Financial journalists and market experts have a new gimmick: the «Trump trade». With another four years of the Trump show ahead, we might derive all sorts of investment ideas from the yet-to-be-implemented policies. But I have my doubts about most of these trades—not only whether they will yield good returns, but also whether they even exist in the first place.

Trump’s presidential motto, as we know, is “Make America Great Again.” This sums up a policy aimed at consolidating American power, strengthening the domestic economy, and prioritising all things American.

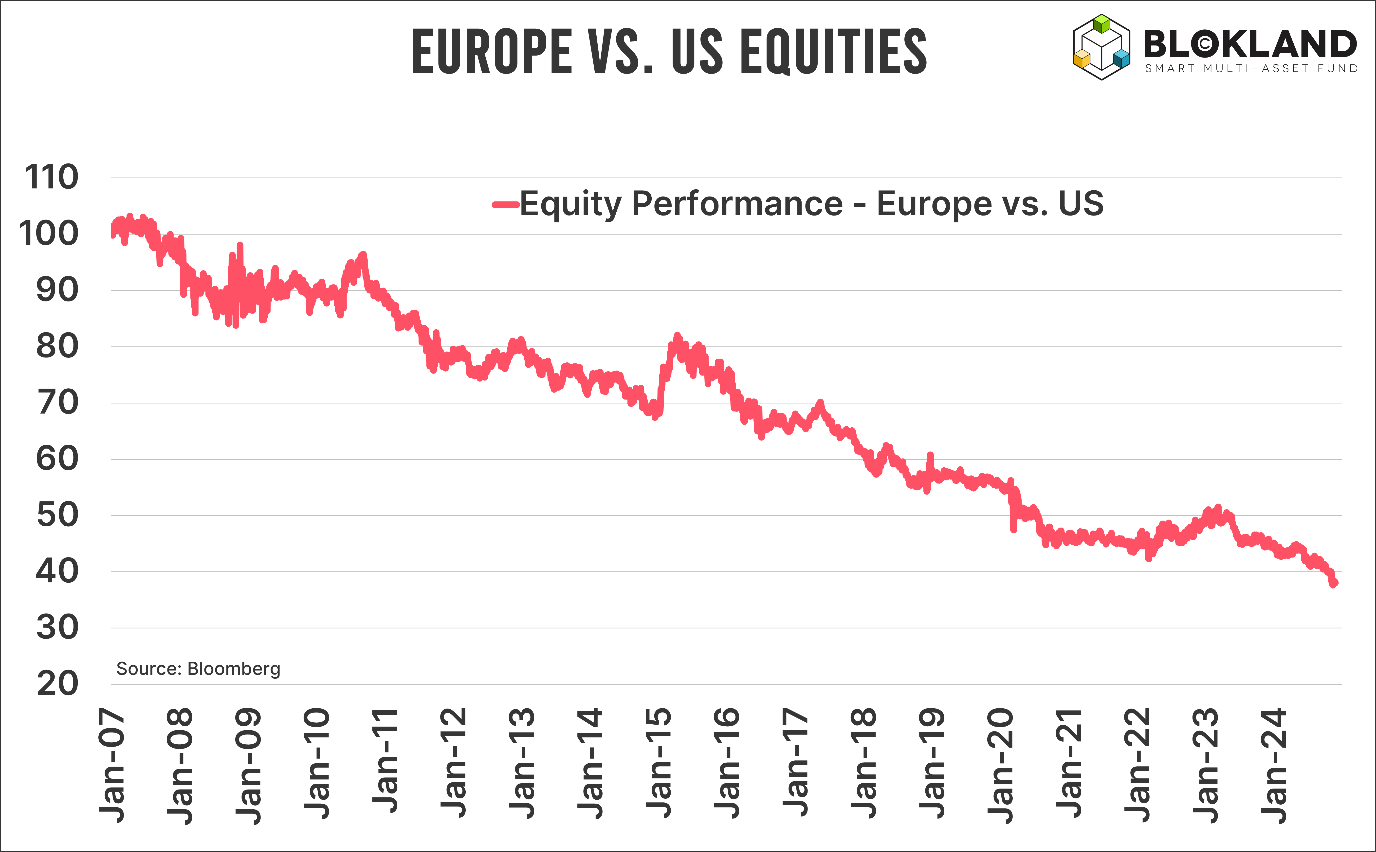

In the weeks following Trump’s victory, U.S. equities performed significantly better than European equities, for example. However, a quick glance at my Bloomberg terminal shows this trend has been in motion for «ages». The reasons are clear and largely tied to Europe: excessive and spiralling regulation, a lack of innovation, hardly any tech giants, an ageing population, overzealous climate policies, flawed energy strategies—you name it. European politicians are too quick to wag an amateurish finger at Trump, who, to be fair, is unlikely to miss an opportunity to rub salt into the wound. That’s just his style.

Small-caps

“Make America Great Again” should, in theory, be particularly beneficial for U.S. small-caps. The Russell 2000 Index outperformed the S&P500 Index immediately after the election, but the two have since moved in tandem. Over the past three and a half years, small-caps have massively lagged behind the technology and AI boom.

The idea that small-caps—still largely absent from this exponential growth trend—will now suddenly outperform is paradoxical. Trump’s goal, including the implementation of large-scale import tariffs, is to persuade companies to produce (and pay taxes) in America. But who do you think will relocate to the U.S.? Precisely: large corporations that will then outcompete smaller American firms.

Energy companies

Trump is not a fan of climate regulations, especially as many seem to have gone overboard. Whether this automatically means you should invest in energy companies, however, is questionable. Trump dislikes (military) wars and generally has a positive view of his ability to end them. A ceasefire in the Middle East, for example, would immediately lead to lower oil prices.

Inflation plays

Those import tariffs are said to cause inflation—at least, that’s what you read everywhere. But this isn’t true. Companies often absorb price pressures, as passing them on to end consumers could lead to a significant drop in sales volumes.

Moreover, trade wars generally create more uncertainty, which benefits no stock. Trump’s recent announcement to take tough action against neighbouring Canada and Mexico is just another example of this.

What does drive inflation is forcing companies to build factories and production centres in the U.S., relocating them from cheaper locations abroad. But that doesn’t immediately benefit American companies—it’s more likely to favour an inflation-sensitive investment category like gold.

The dollar

All this “Make America Great Again” rhetoric is good for the dollar. In fact, I already believe the dollar will outperform other currencies, such as the euro and yen, in the long term—but not necessarily because of Trump’s policies. Quite the opposite, the new Treasury Secretary is known to favour a weaker dollar.

Budget bonus

Finally, I read Elon Musk’s biography. If there’s anyone you can send a budget message to, it’s him. The man managed to launch hobby rockets held together with duct tape into space, ignoring nearly every government regulation along the way.

But people seem to have forgotten what Trump delivered in his first four years: unprecedented budget deficits. The problem with America—and many other countries—is that mandatory spending associated with a welfare state is by far the largest expense. In other words, if you want to structurally reduce deficits, you have to cut there. But making those tough cuts would almost certainly cost Trump his Senate majority in two years. And that would make it much harder to «make America great again».

In conclusion: fade the (Trump) trade—whatever it may be.

Jeroen Blokland analyses striking, topical charts about financial markets and macroeconomics in his newsletter The Market Routine. He is also the manager of the Blokland Smart Multi-Asset Fund, which invests in equities, gold, and bitcoin.