Even before stock market trading in March had really gotten underway, we already knew this month would end up in the history books. You also have to be particularly creative now to write a column that does not touch on what is happening in the Middle East. So here is the expected topic, but with a twist.

Many reports focus on the end of the world. As a perpetual doomsayer, you naturally have to seize every opportunity to once again end up being completely wrong. Even more reports focus on the short-lived impact that military confrontations usually have on stock market prices.

Both statements are true. But it is also a fair observation that stock market developments are increasingly driven by factors that, at least not directly, affect companies’ business models.

And I am not referring only to the structural increase in geopolitical tensions. Social and political polarization, persistent fiscal and debt-related issues, and growing doubts about central bank policy are just a few other examples. We are not in a temporary disruption but in a structural regime shift in which geopolitics, energy, and debt dynamics are forcing permanently higher inflation and risk premiums.

If the world in which you invest is changing, should your investment portfolio not change as well? You may already sense where this is going. It remains an unsolvable mystery to me why the average investor does not store even a small portion of their wealth in gold, while gold has proven to deal far better with all those headline-making factors than traditional investment portfolios.

Unhedged

If the Strait of Hormuz closes, bonds are not what you want to hold. In the first few days of what Trump says could easily last weeks, perhaps even months, the oil price rose by about 15 percent. Changes in the oil price are often reflected almost one-for-one in inflation data. With central banks already feeling compelled to maintain at least some degree of credibility, that quickly leads to rising interest rates.

At the time of writing, bonds have therefore simply been in negative territory since the attacks. You may be falling less sharply than with a tech stock, but there is no real protection.

Missed opportunities

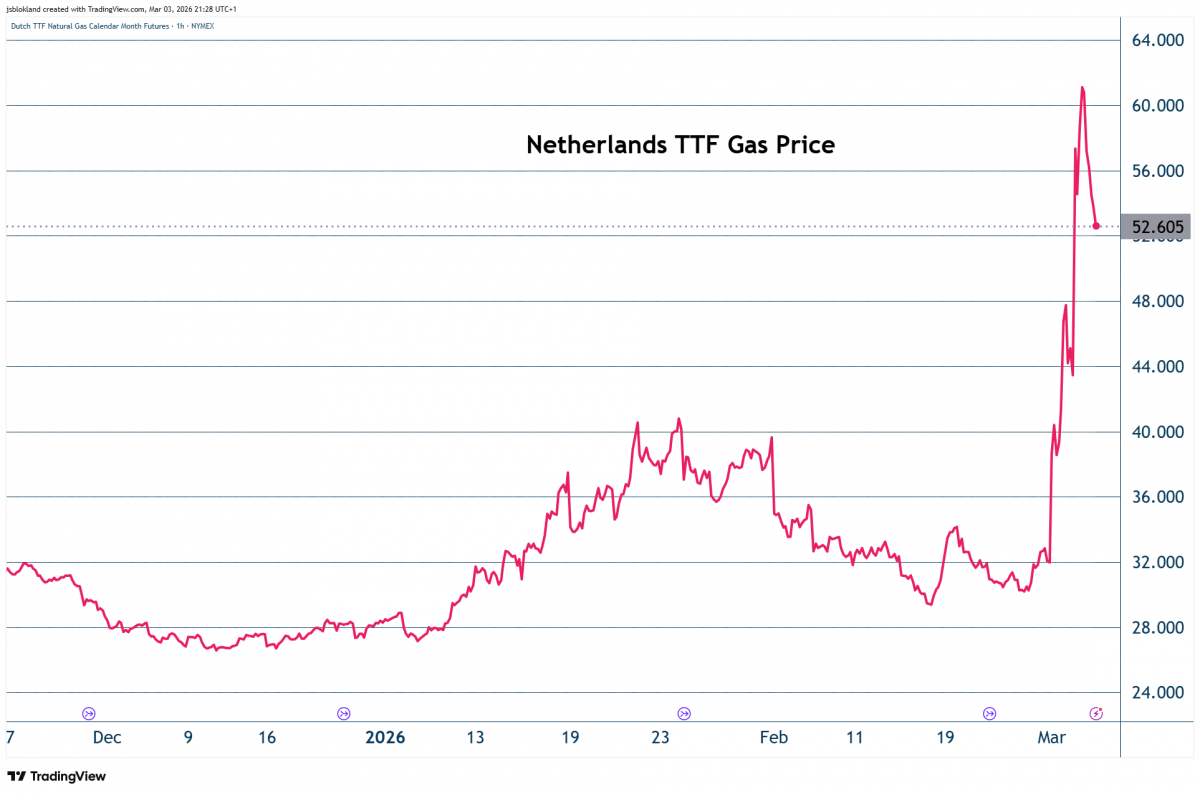

My real twist, however, concerns European policymaking. When I read that people, fully panicked by rising gas prices and the trauma of a few years ago, are desperately trying to secure a fixed energy contract and failing, I hope for a turning point.

How much evidence do policymakers and their voters still want that letting a society drift on immigration debates and unrealistic sustainability targets does not work? It is no coincidence—though it does amount to misleading investors—that one asset manager after another is loosening its sustainability criteria in order to add defense stocks. It is no coincidence that Chancellor Merz, after what was clearly an eye-opening visit to China, returns home saying that things cannot continue like this. That Germans cannot work 40 percent fewer hours than the Chinese and at the same time expect everything to turn out fine.

If you now feel tempted to argue that Germany is much more productive per hour worked, forget it. Productivity growth in my neighboring country has been negative for years. And so it is also no coincidence that Merz emphasizes that climate matters, but not at any cost.

With every geopolitical shock, with every piece of evidence of a structural decline in our competitiveness, with every realization that the policy mistakes of recent years have demonstrably had negative consequences, I hope that the political climate in Europe shifts. Not to the left or the right—the center is usually the most stable—but toward balance. Policies in which energy security, just like housing security, safety, education, and healthcare, once again take center stage.

Developments in the Middle East are the umpteenth wake-up call that it is time for change. Will it ever happen?

Jeroen Blokland analyzes striking and current charts on the financial markets and macroeconomy. He is also manager of the Blokland Smart Multi-Asset Fund, a fund that invests in stocks, gold, and bitcoin.