A strong start to the year for smallcaps does not guarantee outperformance in 2026.

Smallcaps started 2026 strongly, outperforming largecaps over the first two months. However, history suggests caution: in the past fifteen years smallcaps beat largecaps at the start of the year most of the time, yet often still ended up lagging over a full twelve months. Over the past decade, global largecaps have delivered a roughly 12 percent annualized return, while smallcaps lagged by around 2 percentage points. That has been particularly disappointing as smallcaps lagged even in conditions that traditionally favor them, including economic growth, falling interest rates and market recoveries.

Much of the gap stems from the outsized performance of the Magnificent Seven and other AI‑driven largecap stocks in 2023 and 2024. Structural factors also contribute to the gap: the global smallcap index has less US exposure, and smallcaps are underrepresented in technology, which is the decade’s strongest‑performing sector. Quality divergence is another factor. Morningstar data shows declining profitability and financial health among smallcaps, partly because the most promising small firms increasingly stay private or get bought out by private equity. Despite this, valuations are historically attractive today, particularly in Europe.

Against this backdrop, we compare two Morningstar analyst-rated funds in the global small- and midcap equity category: BGF Systematic Global Small Cap and MFS Meridian Global New Discovery.

People

BGF Systematic Global Small Cap is run by Blackrock’s Systematic Active Equity group, a quantitatively-driven platform with deep machine‑learning and data‑science resources. Its leadership, consisting of Kevin Franklin, Raffaele Savi and Richard Mathieson, has long tenures within Blackrock and oversees a sizable team of more than eighty quantitative and research analysts. The team shares responsibility for model development, data testing and idea generation, reflecting a highly collaborative and technologically intensive process.

By contrast, MFS Meridian Global New Discovery is led by four fundamental stock-pickers: Peter Fruzzetti, Michael Grossman, Sandeep Mehta and Eric Braz. They rely on deep company-level research supported by roughly 75 global analysts. Their process emphasizes unanimous decision-making, ensuring that only high-conviction ideas enter the portfolio. The team blends regional expertise (London- and US-based members) and maintains strong alignment with investors through personal investments and MFS’ long-term compensation structure.

Overall, both teams are seasoned and well-resourced. BGF warrants a People Pillar rating of Above Average, while MFS Meridian team’s experience, cohesion and deep research support a High rating.

Process

BGF Systematic Global Small Cap employs a fully quantitative, signal-driven approach that blends traditional factors with a large and expanding set of nonstandard inputs, including machine-learning-derived sentiment signals and alternative data such as natural language processing (NLP) outputs and web-traffic indicators. Its model dynamically adjusts signal weights, with the balance between machine learning and human overlay shifting meaningfully over time. Daily alpha forecasts, high portfolio turnover, and optimizer-based construction characterize a process designed for systematic breadth rather than deep individual company assessment.

MFS Meridian Global New Discovery is a fundamentally driven, research-intensive strategy that emphasizes sustainable earnings growth, competitive advantages and strong governance. Portfolio managers rely heavily on MFS’ global analyst network, applying valuation discipline and independently formed conviction to build a diversified, bottom-up portfolio. Position sizing is conservative, risk management is central, and capacity considerations are monitored.

BGF’s quantitative process uniquely combines traditional and nonstandard signals (machine learning). It earns an Average rating on the Process Pillar, supported by evidence of more consistent and stable implementation after post-2020 process changes had bedded down in recent years. Meanwhile, MFS earns an Above Average rating given its robust process where risk management is a strength.

Portfolio

BGF’s benchmark‑aware approach keeps country and sector weights close to its MSCI ACWI Small Cap Index while seeking alpha primarily through broad security selection. Its portfolios are very large and diverse, typically holding 500 to 2000 names, with position sizing driven by optimization and risk-control frameworks. Meanwhile, its top 10 concentration accounts for only 6.5 percent of assets, including SanDisk, Nomura Real Estate Holdings and Bright Horizons Family Solutions. This is almost double the weight of the category’s benchmark, but a fraction of the 28 percent average of its peers. Despite being systematic, the strategy incorporates significant manager discretion, especially in choosing and weighting signals. This can lead to substantial shifts in portfolio construction, such as doubling the number of holdings during the covid‑19 market dislocations.

MFS Global New Discovery adopts a fundamental, high‑conviction growth-oriented approach with a far more concentrated portfolio of around hundred stocks. The team emphasizes businesses with structural growth, high returns on capital, and typically avoids the smallest, least liquid companies. Sector tilts, such as toward industrials and away from financials and utilities, reflect long-term fundamentals rather than benchmark alignment. MFS also carefully manages capacity and liquidity, using disciplined position sizing to maintain flexibility, through disciplined position sizing, diversification, and limited use of the most illiquid areas.

Performance

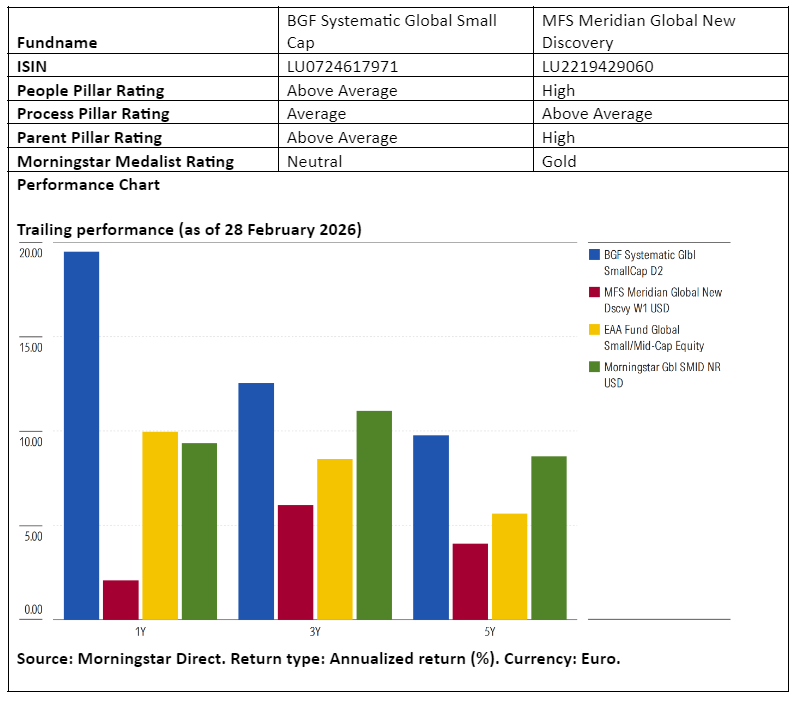

Both funds have respectable long‑term records, yet their performance patterns diverge meaningfully. BGF has delivered consistent peer‑relative outperformance, especially over the past three to five years, with strong stock selection, recently in technology, driving results. Its sentiment and fundamental signals have been key contributors, helping it beat both the index and peers through varied market environments.

Meanwhile, MFS New Discovery, with its quality‑growth orientation, has faced headwinds since 2021 as markets favored momentum and lower‑quality names. While its long‑term results remain solid and ahead of many quality‑growth peers, shorter‑term returns have lagged, pressured by adverse factor trends and numerous small stock picking detractors.

Ronald van Genderen is a senior manager research analyst at Morningstar. Morningstar analyzes and rates investment funds based on quantitative and qualitative research. The firm is a member of Investment Officer’s expert panel.