Some macroeconomic indicators carry more weight than others. But does this mean investors always pay attention to the right ones? I doubt it. That’s why, in this column, I focus on a once-reliable recession predictor whose effectiveness is fading, and another indicator that actually determines recessions—but is largely overlooked.

ISM enthusiasts

First, let’s talk about the US ISM Manufacturing Index, which has managed to cross the crucial 50-point threshold only once in the past 26 months. Despite years of above-average economic performance in the United States, the ISM remains widely followed by investors and, under normal circumstances, would already have signaled at least a slowdown in growth.

For years, I’ve wrestled with the ISM’s value as a predictor of economic growth. On the one hand, it boasts an impressive track record, and the logic that manufacturing—though a small fraction of the US economy—is highly sensitive to the business cycle seems sound. On the other hand, the economy today revolves around services.

The ISM Services Index, meanwhile, has stayed above 50 in 23 of the past 26 months—and by a significant margin. This makes it clear that the ISM Manufacturing Index needs to be viewed in a more nuanced way.

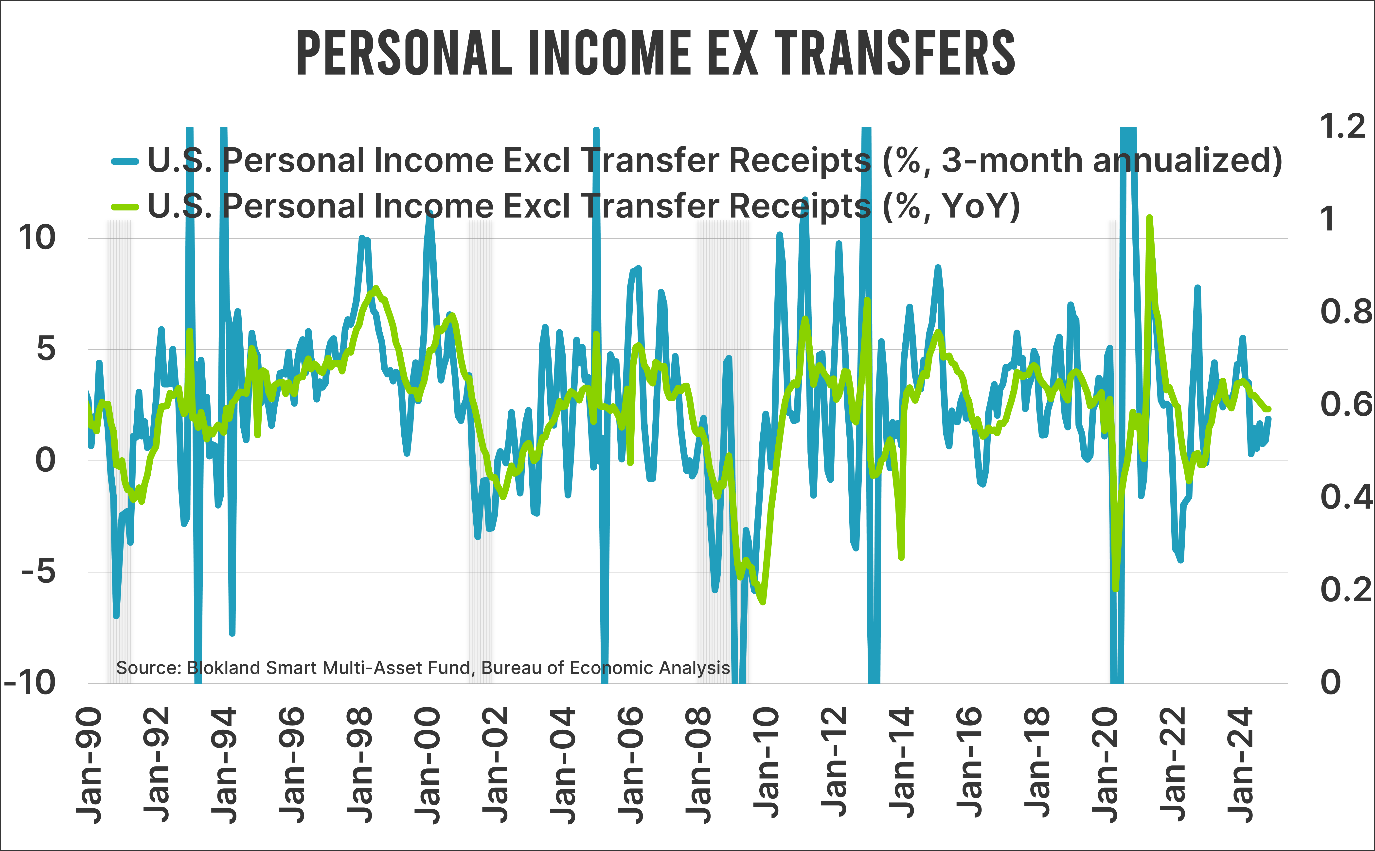

Pure personal income

Now, let’s turn to a metric you rarely hear about but which is nevertheless fascinating: personal income excluding government transfers (such as benefits, subsidies, etc.). In my chart below, you can see this metric represented in two ways: as a year-on-year change and as a 3-month annualized change.

While these series are somewhat lagging indicators, the current data provides little reason to fear a recession. Especially since unemployment claims—typically a reliable labour market predictor—are pointing to job growth. Historically, job growth has been a key indicator of recession risk.

Why is there so little focus on personal income without government contributions? I don’t know. Personally, I always check this data when it’s released, if only because the National Bureau of Economic Research (NBER)—the institution that determines (often retroactively) whether the US is in a recession—uses this figure as one of its two primary inputs for that determination. Perhaps the data just isn’t flashy enough.

The role of the state

However, the distinction between pure personal income and income including government transfers is incredibly relevant today. Why? Simple: government contributions are becoming increasingly significant. In the US, the share of government transfers in total income has grown rapidly over the past 25 years, now accounting for 18 percent.

The government is becoming a bigger player, even in an economy that prides itself as the cradle of capitalism, where many believe the government should remain small.

If you’ve been following my analyses, you might see where I’m going. The fact that the government is contributing more and more to household incomes is not only an example of centralization but also a sign that increasing interventions are needed to sustain economic growth. And this growth is almost always funded by debt.

Income shifts

As a recession indicator, personal income might require us—along with the NBER—to adopt a different standard, such as simply total income including government transfers. After all, when government transfers make up a significant portion of total income, a major shift in this area could likely trigger a recession.

That said, I don’t expect Elon Musk’s newly imagined Department of Government Efficiency to make drastic cuts anytime soon—but I digress.

Jeroen Blokland analyzes striking, current financial and macroeconomic charts in his newsletter The Market Routine. He also manages the Blokland Smart Multi-Asset Fund, which invests in stocks, gold, and bitcoin.