I often read that stocks are incredibly expensive and that a significant correction is “imminent.” But I actually think it’s not as dramatic as it seems. It all depends on the valuation lens you use.

What seems to influence stock investors and “experts” the most is that they view stocks as if they’re the only asset class available, without actively seeking out the most attractive investment categories. But, of course, that’s not how it works. The only way to truly assess if stocks are “expensive” is to compare them with the valuation of other investments. Since most investors are still anchored in the outdated ‘60-40’ rule, bonds become the primary candidate for such a cross-asset comparison.

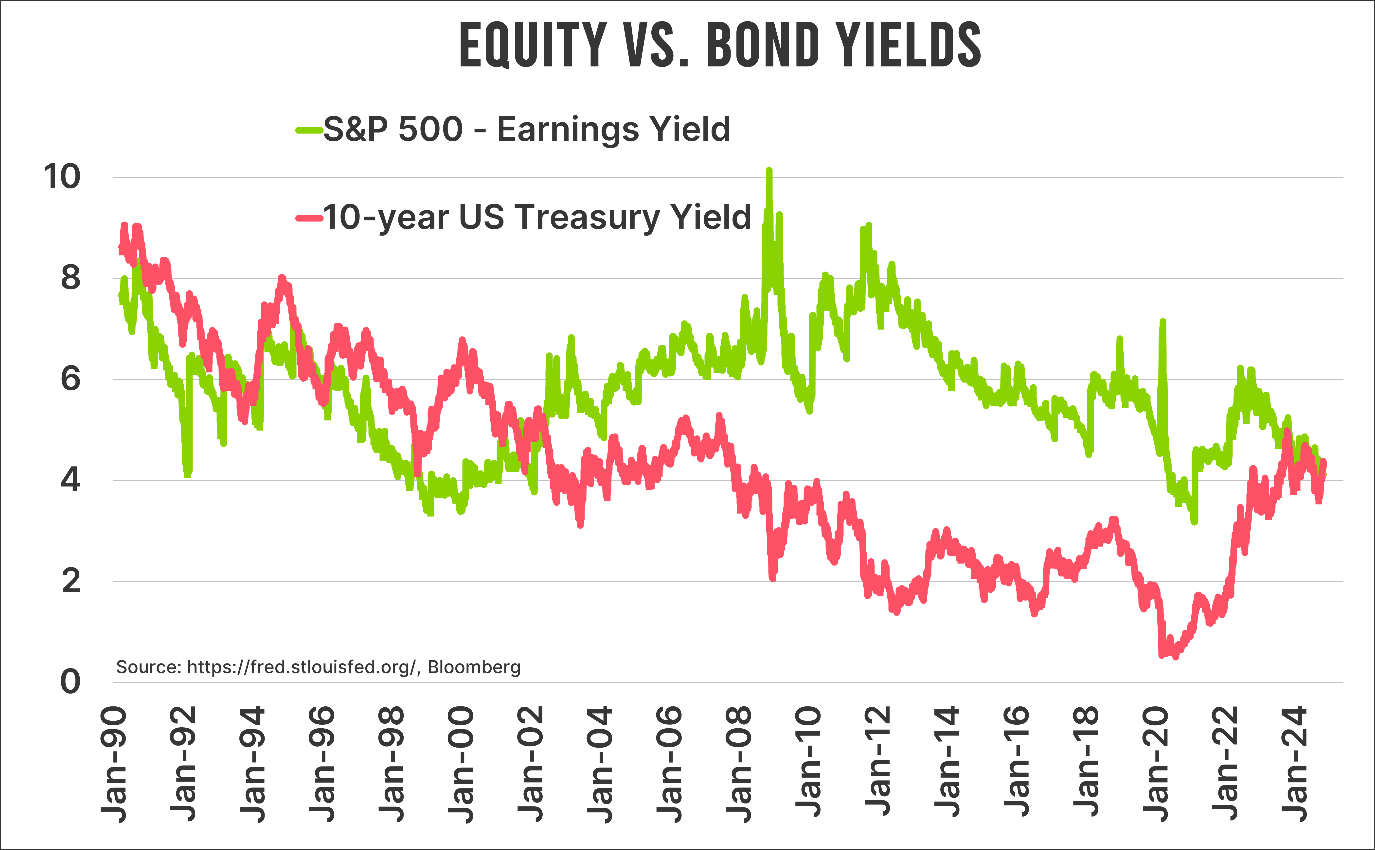

A relative concept

Below is the earnings yield, or the inverse (forward) P/E ratio, of the S&P500 Index, plotted against the U.S. 10-year treasury yield.

While this graph doesn’t capture all valuation aspects relevant for stocks and bonds, it provides a solid conceptual basis. What (implicit) yields should I expect from my investment? Before the Global Financial Crisis, the earnings yield and the treasury yield were reasonably aligned. This was also true before 1990.

Since the Global Financial Crisis and extending well beyond the Covid crisis, stocks have been, at least according to this graph, dirt cheap. This has everything to do with the vast central bank intervention we’ve seen to counter those crises. Ultra-low interest rates have become a standard feature of monetary crisis management.

As a result of the largest inflation crisis since the early 1980s—also due to expansive central bank policies—the current interest rate stands at 4.32 percent. Hardly a bonanza, if you consider this rate in historical context. And it’s also not higher than the current earnings yield of the S&P500 Index. From this perspective, it’s difficult to argue that stocks are expensive.

Where to next?

I want to add two points to the conclusion above. Firstly, we’re looking here at the relatively “most expensive” stock market, the S&P500 Index, compared with the highest interest rate in Western economies. In Europe, the earnings yield of the Stoxx 600 Index stands at 6.9 percent against an average interest rate of, let’s say, 3.0 percent. In Japan, the earnings yield of the Nikkei Index is 4.7 percent against a ten-year yield of less than 1 percent.

Secondly, where do you think interest rates are headed? I estimate a high likelihood that rates will start declining from here. Short-term rates are already dropping sharply, limiting the upside potential of longer-term rates. And since governments are likely to continue with unsustainable fiscal policies, central banks stand ready to suppress rates if needed. No one knows exactly how the ECB’s Transmission Protection Instrument (TPI) works, but it’s prepared and ready for “if”.

I wouldn’t go as far as to say that stocks are “cheap,” but compared to bonds, it doesn’t seem fair to call them wildly overpriced, as many gurus do.

Jeroen Blokland analyses striking, timely charts on financial markets and macroeconomics in his newsletter, The Market Routine. He is also the manager of the Blokland Smart Multi-Asset Fund.