Many investors mistakenly conclude that China and the United States are completely different due to their distinct financial (and societal) systems. However, nothing could be further from the truth. Both nations’ faltering economic engines are kept running by the same remedy: debt.

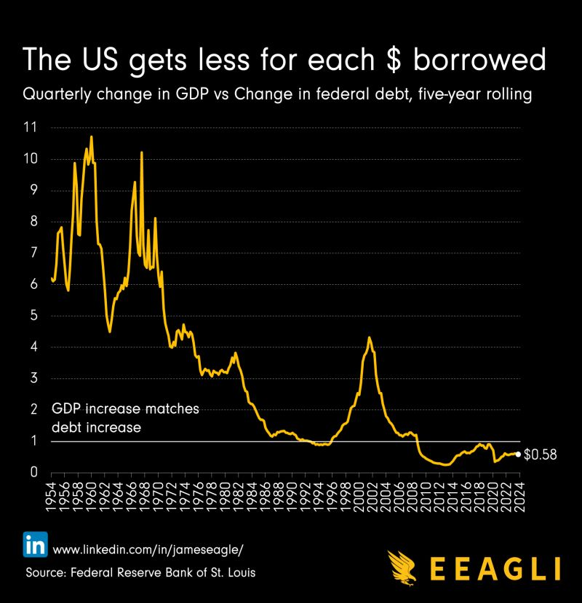

The chart below, from James Eagle (based on Goldman Sachs data, but far more aesthetically pleasing), has gained traction across both traditional media and social media in recent weeks.

It highlights, in a single glance, how the debt intensity of the United States has soared to astronomical levels. Up until the 1970s, every dollar of debt would return between 4 and 8 dollars in nominal GDP growth. Now, that figure has shrunk to a mere 58 cents.

In other words, for every dollar of (government) debt pumped into the U.S. economy, you barely get half a dollar of GDP in return. This makes it easy to answer the question of whether debt will continue to rise in the future. Unless we abandon growth as a goal, more and more debt will be needed to generate it.

Copy-paste

This conclusion, fully justified by hard, factual data, is certainly something to reflect on when considering your investment portfolio.

But it gets worse. No doubt, proponents of debt will point to the unique status of the U.S. and its debt securities as the ultimate form of collateral. Fair enough. So, let’s turn our attention to the other side of the Pacific.

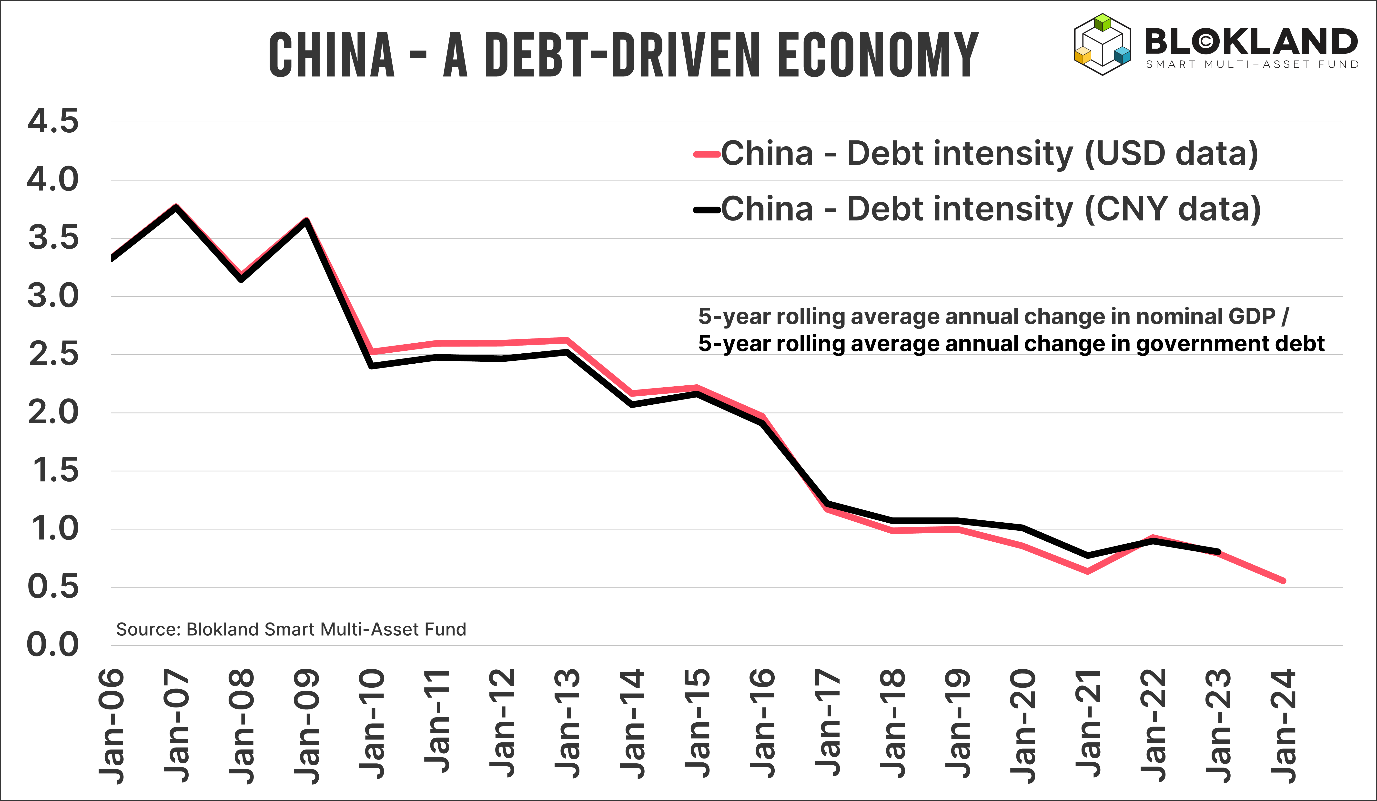

Creating a similar debt-intensity chart is not particularly difficult, so I’ve done that below for China, using the exact same methodology as Goldman Sachs. And since Chinese data often involves U.S. dollar figures, I’ve included both USD and CNY data.

The result is unsurprising, but still spectacular. Based on USD figures (CNY data for 2023 is not yet available), China’s debt intensity stands at 0.56, almost identical to the U.S.’s 0.58. And while I couldn’t go as far back as the 1950s—Chinese data is rather scarce—the trend mirrors that of the United States perfectly.

Do something with it

China, where the working population is set to shrink at an unprecedented pace in the coming decades, is just as much a debt-driven economy as almost every other major economy on the planet.

This has significant implications for bond investors. The need to keep interest rates structurally low in China is clear. More debt will inevitably be required to sustain growth. Do you think Xi Jinping will ever abandon the pursuit of growth? The chances of that happening are zero, especially now that China is in the process of economically sidelining Europe—something the vain Europeans are all too happy to assist with.

Lower interest rates, more concerns about debt sustainability, more central bank antics, and higher and less predictable inflation—everything a bond investor could wish for.

Jeroen Blokland analyses striking, up-to-date charts on financial markets and macroeconomics in his newsletter, The Market Routine. He is also the manager of the Blokland Smart Multi-Asset Fund.