As geopolitical tensions rise and instability in the Middle East persists, small-cap equities have shown notable resilience. So-called “domestic champions”—companies with dominant positions in their domestic markets—are benefiting from deglobalisation and shorter supply chains, and appear less volatile than their reputation suggests.

Scott Woods, portfolio manager at Columbia Threadneedle, argued that small-caps are well positioned in a deglobalising world. “The reshoring trend—bringing production or business activities back onshore—works in favour of small-caps, which tend to be more domestically focused than large-caps,” he said.

He refered to companies with strong positions in their home markets as “domestic champions”. “Their shorter supply chains offer relative insulation from geopolitical risks such as tariffs, export restrictions and disruptions to global trade. In addition, they often operate in niches overlooked by large-caps.”

This dynamic is particularly evident in the United States, where energy independence has reduced the economy’s vulnerability to external shocks. Europe, by contrast, remains more exposed to rising energy costs and shortages of raw materials. According to Woods, investors are increasingly looking further down the market capitalisation spectrum to gain exposure to structural trends such as artificial intelligence, energy bottlenecks, the energy transition and demographic change.

Cyclical recovery

Small-caps are thus returning to the spotlight after investors’ attention since the pandemic has been dominated by the so-called Magnificent Seven. “For roughly 35 years, investors could rely on a small-cap premium driven by stronger earnings growth,” said Dimitri Willems, portfolio manager at Triodos. “That relationship broke down around four to five years ago. Capital flowed heavily into large-caps, particularly the Magnificent Seven, pushing small-caps into the background.”

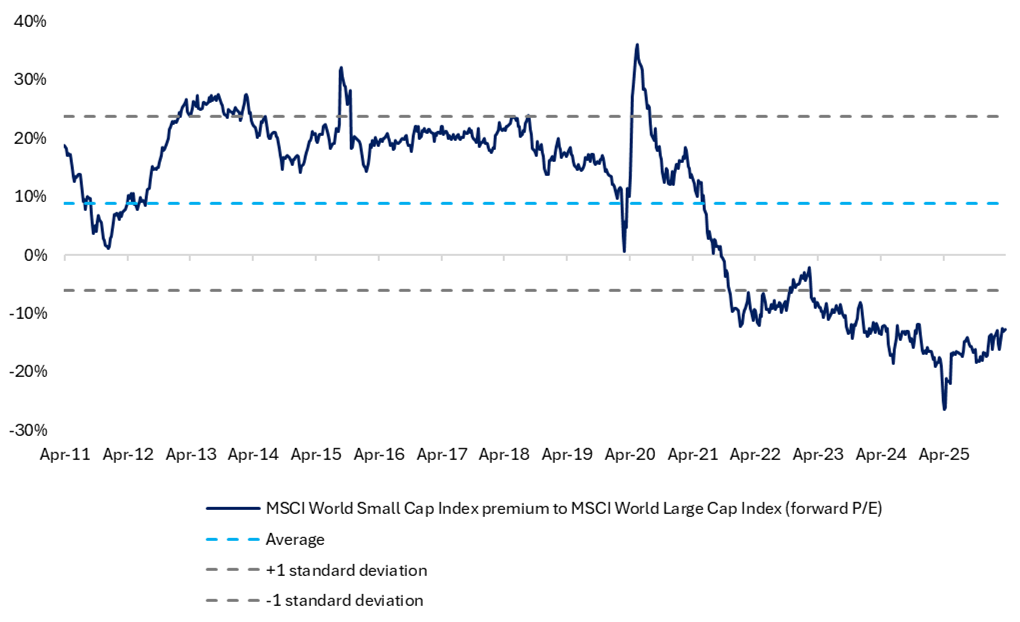

Valuations now reflect that shift. “Small-caps are currently trading at a significant discount to large-caps, well below the 15-year average,” Woods said. According to Willems, the combination of lower valuations and increased concentration in global indices has restored their appeal. “Dispersion has widened significantly, making small-caps once again an attractive source of diversification.”

Premium on small-caps

The broader economic backdrop also supports the asset class. Renco van Schie, CIO at Dutch asset manager Valuedge, points to a “continued cyclical recovery”. “Underlying economic momentum remains strong, and small-caps are benefiting from that.”

He draws parallels with last year. “You could describe it as a kind of ‘Trump spring bottom’. Last spring, drawdowns reached around 20 percent, whereas this year they were limited to roughly 10 percent. Markets are becoming accustomed to Trump’s unpredictability and are already pricing in some degree of de-escalation. This is accompanied by a reallocation from large caps to small-caps.”

Sector allocation

Rising concerns over concentration risk and the heavy capital expenditure of large technology companies are prompting investors to rebalance portfolios. At the same time, they remain keen to benefit from the data centre build-out, leading them to shift towards small caps in industrials and materials. “The capital spending by large caps is actually a tailwind for our companies,” said Willems. “They provide the infrastructure for data centre construction.”

A key distinction lies in sector composition. While large-cap indices are heavily weighted towards technology, small-caps have greater exposure to industrials and materials. This makes them a natural counterbalance in portfolios already heavily concentrated in the Magnificent Seven and the broader tech sector.

Woods noted that “industrials” in the small-cap universe often functions as a catch-all category. “Companies that are difficult to classify tend to be grouped under industrials.” He cited the UK-listed Clarkson, active in maritime services and shipbroking. “Although it is not a traditional industrial manufacturer, it is closely tied to global trade and commodity flows, and is therefore classified within industrials.”

‘Hotel California’ stocks

The perception of small-caps as volatile is partly driven by limited liquidity, which can make it difficult to build or unwind positions without affecting prices. Woods notes that this remains manageable, but requires selectivity.

He warned in particular against so-called “Hotel California” stocks—positions that are easy to enter but difficult to exit due to thin trading volumes. In periods of market stress, these holdings can be hard to unwind without significant price impact, making analysis of trading volumes and shareholder structure as important as fundamental research.