The financial media are buzzing with stories about the impact of Donald Trump as president, questions surrounding the supposedly high valuation of equities, the collapse of Germany, and the meteoric rise in the price of bitcoin. However, these headlines overshadow the troubling developments in the world’s second-largest economy. It’s time to address that imbalance.

In China, the 10-year bond yield has dropped well below the 2 percent threshold. The pace of this decline in recent weeks reveals that the country is facing significant challenges.

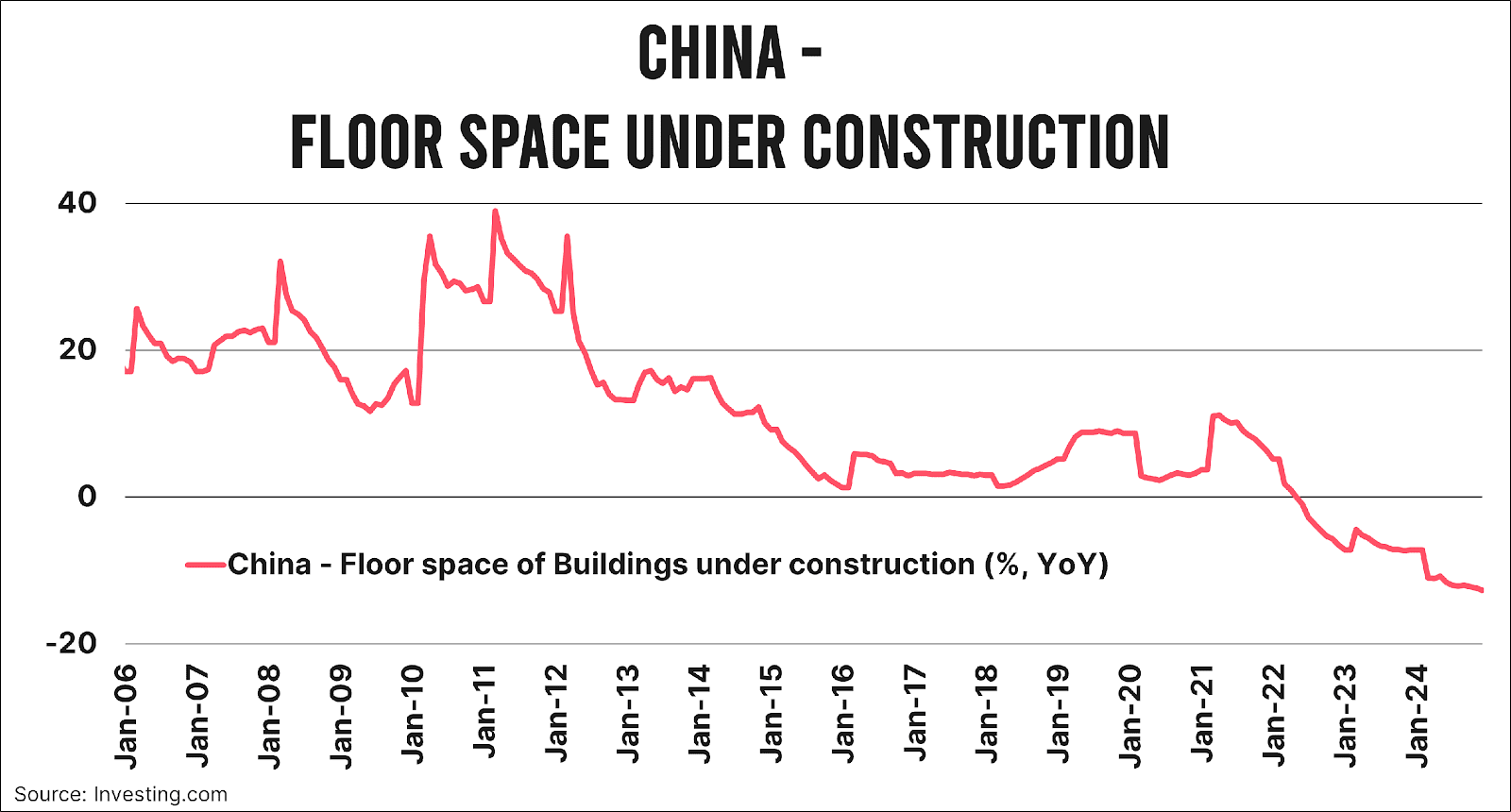

For years, China has dreamed of a more balanced economy, with consumer spending forming the backbone of economic growth. However, years of falling prices and turmoil in the housing market—where many Chinese found themselves paying mortgages on homes that weren’t even completed—have made households cautious. This hesitation is evident in the lack of confidence and subdued spending.

A lack of confidence

Despite a massive series of stimulus measures, consumer spending growth continues to slow. While a 5 percent increase in retail sales was expected for November, the actual growth was only 3 percent. This is a concerning shortfall, especially as China announced barely a month ago that GDP growth for the year would still need to reach 5 percent.

To artificially achieve such growth, policymakers relied until a few years ago on a “trick” involving Local Government Financing Vehicles (LGFVs). These financing arms of local governments were widely used to prop up growth through various channels.

A broken model

The primary revenue source for LGFVs until recently was the sale of land for property development. However, following the collapse of the real estate market, these revenues have all but disappeared.

Some LGFVs have become so distressed that the central government has been forced to absorb some of their debt through debt swaps. Moreover, it is becoming increasingly clear that significant hidden debt remains, which will likely only surface when Beijing is forced to bring it onto its balance sheet.

Predictably, debt—the key growth driver for any ageing economy—has become a hot topic here as well. This also explains why interest rates are so extraordinarily low. China’s debt burden is rising rapidly. The country has abandoned its previous budgetary discipline of keeping deficits below 3 percent of GDP and appears to be in a recession.

Since the Great Financial Crisis, there have been countless examples of what happens in such situations: central banks slash interest rates significantly (check), governments ramp up stimulus efforts (check), and the debt mountain grows structurally (check). If this blueprint continues, we may need to brace for a wave of Chinese inflation in the coming years.

Geopolitical context

Finally, it’s important to view China’s struggles in a geopolitical context. With Trump determined to impose trade wars on anyone who doesn’t conform to the “Make America Great” principle—just as China is increasingly reliant on exports—this is a recipe for tension. China simply cannot afford to see its one remaining growth engine, trade, falter. This is a key reason to believe that China may respond more assertively this time if Trump acts on his threats.

Jeroen Blokland analyses standout, timely charts on financial markets and macroeconomics in his newsletter, The Market Routine. He is also the manager of the Blokland Smart Multi-Asset Fund, a fund that invests in equities, gold, and bitcoin.