After a decade in the shadows, global macro hedge funds are reclaiming the spotlight. As market volatility resurges, professional money managers are eyeing global macro as a cornerstone of their hedge fund strategies.

Macro strategies have historically struggled to deliver consistent returns during periods of low volatility, and the 2010s were not kind to them. Now, with volatility back on the menu, investors believe global macro strategies are back in business.

Unlike traditional stock-pickers, who take a bottom-up approach to individual companies, macro managers focus on big-picture economic and political trends. Their ability to trade across multiple asset classes, including equities, bonds, currencies, and commodities, allows them to profit from major market shifts.

“The new regimes and policy changes in the US and Europe are creating volatility and trading opportunities,” said Tom Wrobel, Director at Societe Generale’s prime brokerage unit. Higher rates and persistent inflation provide fertile ground for these strategies, he said in an interview with Investment Officer.

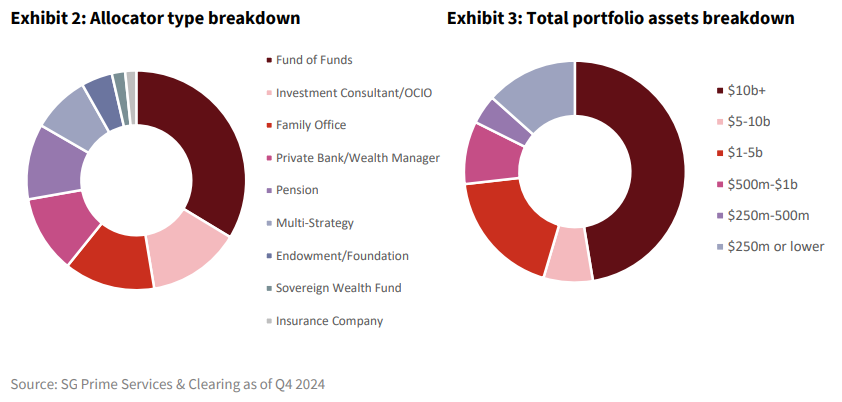

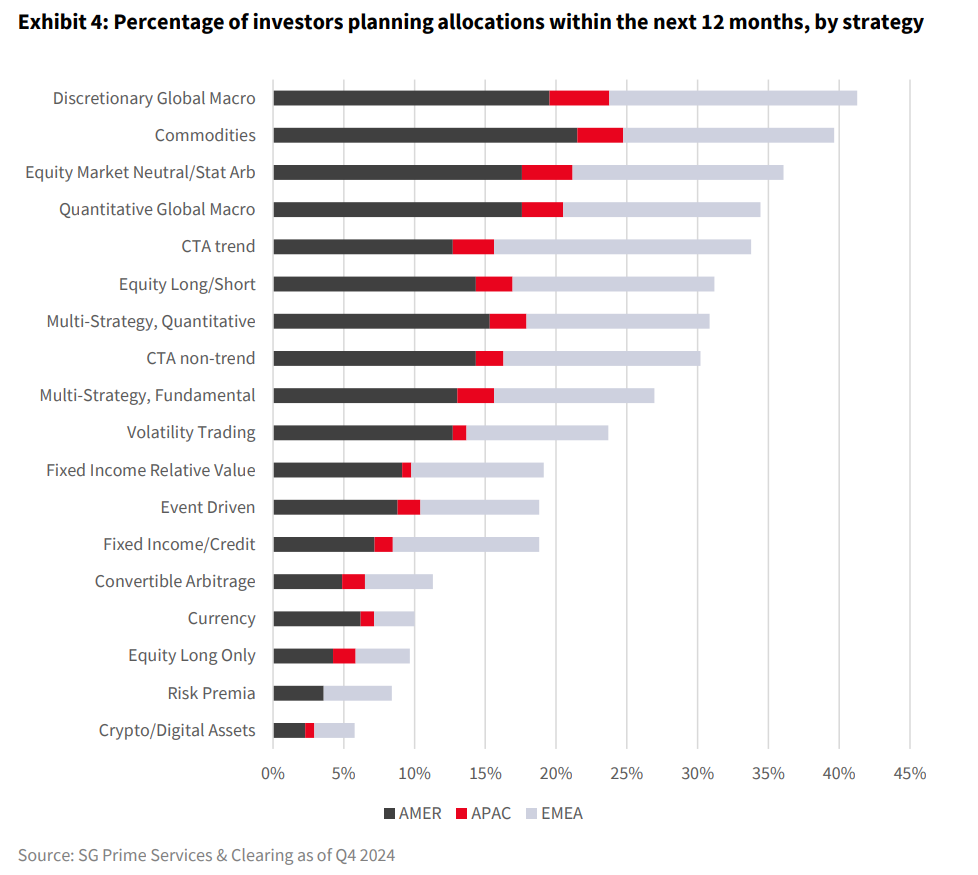

According to Societe Generale’s latest survey of 239 investment firms, global macro strategies ranked first in a list of hedge fund strategies that investors around the world want to employ in 2025. Crypto ranked last.

According to Wrobel, macro managers are zeroing in on three key areas: geopolitical dislocations, high interest rates, and inflation. “Macro strategies are particularly well-suited for the current environment,” he said. “They’re not just taking directional bets, they’re also exploiting relative value opportunities across asset classes.”

Institutional investors have long prioritized resilience and diversification, yet their portfolios often circle back to U.S. equities. With the S&P500 delivering annualized net gains of more than 10 percent over the last decade, the allure of a proven performer has been hard to resist. However, stretched valuations are forcing a re-evaluation.

At a forward price-to-earnings ratio near 22, the S&P500 appears expensive by historical standards. The Nasdaq, dominated by high-growth tech giants, trades at even loftier multiples. This raises doubts about whether U.S. equities can maintain their stellar track record. Meanwhile, equity markets in other regions offer little refuge, with lackluster growth prospects and subdued investor sentiment making them unappealing alternatives for most institutions.

“Investors are realizing the need for more resilient portfolios that can adapt to changing market dynamics,” said Wrobel. The once-reliable 60/40 portfolio, a staple of institutional investing, is under scrutiny. Bonds, traditionally seen as a counterbalance to equities, have faced negative returns in recent years, and their historically negative correlation with stocks has weakened. “This shift challenges their role as a hedge in balanced portfolios,” Wrobel noted.

New funds

In the Netherlands, new players emerge. Palinuro Capital, a new global macro hedge fund founded by Alfonso Peccatiello, will launch on the 13th of January with nearly 100 million dollars in investor commitments. Peccatiello, the founder of the newsletter The Macro Compass, previously managed a 20 billion dollar portfolio at ING.

“Many investors are drawn to hedge funds not just for returns but for the value of direct access to managers,” Alfonso Peccatiello told Reuters ahead of Palinuro Capital’s launch. “Having the opportunity to engage, review research, and ask questions is a significant advantage,” he said.

Lombard Odier too launched a new Global Macro strategy this year. Traditional diversification has its limits in volatile markets, according to Didier Anthamatten, Portfolio Manager at Lombard Odier Investment Managers.

“Our DOM Global Macro strategy aims to deliver steady returns by reducing reliance on equities and bonds, providing stability in uncertain conditions”, he told Investment Officer in an email.

Critique

Critics of macro strategies say they are notoriously complex, with returns too low to justify high fees. Global macro strategies, alongside statistical arbitrage, command the highest average fees in the hedge fund industry, according to Aurum’s Hedge Fund Data Engine.

The very factors that make them appealing like volatility, uncertainty, and geopolitical tension, also make them risky. Funds positioned on the wrong side of major moves often face steep losses.

During Russia’s invasion of Ukraine in early 2022, many macro funds were heavily long on Russian and Ukrainian assets. These positions were underpinned by strong fundamentals and a positive outlook on commodities, until the geopolitical upheaval rendered those bets catastrophic.

Similarly, the collapse of Silicon Valley Bank in March 2023 blindsided several macro managers, like Graham Capital Management. Despite their focus on macroeconomic trends, few are prepared for the ripple effects of sudden unforseen events.

Performance

Despite the challenges, 2024 was a banner year for many macro-focused hedge funds. Discovery Capital, a prominent global macro fund, led the pack with a remarkable 52 percent gain in 2024. The fund’s success stemmed from strategic bets across multiple asset classes in both emerging and developed markets, according to a Reuters report.

Bridgewater Associates, the world’s largest hedge fund, also staged a comeback. Its flagship Pure Alpha 18 percent Volatility fund posted an 11 percent gain, a marked improvement from its subdued performance in prior years.

D.E. Shaw & Co., typically recognized for its quantitative strategies, demonstrated the growing appeal of macro investing as well. While its flagship Composite fund delivered a robust 18 percent gain, the more macro-focused Oculus fund achieved a staggering 36 percent return, its best annual performance to date.

Societe Generale’s survey report found that funds trading in commodities and equities ranked second and third in terms of investor interest. This reflects a growing understanding of the need to build what Wrobel calls “storm-resistant” portfolios.

“It’s no longer just about sticking to a strict 60/40 split. Bonds still have a role, but they’re now accompanied by other assets designed to create more resilience and diversification,” Wrobel said.