growth. But let’s keep things upbeat for today: I’ll take more AI.

Jeroen Blokland analyzes striking, up-to-date charts on the financial markets and macroeconomy. He is also the manager of the Blokland Smart Multi-Asset Fund, which invests in equities, gold, and bitcoin.