Fed Chair Powell has made no secret of it: he and his colleagues aim to bring interest rates back to the elusive, yet undefined, neutral rate. To reinforce this narrative, the FOMC members filled their forecasts with a significant number of expected rate cuts. However, the question now arises: does inflation actually permit this?

What stands out to me in the inflation debate is that, despite inflation failing to hit the 2 percent mark for three and a half years, the special inflation measures that were emphasised during the peak inflation period—supposedly to provide a clearer picture—suddenly seem to have lost their importance.

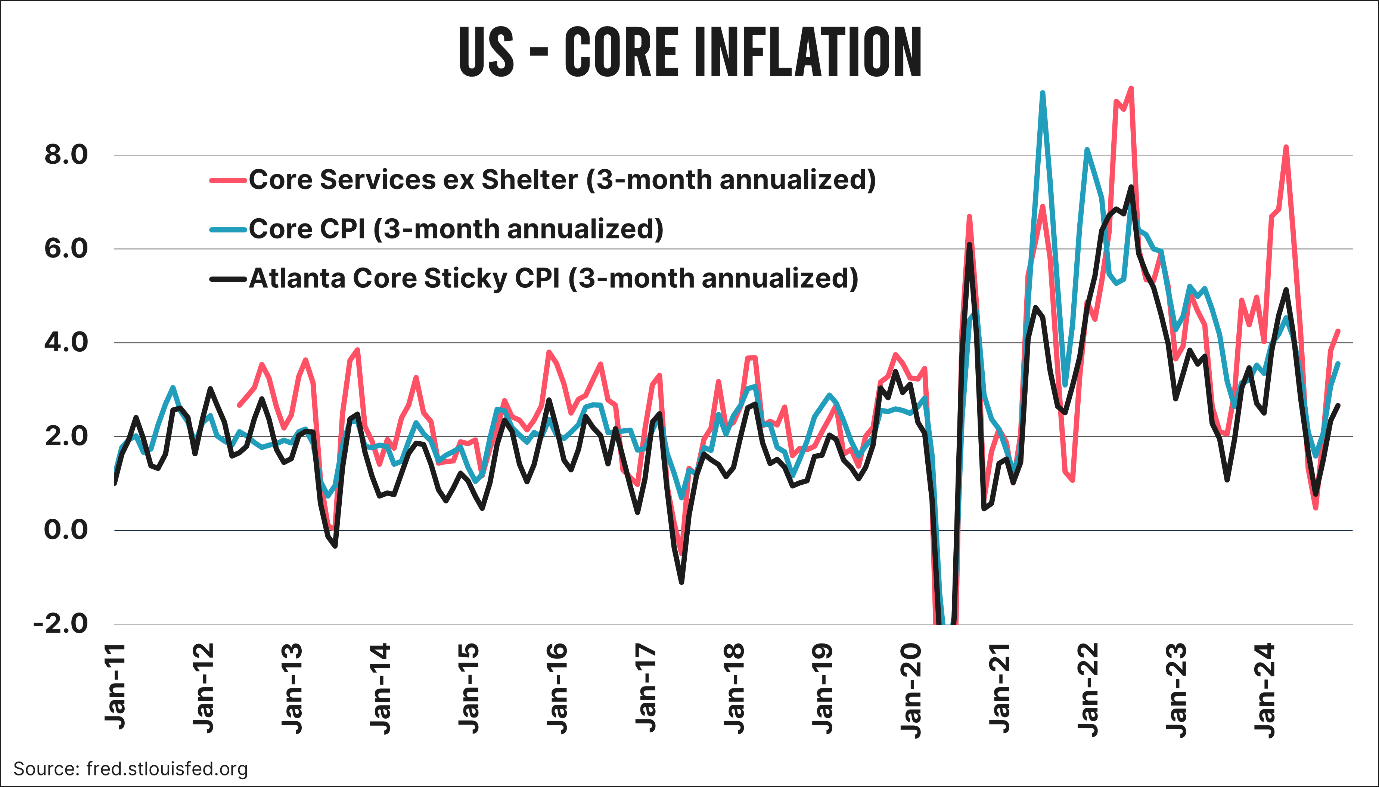

For instance, when was the last time Powell mentioned the three-month annualised Core Services ex-Shelter inflation? This metric was, for a considerable part of the inflation crisis, seen as the benchmark on which the Fed tried to base its policy. And there were other price indicators that have now faded into obscurity. Fortunately, I’ve kept the charts for these inflation indicators neatly at hand. Below is a graph showing the three-month annualised Core Services ex-Shelter, the Atlanta Fed Core Sticky Prices, and regular core inflation.

In October, inflation according to these three indicators stood at 4.2 percent, 2.7 percent, and 3.6 percent, respectively—all well above the Fed’s 2 percent target. Over the past 12 months, inflation levels have been at 4.4 percent, 2.9 percent, and 3.3 percent. Again, these figures show that the Fed is still far from where Powell and his colleagues want to be.

Considered crazy

Of course, it’s true that with a Fed Target Rate of 4.75 percent (upper range), you are still well above the neutral rate. While opinions vary, most experts estimate that the neutral rate lies somewhere between 2.5 percent and 3.0 percent.

Personally, I believe it might be even lower, especially when considering factors like potential growth (on a downward trend) and the rising U.S. debt burden (on an upward trend). But had you suggested a few years ago that the Federal Reserve would happily be cutting rates with an inflation measure above 4 percent, those same experts would likely have considered you crazy.

The key question

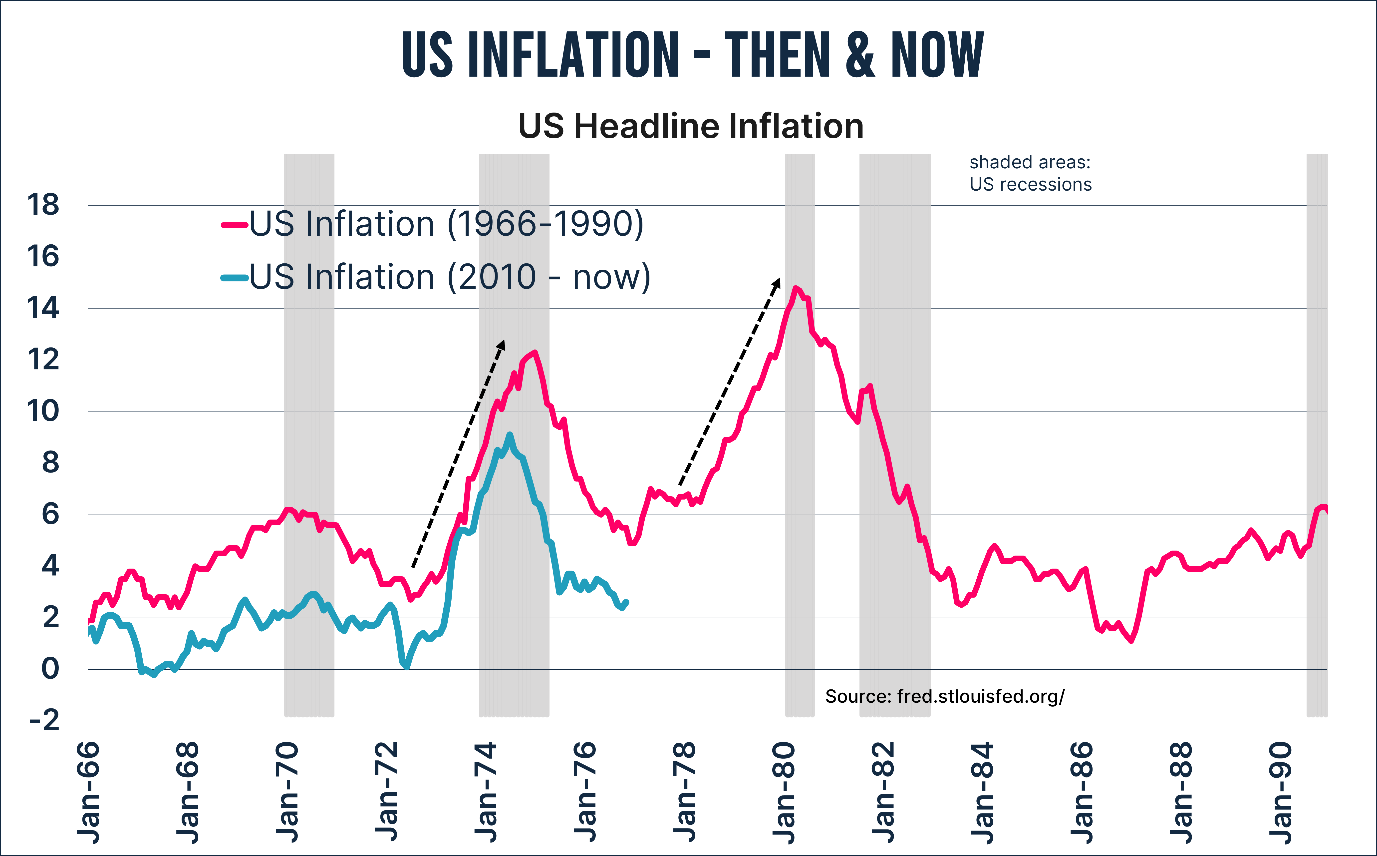

The pressing question now is whether we are headed for a repeat of the 1970s and 1980s. Back then, following an extraordinary inflation peak of over 12 percent, an even more extreme peak of nearly 15 percent occurred a few years later. That price explosion cemented then-Fed Chair Volcker’s place in history, as he was forced to raise interest rates to well above 10 percent.

Of course, I don’t know the answer to this question either, except to say that a repeat scenario cannot be ruled out. For example, Trump and Elon Musk have floated cutting 2 trillion dollar in government spending per year, but a simple calculation shows this is almost certainly doomed to fail. “Mandatory” spending on social security and healthcare continues to rise rapidly. Unless Trump is willing to relinquish his clean sweep ambitions in the 2026 Senate elections, making cuts to these expenditures will remain difficult.

Another key question

With all this in mind, another question arises: why is Powell so eager to cut rates already? After all, the U.S. economy doesn’t seem to be collapsing under an interest rate of just over 4 percent.

My answer to this is that the Fed doesn’t have two, but three mandates: price stability (read: structural currency devaluation), maximum employment, and debt sustainability. Powell has repeatedly stated that the fiscal policy of his country is unsustainable. “We are past the point of needing to have an adult conversation about fiscal policies,” Powell said.

By lowering rates early, concerns about debt sustainability can be partly managed. Since “monetising” debt has become commonplace—ensuring the U.S. won’t face bankruptcy any time soon—the Fed always retains the option to push rates down. First, through rate cuts, and later through Quantitative Easing.

Perhaps that’s precisely why Powell seems to have forgotten about those once-critical inflation measures.

Jeroen Blokland analyses striking, current financial market and macroeconomic charts in his newsletter, The Market Routine. He also manages the Blokland Smart Multi-Asset Fund, which invests in equities, gold, and bitcoin.