Individual investors, especially Dutch investors, continue to have unwavering confidence in oil company Shell, according to recent research by De Nederlandsche Bank. This makes Shell still a cornerstone in many investment portfolios. However, professional investors view (fossil) energy stocks very differently.

By the end of June, Dutch households held €5 billion worth of Shell shares, making it the company in which Dutch households had invested the most capital. This perspective contrasts sharply with that of many professional investors, who systematically underweight energy stocks in their portfolios or exclude them entirely due to sustainability concerns.

Since 2012, the energy sector has gradually lost its weight in the Morningstar Global TME Index. Twelve years ago, energy stocks accounted for around 12% of the index, but by 2024, this has shrunk to less than 5%. A temporary low point was reached in 2020, with energy comprising just 2.9% of the index.

Despite the sector’s diminished weight over the past twelve years, fund managers in the Morningstar global large-cap blend equity category have been even more sceptical about the future resilience of these companies. Since 2013, the sector has been structurally underweighted in global investment portfolios, with an average of just over 3% of fund assets allocated to the oil and gas sector as of the end of July.

The cyclical nature and capital intensity of the sector are among the reasons fund managers avoid oil and gas companies. The dependency on volatile energy prices, geopolitical tensions, and the dominant role of the OPEC oil cartel make the sector unpopular among fund managers. Additionally, the growing focus on sustainability has driven a reduction in exposure to fossil fuels. Of the approximately 2,200 investment funds in the Morningstar global large-cap blend equity category, more than 700 formally exclude fossil fuels.

However, for global dividend funds, the energy sector remains an important source of income, giving it a more prominent position in some portfolios. And within these, there are some interesting strategies.

Fund Radar

The strategies that feature prominently on Morningstar’s radar either boast a solid management team and investment process, as judged by fund analysts, or are rated highly based on an algorithmic evaluation using the same criteria. In this edition, we highlight a globally investing dividend fund with above-average exposure to the energy sector.

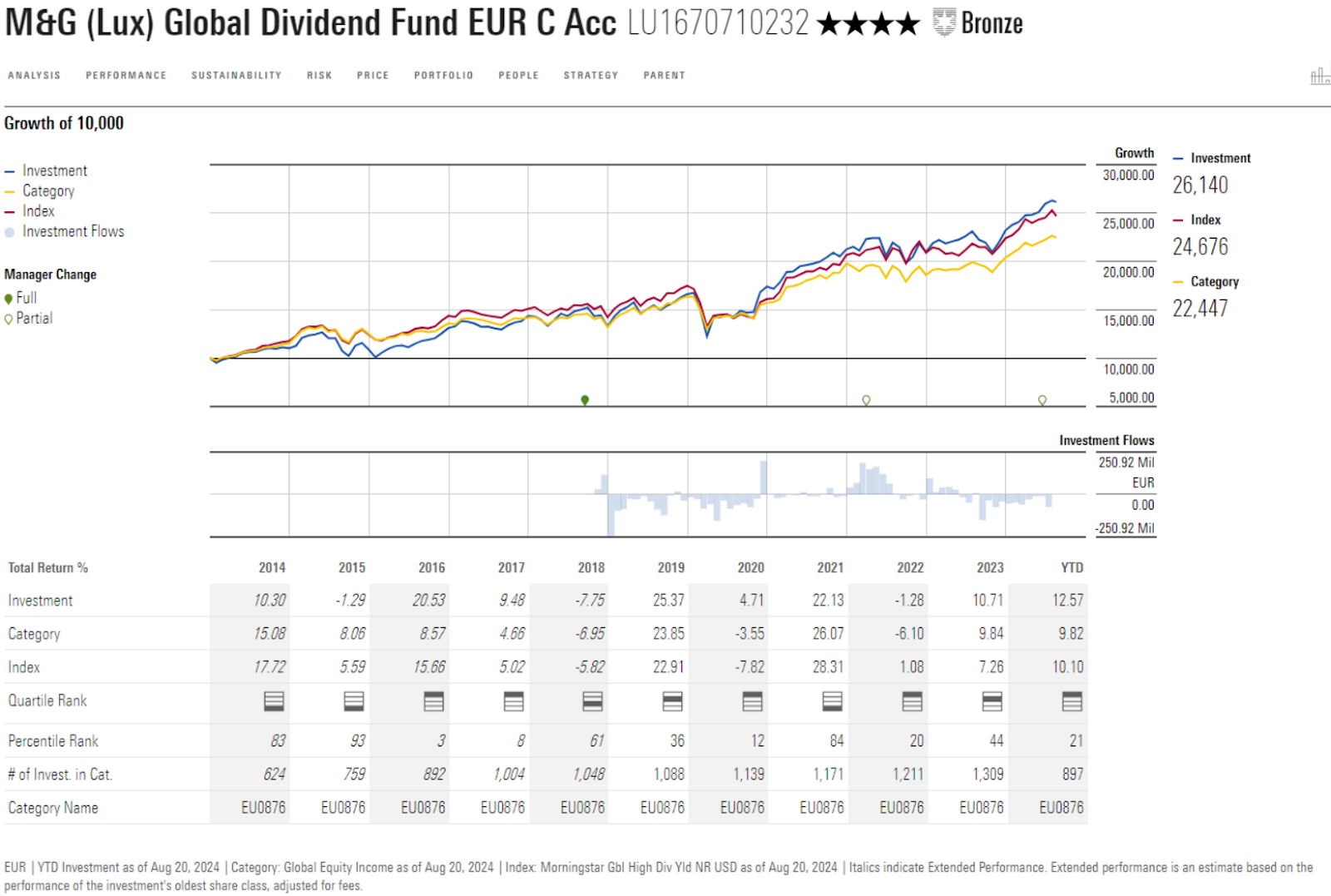

For a long time, the energy sector has been a key pillar for the M&G (Lux) Global Dividend fund, which holds an Above Average Pillar rating for both People and Process. While global equity funds have systematically underweighted the sector since 2013, fund manager Stuart Rhodes has done the exact opposite. In 2014, exposure to the sector peaked at nearly 19%. Although the sector weight in the portfolio has decreased to just over 11% as of July 2024, this remains significantly higher than in the global equity index and contrasts with what many other global investment funds have done.

Rhodes opts not for the major oil companies, but for midstream companies like Keyera and Gibson Energy, which are active in energy transport via pipelines, oil storage facilities, and refining. These two companies have long been a cornerstone of the portfolio, with Rhodes having been a shareholder for over 10 years.

Exposure to the sector has caused headaches at times, especially in 2014 and 2015. The impact of a shaky oil price cost the fund 5% in performance at the time, with positions in Prosafe, Seadrill, and Gibson Energy causing the most damage. This prompted Rhodes to publicly apologise to investors in the fund through a letter, acknowledging the underperformance, the mistakes he made, and the lessons he learned. This level of honesty and humility is rarely seen in the fund industry.

It’s one of the qualities that Morningstar analysts appreciate in Rhodes. His long track record since the fund’s inception in 2008 has established him as a seasoned dividend investor. Under his leadership, he has skillfully navigated the fund through various economic cycles, remaining true to his investment philosophy and principles, which, given the potentially volatile nature of the strategy, demonstrates discipline and resilience. He also sometimes goes against the grain with his choices of specific companies or sectors. Over the years, he has showcased his investment talent at crucial moments.

The team supporting Rhodes has seen some changes in recent years. Co-manager Chris Youl left for another M&G fund, leaving Rhodes now managing the strategy alongside Kathryn Leonard. They draw on ideas generated within the broader dividend team and can also use M&G’s central analyst team as sparring partners.

Due to the focus on dividend growth, the portfolio’s dividend yield is generally lower than that of its peers, and it shows a milder value tilt compared to competitors. Rhodes selects a compact portfolio of 40-50 stocks based on bottom-up fundamental analysis, dividing the portfolio into three segments: assets, quality, and rapid growth.

However, this strategy is not for risk-averse investors. The portfolio is concentrated in its top holdings, with the 10 largest positions making up roughly half of the portfolio. Moreover, the strategy holds a larger stake in smaller companies like Methanex, Trinseo, and Gibson Energy, increasing liquidity risk.

Exposure to cyclical sectors, combined with a clear preference for mid- and small-caps, can heighten volatility. Although investors have been compensated for the higher risk, they must be prepared to endure periods of erratic and poor relative performance to reap the long-term benefits.

Jeffrey Schumacher is director manager research at Morningstar Benelux. Morningstar analyses and evaluates investment funds based on quantitative and qualitative research. Morningstar is an Investment Officer knowledge partners and takes an analytical look at a specific category of investment funds every Friday.