A beneficial side effect of President Trump is that we can trash all incoming macro figures without further analysis. That saves time and provides space to focus on what will almost certainly be a titanic battle: Powell vs Trump.

While multiple empirical studies show that import tariffs do not necessarily lead to more inflation—because the volume effect of tariffs can actually lead to lower prices and companies often absorb some of the tariffs through their profit margins precisely to mitigate the volume effect—that is not what the market is currently expecting.

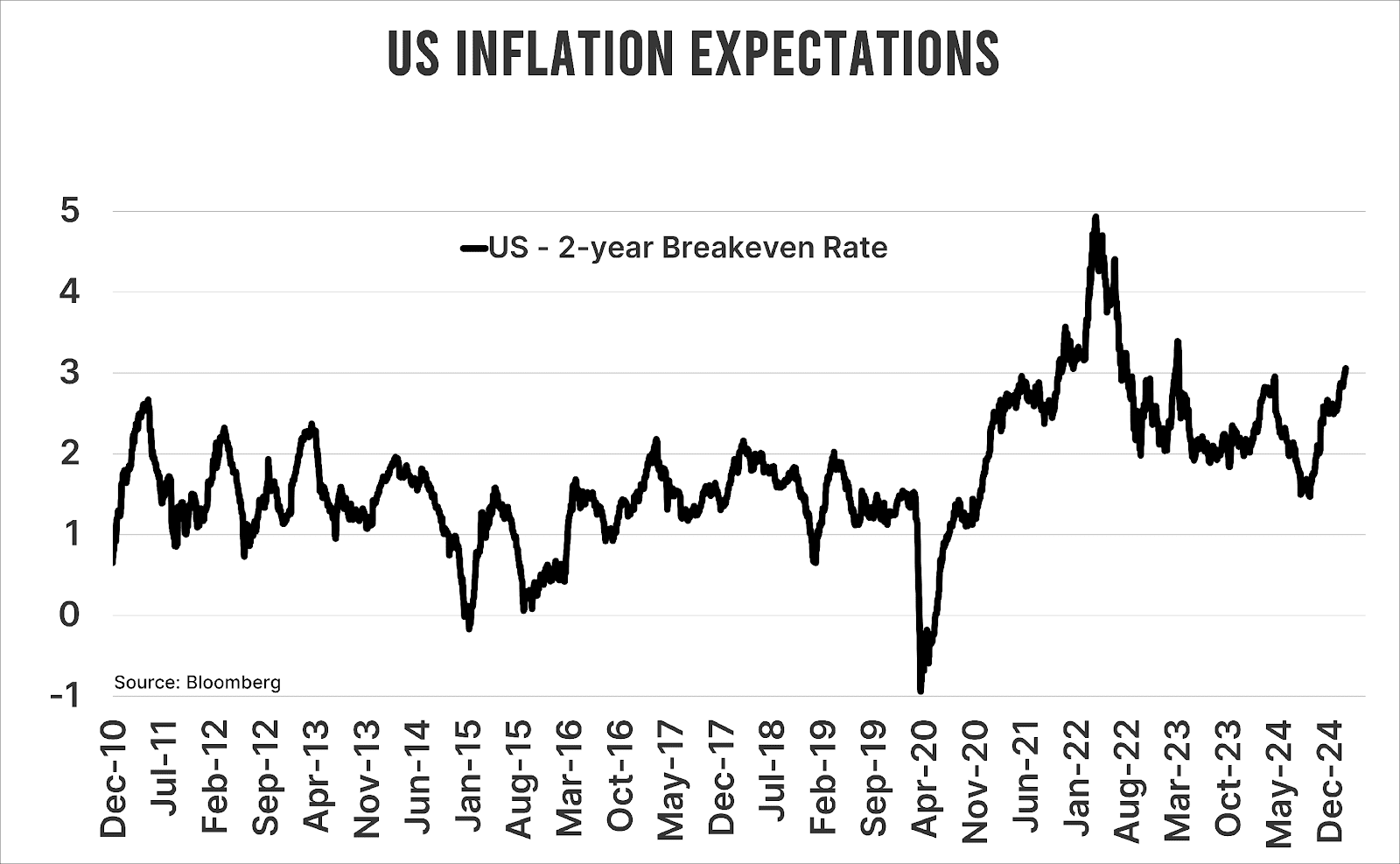

The chart above shows the 2-year breakeven rate in the US, or the difference between interest rates on nominal and inflation-indexed bonds (TIPS). In less than five months, it has doubled and is now above 3.0 percent. No surprise: the correlation with Trump’s rate rhetoric is high. After the first round of tariffs—whose levies for Canada and Mexico were immediately suspended for a month—the breakeven rate rose to its highest level in almost two years.

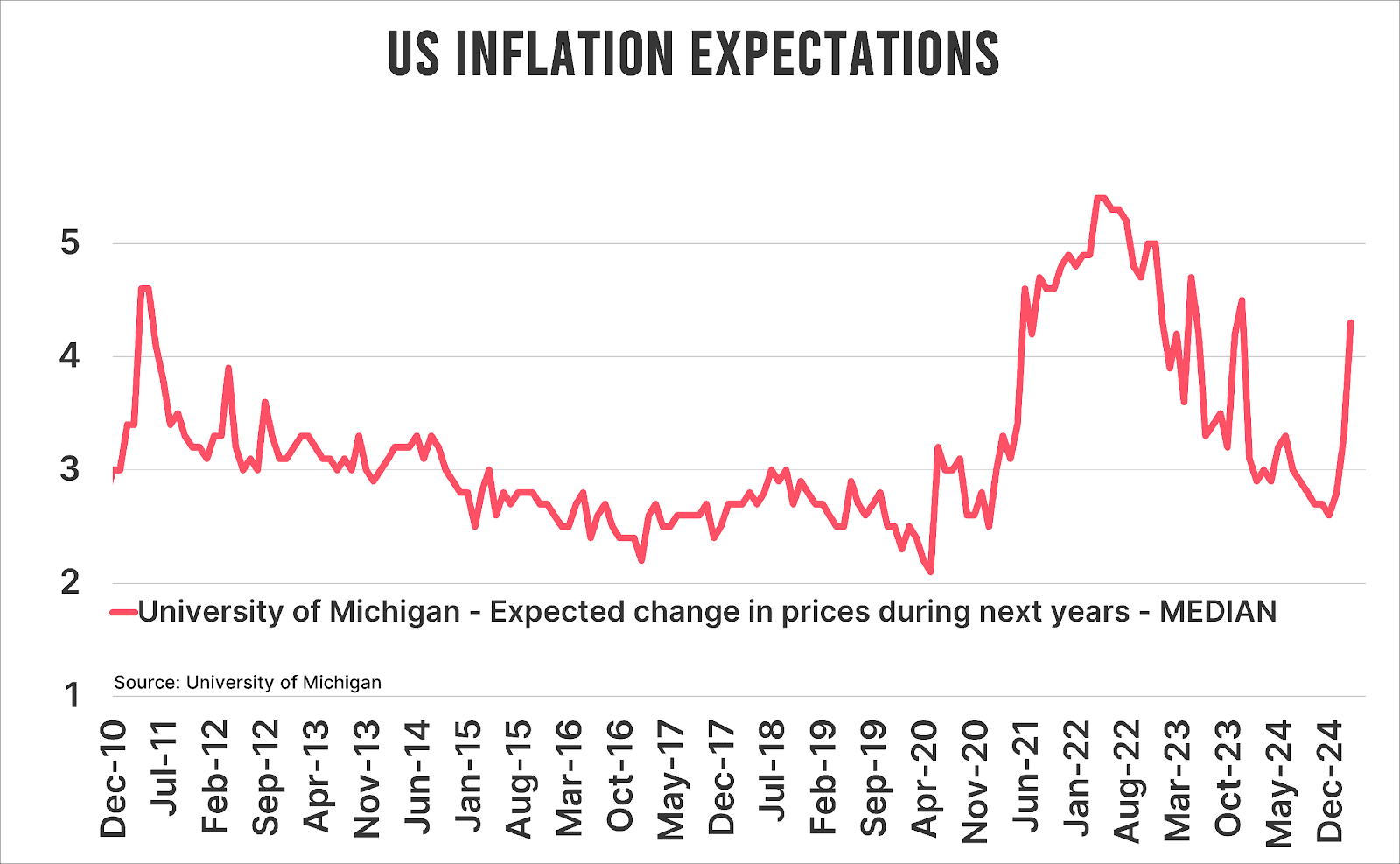

But that is peanuts compared to the following chart. Here we see US consumer inflation expectations for the next 12 months. That rose by a full percentage point to 4.3 percent this month, simply because Americans are constantly bombarded with clickbait about import tariffs.

Powell parked

The Federal Reserve does not take kindly to which inflation definition is used—no doubt Fed toilets are full of tiles saying ‘the end justifies the means’—but inflation expectations always play a role in policy.

In other words, with markets and consumers convinced that Trump is undercutting purchasing power, Powell is stuck. The Fed already had to take a break because of persistent inflation risks, and now that Trump has pushed transparency to absolute zero, it is well-nigh impossible for Powell and his colleagues to do anything but wait and see.

Incidentally, I expect US inflation to remain structurally above 2 percent, but that aside.

It’s going to crackle

We know from Trump’s previous tenure that he and the Fed boss do not exactly go well together. Powell was therefore quick to make it clear at one of the FOMC meetings that the president cannot just fire him.

Funnily enough, Trump has so far kept relatively quiet. His Treasury Secretary let it be known that Trump is not concerned with interest rate cuts, but with lowering 10-year interest rates.

Without Powell’s help, Trump has roughly two ways to get that done:

- Lower inflation

- A recession

You can feel it coming: it is only a matter of time before Trump’s focus shifts to barely a kilometre away: the Fed headquarters. Judging by the characters of the two men, that could crackle big time. Especially if it turns out that all this madness from USAID is just drops in the ocean. After all, to really make a dent in the ever-expanding budget deficit, the DOGE-boss needs to look at sacred cows like healthcare and social services. But let Elon figure that out for himself.

Jeroen Blokland analyses eye-catching, topical charts on financial markets and macroeconomics in his newsletter The Market Routine. He also manages the Blokland Smart Multi-Asset Fund, a fund that invests in equities, gold and bitcoin.