This week, the following chart from the Financial Times caught my attention. It shows the net issuance of shares worldwide since 1999. Although the year is still relatively young, 2024 so far shows the largest negative issuance over this period.

As the chart also indicates, in recent years, it has become more common for more shares to “disappear” (often bought back in buyback programs) than are issued. To be precise, in four of the last nine years.

More Debt

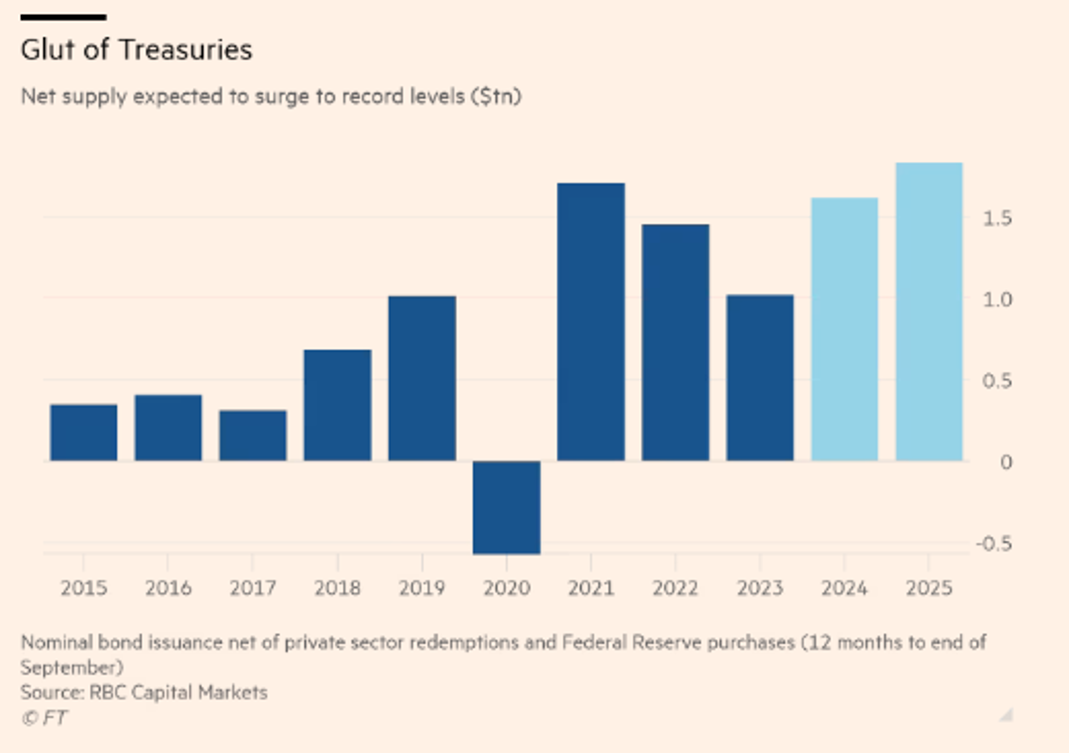

In an environment where debt ratios and budget deficits make the headlines almost daily, this raises the question how this looks like for that other major investment category: bonds. Fortunately, the Financial Times has also made a chart of this.

Here we see the net issuance of U.S. Treasury bonds since 2015. It will come as no surprise that this chart looks the same for many countries. Since Covid-19, the net issuance of government securities is on a “slightly” different level than before.

Equity vs. Debt

In summary, the supply of the largest traditional investment category is steadily decreasing, while that of the second largest is rapidly increasing. In other words, equity is becoming scarcer relative to debt. Assuming that one of the basic principles of economics still holds, that scarce goods (in relative terms) are more expensive than abundant goods, does this not also apply to capital?

Shift?

Many “investors” immediately jump to their extreme role as proponents or opponents of gold and Bitcoin at the mention of scarcity, and for those who follow me, it will come as no surprise that I deal with this daily. But that’s not at all necessary.

If stocks are now structurally more expensive relative to bonds vs in the past, than that can be justified to a certain extent. If the MOVE index (implied volatility Treasuries) is structurally higher than the VIX index (implied volatility S&P 500 Index) compared to the past, than that is not so strange given the supply and demand ratios.

It is interesting to see if and when (institutional) investors will reflect these developments in their strategic portfolios. They will probably wait for the coming rally in bonds (in nominal terms, that is), but what if interest rates return to 2% or lower? Even without expectations about debt sustainability, the size of central bank balances, future inflation, and so on, a simple analysis of the supply of the two largest investment categories raises the question of whether a structural adjustment is not already necessary.

Jeroen Blokland, with his deep expertise in multi-asset investment strategies and keen insights into economic trends, challenges us to ponder the true nature of growth and its implications. His weekly analyses, drawing from his extensive experience at Robeco and through his innovative platforms, urge us to consider whether our collective growth ambition aligns with the realities of our time and the planet.