Since the end of the Cold War in 1991, Europeans have lived largely free from the fear of major conflict. That all changed on 24 February 2022, when Putin’s army invaded neighbouring Ukraine.

Investors are spotting opportunities in defence companies, particularly given the continued military support for Ukraine and significant increases in European defence budgets. Long-term revenue prospects appear stable, driven by the ongoing maintenance of military equipment and the need to replenish supplies.

From the escalation of the Ukraine war in February 2022 through to the end of August 2024, the Morningstar Global Aerospace and Defence Index has returned around 57%, significantly outperforming the broader Morningstar Global Markets Index, which gained 26%.

This index covers companies that manufacture tanks, fighter jets, missiles, and defence systems, including Lockheed Martin and the UK’s BAE Systems, as well as aircraft makers like Airbus and Boeing, and engine producer Rolls-Royce. GE Aerospace and RTX Corp (formerly Raytheon Technologies) are index heavyweights, with a weighting of over 10%. RTX Corp not only manufactures aircraft engines but also air defence systems, satellites, and drones.

However, not all parts of the sector are as predictable in terms of revenue. For instance, sales of ammunition and other direct supplies to the Ukrainian army may fluctuate depending on political dynamics, which could lead to sudden drops in revenue.

Increased defence budgets

The Ukraine war, now dragging on for over two years, has contributed to a broader sense of geopolitical insecurity. This is compounded by other conflicts, such as those in Gaza and Lebanon, rising tensions between China and Taiwan, and disputes in the South China Sea between China, Vietnam, the Philippines, and Malaysia, a vital maritime trade route.

After years of defence budget cuts, European countries are now ramping up spending. The Dutch military, for example, will see significant increases in funding in the coming years, with a budget of 21 billion euro’s for 2024, bringing it close to NATO’s benchmark of 2% of GDP. In contrast, Belgium, with just 1.1% of GDP allocated to defence, remains at the bottom of the NATO list.

ESG considerations?

Ethical issues surrounding the defence sector remain a topic of debate. Advocacy groups are seeking to shake off the negative stigma attached to the industry, while politicians are pushing to mobilise institutional capital in favour of domestic defence industries.

Before the Ukraine war, most (sustainable) investors avoided companies that produce weapons. While this principle still holds for many, some investors are rethinking their stance, with the argument of self-defence gaining more traction. This has created a grey area around defence investments: when are weapons used for attack, and when for defence? Nevertheless, investing in controversial weapons, such as anti-personnel mines or nuclear, biological, or chemical weapons, remains unacceptable.

ETF differences

There are relatively few options for directly investing in this sector through (active) funds, largely due to exclusion criteria. However, ETFs such as the iShares Global Aerospace & Defence UCITS ETF and the VanEck Defence UCITS ETF are available.

The differences between these two trackers are significant, as they follow different indices. iShares tracks the S&P Developed BMI Select Aerospace & Defence 35/20 Capped Index, while VanEck follows the MarketVector Global Defence Industry Index. As a result, the two ETFs only share 19 holdings (less than 10% overlap), despite iShares holding 57 positions and VanEck 28. Palantir Technologies, the largest position in the VanEck ETF, is a software company co-founded by Peter Thiel, and not part of the iShares tracker.

Conversely, RTX Corp, Lockheed Martin, or Safran are absent from VanEck, which claims to give investors access to leading companies in defence technology, cybersecurity, and defence-related suppliers. iShares focuses on aerospace and defence stocks as classified by the GICS sector.

Fund radar

Strategies that appear prominently on Morningstar’s radar are judged by fund analysts to have strong management teams and robust investment processes. Alternatively, Morningstar’s algorithm may assign these qualities based on the same framework used to evaluate funds.

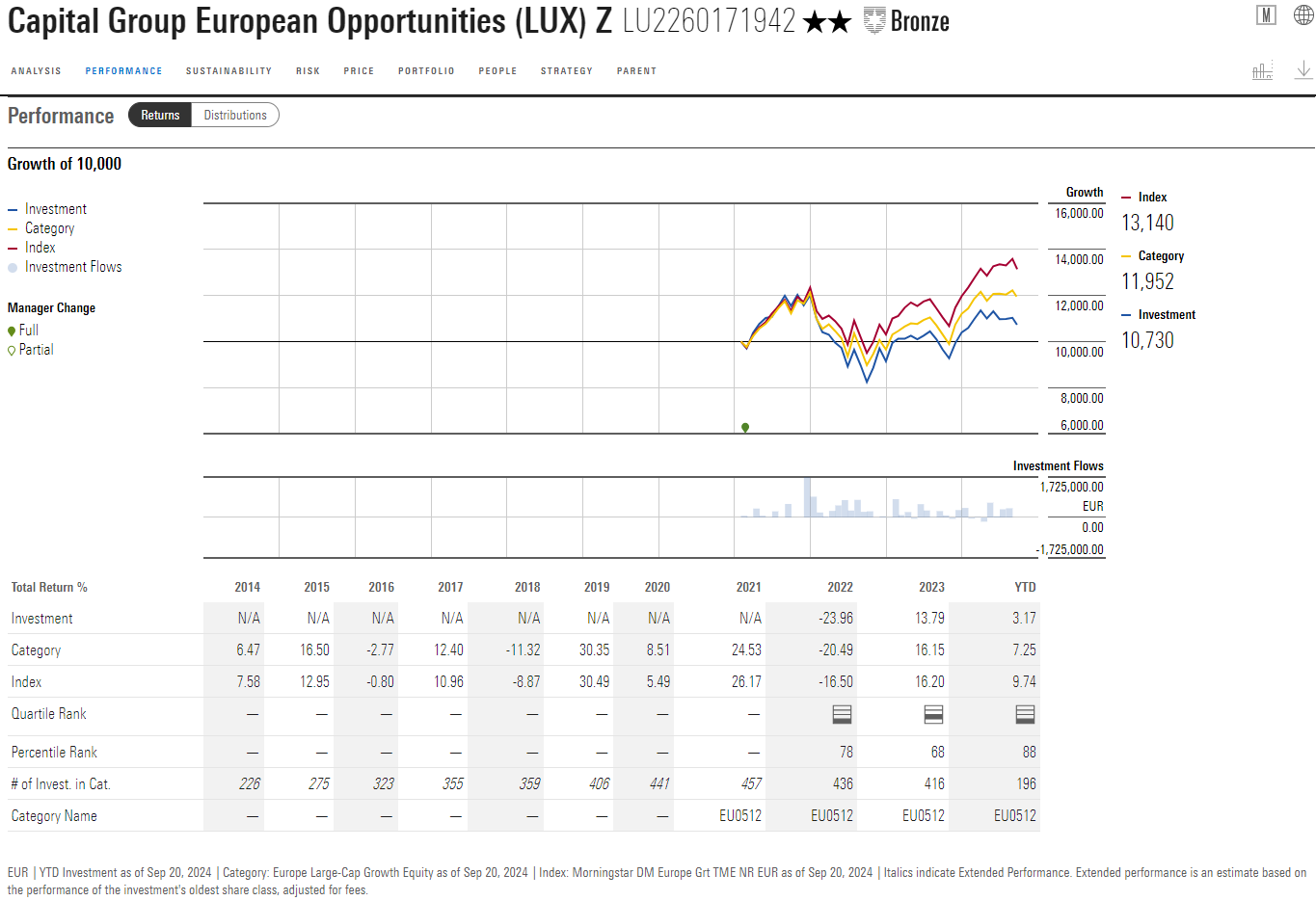

The Capital Group European Opportunities fund is a broad European equities fund but stands out with over 10% exposure to the aerospace and defence sector, with BAE Systems as its largest holding. Last year, the managers added Melrose but took profits in Rheinmetall.

Although this fund only launched in February 2021, the underlying strategy has been in use since 1992, making the track record of the fund itself less relevant. Michael Cohen has been the longest-serving manager (since 2017), while Lawrence Kymisis and Patrice Collette replaced former manager Philip Winston in July 2020. While the team has seen significant changes in recent years, each of the three managers has two to three decades of investment experience. Capital Group’s multi-manager approach reduces the risk of key-person dependency and limits disruption from any managerial departures.

Cohen oversees the strategy but generally does not interfere with the portfolios of the other managers. They focus on investing in high-quality European growth companies with robust business models, competitive advantages, and strong management teams. Collette is willing to invest in out-of-favour companies, while her colleagues focus more on growth. The combination of different portfolios and styles provides a degree of diversification, but the strategy has been more volatile than the MSCI Europe Growth Index.

In recent years, the mandate has expanded to allow for more flexibility in market capitalisation and to invest in emerging European companies. With relatively limited assets, the strategy remains quite nimble, allowing managers to take meaningful positions in small-cap companies, something Cohen has capitalised on.

Thomas De Fauw is a manager research analyst at Morningstar. Morningstar analyses and rates investment funds based on quantitative and qualitative research. Morningstar is part of Investment Officer’s expert panel.