Net like a few years ago, asset managers are once again questioning the traditional 60/40 mix between equities and bonds, as the two asset classes are no longer reacting in opposite directions to market shocks, but increasingly moving in tandem. Is the “safe” 60/40 model portfolio gradually becoming a thing of the past?

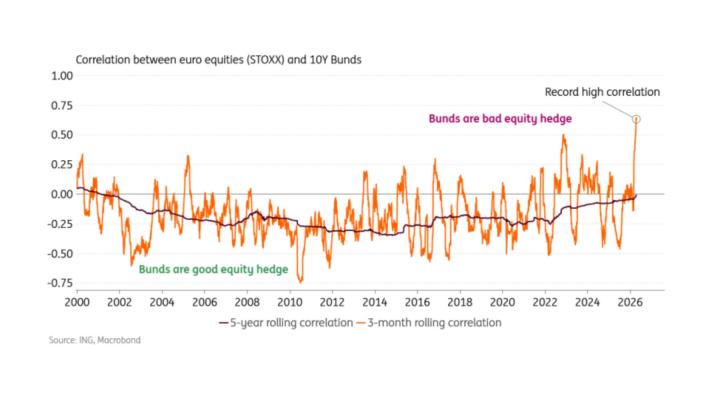

A chart from ING illustrates just how exceptional the past few weeks have been. European equities and German government bonds usually show a negative correlation: when one asset class rises, the other tends to fall, and vice versa. Recently, however, they have started moving in the same direction. With a positive correlation above 0.5, this marks a record not seen so far this century.

Chart: equity and bond correlation (ING)

The exceptional spike is only part of the story. The five-year correlation measure, which reflects the longer-term trend, has become steadily less negative and is now close to zero. That is something markets have not experienced over the past two decades. A structural shift therefore also appears to be underway.

“Bonds are losing their value as a hedge against equities in a portfolio,” ING strategists concluded. “Inflation concerns are likely to persist, even if oil prices decline again, while the short-term impact of AI on inflation also remains subject to debate. As a result, bonds may continue to look unattractive from a portfolio perspective.”

Heading for the trash bin?

All of this is once again putting the classic 60/40 portfolio under heavy pressure, much like three or four years ago. Such a standard portfolio assumes 60 percent equities to benefit from economic growth and 40 percent bonds as a buffer during equity market downturns.

“Look, what was the purpose of 60/40? It provided a defensive component, a type of protection or shield during periods of market stress through government bonds that offered downside protection. And when equity markets were performing well, you would generally still earn some return from those government bonds. Today, that system works far less effectively because of high volatility and inflation—the story is well known,” analyzed Mabrouk Chetouane, chief strategist at asset manager Natixis.

“We cannot bury 60/40 yet, because the model still appeals to many investors”

Mabrouk Chetouane, chief strategist at Natixis

Has the protective power of the mix disappeared for good? According to asset manager Carmignac, the disastrous financial year of 2022—when both equities and bonds suffered heavy losses—effectively marked the end of 60/40. Since then, the allocation model has never truly recovered.

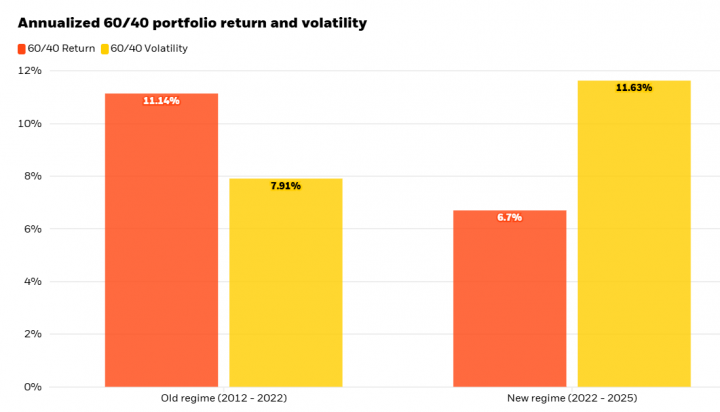

A recent analysis by Blackrock shows that returns from a 60/40 portfolio have been lower in recent years than before, while volatility has increased.

Chart: return and volatility of a 60/40 portfolio (Blackrock)

The New 60/40

Several asset managers are advocating an adjusted version that includes a third asset class, such as private investments, commodities, rare metals, or alternative liquid investments. However, this naturally comes at the expense of the simplicity of the binary formula, which still retains strong commercial appeal among investors.

Others, such as Nomura strategist Charlie McElligott, are searching for “The New 60/40.” These allocation models still feature both a risk-on and risk-off component, but without government bonds. McElligott proposed a combination of technology stocks (risk-on) and energy stocks (risk-off).

Natixis, for now, continues to offer the traditional 60/40 model, albeit with what it describes as a “smart” implementation. “That 60/40 framework remains familiar to many investors. We are therefore implementing a ‘smart’ 60/40 approach, allowing us to increase our equity exposure above 60 percent. At the moment, we are even above 80 percent. We cannot bury 60/40 yet, because the model still appeals to many investors. What we are doing is making it more dynamic, rather than sticking to a static allocation,” Chetouane explained.

But does that still mean the long-term average allocation will eventually return to the 60/40 ratio? “We only started this approach in mid-2025, so we do not yet have enough historical data to determine what the average exposure will ultimately be,” the Natixis strategist replied.

In short, the debate surrounding a possible reinvention of 60/40 is far from settled. The coming months are likely to provide greater clarity on how fundamentally the correlation between equities and government bonds has changed. That, in turn, could pave the way for new defensive multi-asset strategies.