Emerging markets started the year strongly, but geopolitical tensions stemming from the US/Israel–Iran conflict have since tempered sentiment.

Global emerging markets started the year on a very strong footing. The Morningstar Emerging Markets TME Index rose steadily and convincingly to a gain of more than 13 percent by the end of February 2026, representing an outperformance of roughly 10 percentage points versus developed markets, as measured by the Morningstar Global TME Index. The rally was led by South Korean equities, which gained more than 56 percent in the first two months of 2026, following an exceptionally strong 2025 in which the South Korean market advanced nearly 75 percent. Performance was primarily driven by technology-related companies such as index heavyweights Samsung Electronics and SK Hynix, although Hyundai Motor proved to be an even stronger performer over the period.

However, the rapid escalation of the US/Israel–Iran conflict triggered a sharp shift in sentiment, sparking a broader market downturn and renewed risk aversion that weighed heavily on emerging markets. In March, emerging market equities fell by nearly 11 percent, while developed markets proved more resilient, limiting losses to around 5 percent. South Korean stocks declined approximately 24 percent, faring the worst among emerging markets. While profit-taking after the prior strong gains likely played a role, the country’s high dependence on oil imports was also a key factor, as was the case for other weak-performing markets such as South Africa, Indonesia, India and Taiwan.

Against this backdrop, we assess two strategies in the Morningstar category Global Emerging Markets Equity covered by Morningstar analysts and have historically adopted distinct approaches to South Korea: Invesco Emerging Markets Equity and First Sentier Stewart Investors Global Emerging Markets Leaders.

People

Both Invesco Emerging Markets Equity and First Sentier Stewart Investors Global Emerging Markets Leaders earn Above Average People ratings, reflecting experienced leadership, strong team support, and collaborative cultures, but they differ in structure, continuity dynamics and decision-making.

Invesco benefits from long-standing team stability and internal continuity. Lead manager Charles Bond has progressed internally over more than a decade and operates within a tightly integrated Asia and emerging markets team of 10 professionals who have largely worked together for many years. The team follows a shared philosophy and manages multiple regional and emerging-markets strategies with significant portfolio overlap, with Bond primarily implementing collective views while retaining limited discretion.

By contrast, First Sentier’s strategy has undergone a recent but well-managed leadership transition following the dissolution of Stewart Investors, effective November 14, 2025. As part of this change, Rasmus Nemmoe assumed the lead role and holds final decision-making authority, working alongside comanager Rizi Mohanty. While the handover introduces less continuity than at Invesco, Nemmoe’s long and successful track record in emerging markets and alignment with FSSA’s quality-focused philosophy mitigate transition risk. FSSA’s larger analyst team of 16 places stronger emphasis on structured debate, succession planning, and embedded incentives such as profit sharing and co-investment.

Process

Both strategies are underpinned by robust, well-articulated investment processes that merit an Above Average Process assessment, but they differ meaningfully in philosophy and implementation. Invesco prioritizes valuation opportunity and contrarian ideas, whereas First Sentier emphasizes quality, capital preservation, and sustainability-led discipline.

The Invesco strategy is valuation-driven and unconstrained, aiming to identify mispriced companies trading at a significant discount to internally assessed fair value. It relies on systematic screening, detailed fundamental analysis, and explicit ranking of stocks by expected total return, with a willingness to exploit both long-term opportunities and short-term valuation anomalies. While nominally style-agnostic, its contrarian valuation focus tends to result in a modest value tilt.

Meanwhile, the First Sentier approach is quality-focused and explicitly risk-aware, defining risk as permanent capital loss rather than relative underperformance. It follows a bottom-up, buy-and-hold philosophy, emphasizing strong franchises, high returns on capital, financial resilience, and, critically, management integrity. The strategy is prepared to pay premiums for exceptional businesses and incorporates hard sustainability exclusions (controversial products such as alcohol, tobacco and gambling), alongside a clear largecap focus.

Portfolio

Both strategies are concentrated, high‑conviction emerging markets equity portfolios, but they differ meaningfully in how they express conviction and manage risk. Invesco Emerging Markets Equity runs an unconstrained, valuation‑driven portfolio of around 50 stocks, where position sizes are primarily determined by the perceived gap between market price and intrinsic value. While mindful of benchmark risk, the approach is explicitly not benchmark‑driven. Country positioning reflects bottom‑up valuation opportunities, exemplified by notable and structural overweights in Brazil, South Korea, and dominant semiconductor names in Taiwan and Korea, supported by attractive valuations, dividends, and structural earnings drivers.

First Sentier Stewart Investors Global Emerging Markets Leaders is even more concentrated, with 35-45 holdings and a high active share, reflecting a benchmark‑agnostic, bottom‑up philosophy focused on quality franchises. Under Nemmoe, the portfolio was reshaped to align with his broader FSSA emerging markets process, with adjustments to country exposures and the addition of high‑conviction names. This included a change in positioning toward South Korea. Having been a significant underweight historically, Nemmoe shifted it to a slight overweight late 2025, primarily by increasing the allocation to Samsung Electronics and initiating a new position in SK Hynix.

Performance

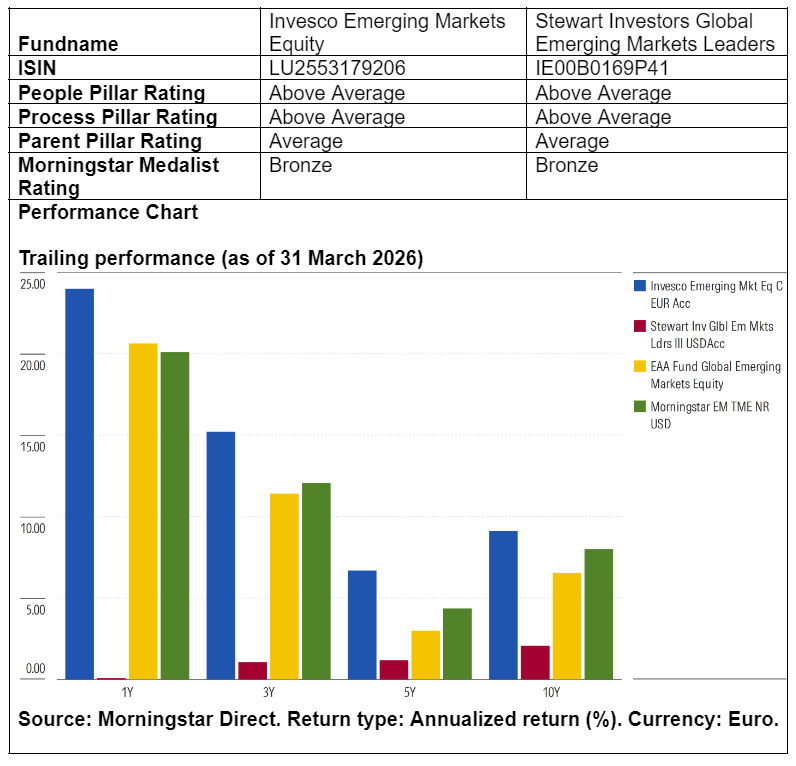

Invesco Emerging Markets Equity has delivered strong, consistent outperformance since 2020, benefiting from valuation discipline, balance-sheet strength, and effective country and stock selection, notably in Korea and Brazil. This approach has underpinned superior downside protection and steady excess returns versus the Morningstar Emerging Markets TME Index and peers. By contrast, the First Sentier Stewart Investors Global Emerging Markets Leaders strategy is at an inflection point following the November 2025 transition to FSSA leadership, rendering its prior track record less relevant. While the philosophy remains quality-focused and defensively oriented, recent performance under Stewart Investors has been weak, hurt by poor stock selection across sectors and countries.

Ronald van Genderen is a senior manager research analyst at Morningstar. Morningstar analyzes and rates investment funds based on quantitative and qualitative research. The firm is a member of Investment Officer’s expert panel.