Geopolitical unrest is forcing investors to reassess their portfolios. As bonds lose their strength, volatile asset classes are returning as an alternative for diversification, said Jitzes Noorman, delegated CIO and investment strategist at Columbia Threadneedle Investments.

Investors are turning to commodities and emerging markets to absorb fluctuations in their portfolios. That is striking, as these categories were long considered riskier in traditional portfolio construction due to their structurally higher volatility.

According to Noorman, the renewed interest in these categories is because “bonds are currently not fulfilling their role as a shock absorber for equities”. “Due to higher inflation, a positive correlation has actually emerged,” he said.

In their search for diversification, investors are now accepting more volatility at the individual level, he notes, as long as investments behave differently from the rest of the portfolio. The focus is no longer on the standard deviation of a single investment, but on correlation within the overall portfolio dynamics.

Doomsday Clock

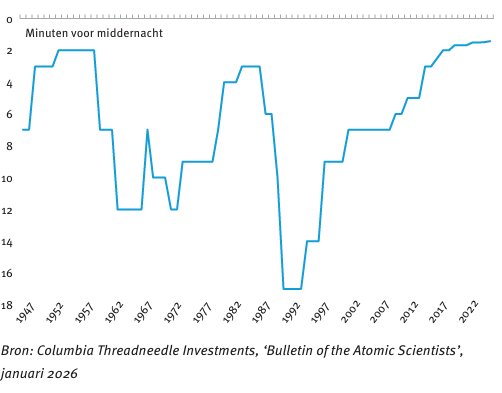

Geopolitical risks have now reached historically high levels, which is reflected, among other things, in the so-called Doomsday Clock. This symbolic clock, introduced in 1947 by, among others, Albert Einstein and since maintained by the Bulletin of the Atomic Scientists, indicates how close humanity is, according to experts, to a global catastrophe: the closer to midnight, the greater the risk. While shortly after the Cold War in 1991 the clock stood at 17 minutes to midnight, in 2026 it stands at 85 seconds to midnight. That is the highest warning level ever, driven by nuclear, climate, and technological risks.

Doomsday Clock

Source: Columbia Threadneedle Investments, “Bulletin of the Atomic Scientists,” January 2026

War and rearmament are almost always accompanied by higher government spending, which is rarely fully financed through taxes. In practice, this leads to more debt issuance and in some cases to monetary financing.

Noorman therefore expects that current tensions will further increase upward pressure on sovereign debt. “Where government bonds from developed countries once served as an anchor in the portfolio, that counterbalance has partly disappeared due to inflation. Moreover, they are no longer seen as risk-free,” he said. “In a world where debt levels are already historically high and continue to rise, inflation risk increases, and with it the likelihood that bonds will further lose their stabilizing role in portfolios.”

Developed markets more volatile

Emerging markets may be able to take over that role from bonds. While they were long seen as the most volatile part of the portfolio, they are increasingly shifting toward a role as a diversification instrument.

According to Noorman, the volatility of equities in emerging markets has in recent years no longer been structurally higher than that of developed markets. This is partly because volatility in developed markets themselves has increased, influenced by Trump, unpredictable central bank policies, and shocks related to technology and AI, in which Western markets are relatively heavily invested. At the same time, the correlation between emerging and developed markets has decreased, increasing their value as a diversifier.

“Emerging markets have always been part of the portfolio, but often to a limited extent. The discussion is now shifting to whether that allocation should be increased further,” said Noorman.

Commodities

Alternative investments are also receiving more attention. Dutch pension funds are rebuilding their commodity allocations after years of reductions. “Commodities are finding their way back into portfolios, including among institutional investors,” Noorman noted. “The fact that pension funds are rebuilding these allocations points to a structural trend.”

Recent history underscores this shift. During the stagflation following the Russian invasion of Ukraine, commodities—a broad basket including oil, gas, industrial metals, and agricultural products—rose by 12 percent, while equities in developed markets lost 23 percent and euro-denominated government bonds declined by 17 percent. In an environment of rising inflation and increasing interest rates, commodities thus provided protection.

That does not mean commodities can always fulfill that function during a crisis. During the Lehman crisis in 2008 and the coronavirus shock, commodities fell sharply, while government bonds still functioned as a safe haven at that time. Which asset class provides protection depends on the type of shock, said Noorman. “Investors therefore face the choice of which crisis they fear more: an economic or an inflation crisis. Commodities work in inflation, but not in a growth shock or liquidity crisis.”

Performance in percent during crises in recent years