I was brought up in an investment era where bond investors proudly positioned themselves as «smart money» investors, in contrast to the «dumb money» crowd that invested in equity markets. But it’s becoming increasingly clear that these bond aficionados may need to relinquish their self-awarded title.

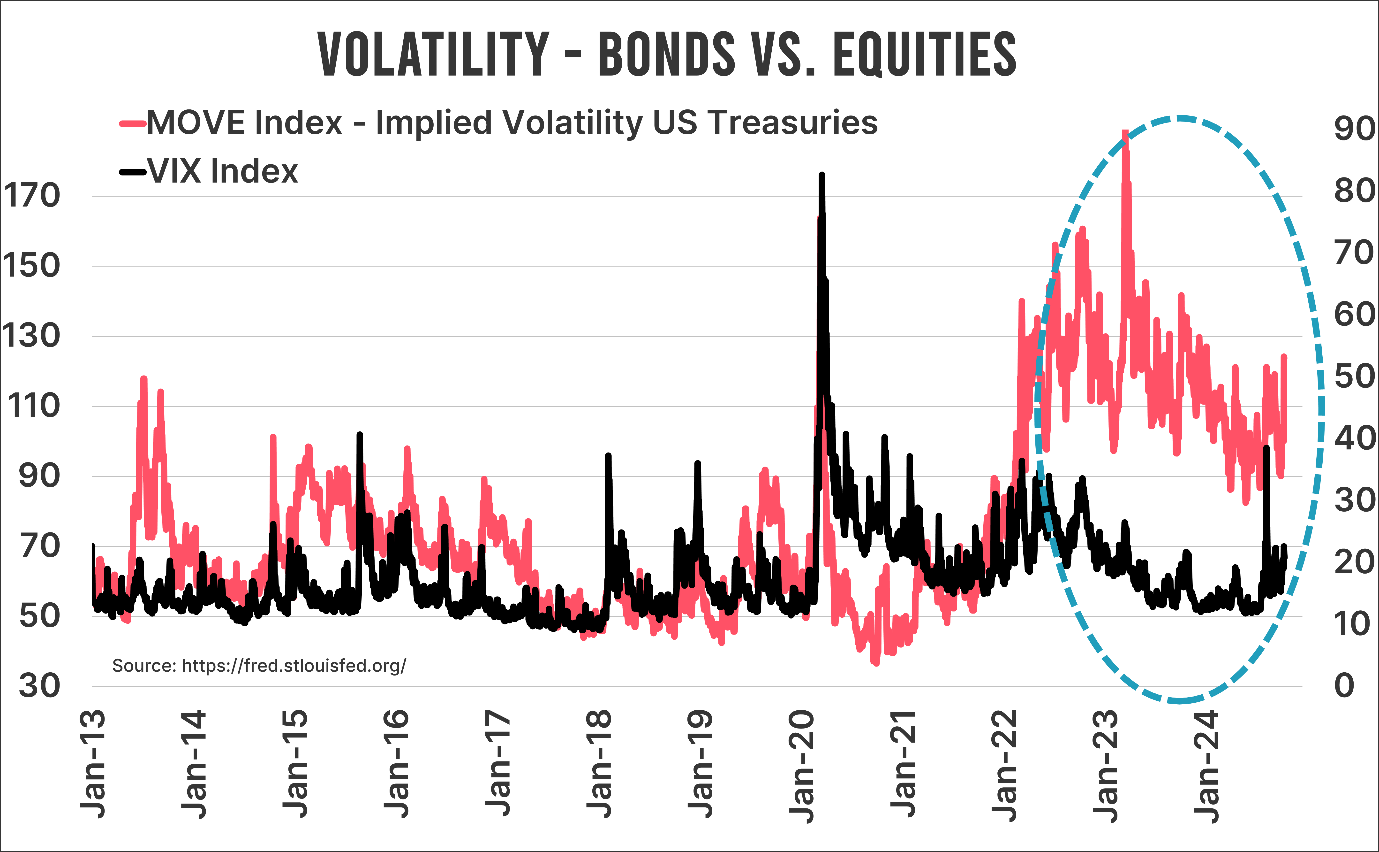

A compelling chart that suggests you shouldn’t automatically trust bond investors is shown below. It displays the MOVE Index, which represents the implied volatility of US government bonds, alongside the VIX Index, representing the implied volatility of the S&P500 Index.

For a long time, the rule of thumb was that when the MOVE Index spiked, driven by supposed «smart money» investors, the stock markets, represented by the naive «dumb money,» would soon follow with a downturn.

As you can see from the chart (and an unseen longer historical trend), the two indices used to mostly move in tandem, each on its own axis. However, since «Bondmageddon» in 2022, bond volatility has consistently remained higher than stock volatility. And although both stocks and bonds suffered a disastrous year in 2022, equities have since rebounded.

Since the beginning of 2023, the S&P500 Index (total return) has soared by an impressive 57 percent. And bonds? Over the past 21 months, they have delivered precisely zero returns, while bond volatility has remained stubbornly in the «red.»

How come?

What is the cause of this? Many investors look to equities for the answer, whereas they should be focusing on bonds. There’s a strong case to be made that this asset class is structurally more risky.

In recent weeks, my Bloomberg timeline has been filled with reports on how much debt both Kamala Harris and Trump will add to the already massive US debt pile. How interest expenses are squeezing out spending on social welfare and other «fixed costs,» how France will never meet the once-sacred 3 percent of GDP target for budget deficits, how Germany, without (artificial) growth, is grappling with existential risks, and how China, after years of stagnation, is trying to escape its seemingly endless property recession with lower rates and more liquidity.

Divergence

So, when the MOVE Index spikes, the question should no longer be what this means for stocks, but rather what it implies for bonds. You could take it a step further by questioning what truly constitutes «dumb money» in a world where interest rates must be kept artificially low, and inflation risks are rising. Locking in negative real yields at higher risk is not exactly smart.

That said, I wouldn’t readily assign the «smart money» label to a market dominated by meme stock investors, one-day options speculators, and perma bears.

Jeroen Blokland analyses striking, current charts on financial markets and macroeconomics in his newsletter The Market Routine. He is also the manager of the Blokland Smart Multi-Asset Fund.