Germany’s economy has struggled for momentum in recent years, weighed down by structural headwinds and weak growth, yet its stock market has told a very different story.

Over the past several years, the German economy has struggled to regain sustained momentum, underperforming much of the rest of Europe. Structural headwinds, including high energy costs after the Ukraine war, weak global manufacturing demand, slowing Chinese growth, and persistent bureaucratic and investment bottlenecks, have weighed heavily on Germany’s export‑ and industry‑driven model. GDP growth has been flat to weak since 2022, with Germany often labeled the “sick man of Europe” once again, while countries such as Spain, France, and parts of Southern Europe have benefited from services, tourism, and EU investment programs.

Against this challenging macro backdrop, financial markets have told a more optimistic story. German equities have delivered solid returns in recent years. While the Ukraine war weighted initially on the performance of the German stock market, it has rebounded strongly registering an outperformance versus the broader European markets in 2023, 2024 and 2025. This strong performance was driven by mainly three companies which each benefited from different market trends: Siemens Energy (energy transition), Rheinmetall (increase in defense spending) and Commerzbank (improved rates environment).

Against this backdrop, we assess two strategies in the Morningstar Category Germany Equity that are covered by Morningstar analysts: DWS Invest German Equities and Fidelity Germany.

People

Both DWS Invest German Equities and Fidelity Germany carry Average People Pillar ratings, due to manager transitions that introduce uncertainty; however, the nature of these changes differs meaningfully.

DWS Invest German Equities has undergone deeper and more disruptive turnover since 2023. The departure of long-tenured manager Tim Albrecht, followed by the exit of his successor Marcus Poppe and several other experienced team members, has materially altered the team. Current managers Philipp Schweneke and Andreas Wendelken bring long DWS tenures and broad portfolio-management experience, though much of it lies outside German equities. A key concern is Schweneke’s heavy workload, as he retains multiple leadership and portfolio management responsibilities. Positively, the team has moved toward a more collaborative decision-making structure for DAX 40 exposure, which reduces key‑person risk. Still, the German equity team is leaner than before and must prove stability and effectiveness over time.

Fidelity Germany, by contrast, reflects a more orderly succession. Leadership passed internally to Tom Ackermans in September 2023, with former lead manager Christian von Engelbrechten remaining nearby and informally involved. This continuity supports investment debate and process stability. However, Ackermans’ limited track record as lead manager, with most of his experience stemming from analyst roles and a relatively recent comanager position, temper our conviction. Fidelity’s strength lies in its substantial European research platform, which mitigates execution risk despite Ackermans’ shorter history.

Process

Both strategies rely on fundamental, bottom‑up stock selection, complemented by risk controls, but differ in maturity and conviction.

DWS Invest German Equities is in a transition phase, supporting an Average Process Pillar rating. Under Albrecht, the strategy followed a bold, often contrarian approach, actively adjusting net equity exposure, including leverage, based on top‑down views. The current managers retain some flexibility but apply it more cautiously, with tighter limits on leverage and a clearer focus on downside resilience. Stock selection continues to emphasize earnings and cash‑flow growth, assessed through structured analysis and valuation discipline. Top‑down inputs remain relevant but are now more closely anchored to DWS’ house view, reducing discretion versus the past.

Fidelity Germany follows a more established and proven process, supporting an Above Average Process Pillar rating. Fundamental research sits at the core of the approach, drawing heavily on Fidelity’s large European analyst team. The strategy emphasizes quality, balance‑sheet strength, and sustainable growth, while applying pragmatism around valuation and risk management. Compared with DWS, Fidelity’s process is less top‑down shows lower reliance on exposure management, with stronger evidence of consistency across market environments.

Portfolio

Both portfolios reflect the concentrated nature of the German equity market but differ clearly in portfolio construction and activeness.

DWS Invest German Equities holds 40–60 stocks and has historically differentiated itself through active management of net equity exposure, including leverage and futures. While this added tactical flexibility, regulatory constraints and the dominance of mega‑caps like SAP limit stock‑level conviction, resulting in a low active share of around 30 percent. Small‑ and mid‑cap exposure, once meaningful, has declined, and the portfolio has recently moved closer to the benchmark as leverage was removed.

Fidelity Germany runs a more concentrated 30–45 stock portfolio, with the top 10 accounting for about 60 percent of assets. Conviction is expressed primarily through bottom‑up stock selection, delivering a higher active share of 40 percent–60 percent. Compared with DWS, Fidelity exhibits clearer style expression through its growth bent, higher stock‑specific risk, and greater flexibility, including limited investments outside Germany.

Performance

Both strategies have credible long‑term performance records but differ in consistency and recent momentum.

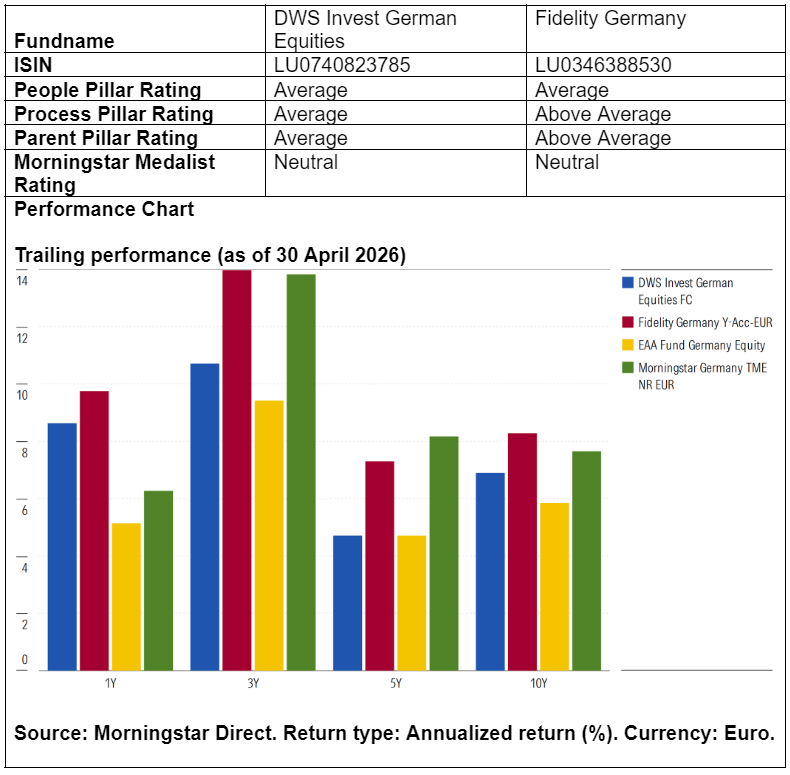

DWS Invest German Equities generated strong long‑term outperformance under Albrecht, albeit with elevated volatility. Since 2018, however, bold positioning, leverage, and persistent underweights in index heavyweights such as SAP and Rheinmetall have weighed on relative returns, particularly during 2022–24. Recent performance has lagged benchmarks, though it remains ahead of peers.

Fidelity Germany has delivered more consistent long‑term outperformance, supported by lower volatility and stronger downside protection. While post‑pandemic style headwinds affected both strategies, Fidelity’s results have held up better overall. Under Ackermans, performance has been respectable, but the short lead‑manager track record warrants continued monitoring.

Ronald van Genderen is a senior manager research analyst at Morningstar. Morningstar analyzes and rates investment funds based on quantitative and qualitative research. The firm is a member of Investment Officer’s expert panel.