Geopolitical conflict and renewed inflationary concerns sapped the wind from high-yield sails.

Fixed income markets made an abrupt U-turn in the first quarter. After a positive start to the year, markets dramatically pulled back in March resulting in negative returns for high yield bonds and outflows from the category. Escalations in geopolitical tensions in the Middle East led to a spike in energy prices and supply chain disruptions that caused renewed inflationary concerns—with the ECB initially estimating March inflation at 2.5 percent (above its 2 percent long-term target). That prompted changes in interest rate expectations, with investors shifting their policy expectations from near-term rate cuts, to a pause, or even slight rate hikes later in the year. Spreads widened, and the representative ICE BofA Euro High Yield Index lost 1.7 percent over the quarter, compared to a 0.5 percent gain the previous quarter.

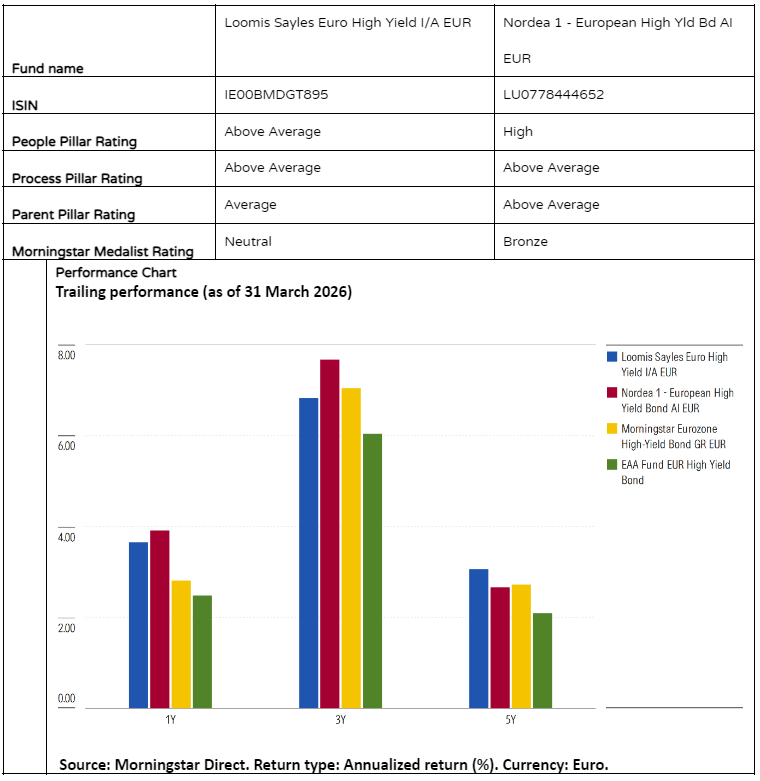

Within the Morningstar European High Yield Bond category, we compare two analyst-rated strategies: Loomis Sayles Euro High Yield and Nordea European High Yield Bond.

People

Both funds are led by experienced teams, though their structures differ.

Loomis Sayles Euro High Yield is managed by a seven-member team that joined the firm from Van Lanschot Kempen in November 2020. Rik den Hartog, Pim van Mourik Broekman and Luuk Cummins form the investment committee that approves all portfolio trades. Each has more than 10 years experience and they have worked together for eight years. The remaining four managers also have responsibilities spanning quantitative tools, trading oversight, and sustainability. All seven portfolio managers conduct issuer research, each covering 30 high-yield and 40 investment-grade names. The team has been stable since 2020, and the tight structure helps mitigate workload and key-person risk. It receives an Above Average People Pillar.

Nordea European High Yield Bond is overseen by four portfolio managers. Sandro Näf and Torben Skødeberg have managed the fund since its 2002 inception, first at Nordea and, from 2007, as founders of Capital Four, which subadvises the strategy. Mikkel Sckerl (2013) and René Kallestrup (2012) complete the team. The managers are supported by a large research platform, comprising 17 global credit analysts and dedicated optimisation and distressed teams. Senior departures included portfolio manager Laust Johnsen in September 2022, but decision-making is consensus-based, and his responsibilities were comfortably absorbed by this team. Altogether the team earns a High People Pillar.

Process

Both strategies are rooted in bottom-up credit research and earn Above-Average Process Pillars, but they manage risk differently.

Loomis Sayles, a fixed-income boutique under the Natixis umbrella, applies a simple and repeatable process across its credit strategies. Bottom-up security selection dominates, complemented by modest top-down adjustments. Sector weightings are typically kept within a few percentage points of the benchmark, while overall credit risk is maintained within 5 percent of benchmark risk. A defining feature is its quality bias: CCC-rated securities are excluded entirely, and a further 4.5 percent of the universe is excluded for sustainability reasons. The managers can invest up to 30 percent in investment-grade bonds to broaden their opportunity set, and use credit default swaps to fine-tune exposure.

Nordea’s process integrates fundamental, legal, and quantitative analysis through proprietary systems. It begins with a broad screening and detailed credit write-up on approximately 250 issuers. Analysts apply conservative growth assumptions and place strong emphasis on new issuance and company access. Liquidity-risk tools, previously an area of concern, have improved materially and shown resilient during the March 2020 market sell-off. The strategy’s size reduces flexibility (5.1 billion euro at the end of 2025), though liquidity metrics remain in line with peers overall.

Portfolio

Differences in portfolio construction reveal the stylistic contrasts between the funds.

Loomis Sayles Euro High Yield is benchmarked against a custom index, combining 85 percent ICE BofA BB Euro High Yield Non-Financial Constrained and 15 percent ICE BofA Euro Subordinated Financials, and the portfolio typically spans 140 to 170 holdings.

Since its February 2021 inception, exposure to BB-rated bonds has ranged from 60 percent to 80 percent. BBB exposure peaked at 27 percent in July 2023 and remained around 20 percent through December 2025, mainly via subordinated bank debt (though Additional Tier 1 and Restricted Tier 1 securities are excluded). Bank exposure averaged 9 percent over the past five years, with conservative positioning evident in an underweight to Italian banks in 2024 and a 3 percent soft cap on French banks extending into 2025.

The Nordea European High Yield Bond has a broader remit. The portfolio historically held around 250 holdings from 150 issuers, but the number of holdings has ticked up in recent years to above 300 issues as of end 2025. While the average rating is BB, the managers have mainly been underweight BB and overweight B and BBB for the four years through 2025. CCC exposure, elevated in 2020 following several downgrades, has declined but remains slightly above their benchmark. At times the team has also used a significant tactical exposure of 5 percent to 6 percent in the iTraxx crossover CDX. Their sector positioning has generally favoured services, with underweights in automotive, utilities and basic industry.

Performance

While the Loomis Sayles Euro High Yield fund is still relatively young, it ranked in the top quartile of its Morningstar Category on both absolute and risk-adjusted measures from February 2021 through January 2026. Returns are generated through disciplined bond selection and numerous small trades. The exclusion of CCCs constrained upside in strong rallies but supported downside protection, including during the US tariff-related March–April 2025 sell-off, when defensive positioning and a telecoms overweight added value.

Nordea European High Yield Bond demonstrates strength over a longer track record. From February 2002 to September 2025, it delivered an annualised return of 6.8 percent, outperforming the average peer by 2 percentage points, while trailing its ICE BofA benchmark by 0.2 percentage points per year. Issuer selection has been the primary driver of historic and recent excess returns in 2025, while derivatives have had mixed effects. Despite occasional short-term shocks (including a 162-basis-point loss in March 2023 linked to its stake in Credit Suisse AT1s that was wiped out), long-term default losses remain below market averages.

Jeana Marie Doubell is investment analyst fixed income EMEA at Morningstar. Morningstar is a member of Investment Officer’s Expert Panel.