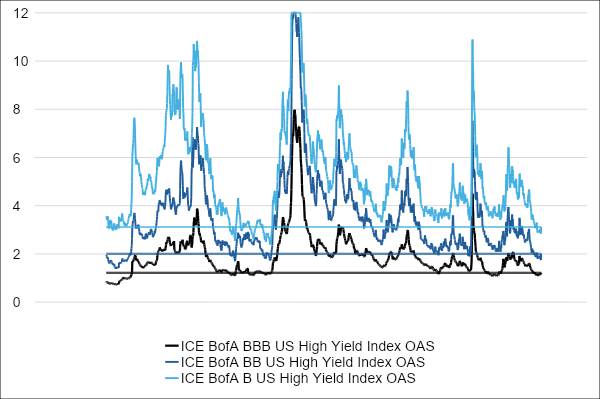

The fortunes of corporate bonds seem heavily reliant on a ‘soft landing’ scenario, given the tight spreads. However, recent history reminds us that spreads can easily double during a recession.

The most challenging environment for corporate bonds is one with bleak economic prospects, coupled with rising interest rates. Fortunately, this was not the case in the first seven months of 2024. The Morningstar US Corporate Bond Index rose by 4.1% in euros, while the Morningstar US High Yield Bond Index, which represents high-yield dollar bonds, performed even better with a 6.8% increase.

In contrast, US Treasury bonds, represented by the Morningstar US Treasury Bond Index, lagged behind with a 1.8% return in euros. Due to the strength of the dollar, the returns of comparable Eurozone bond indices were lower. The Morningstar Eurozone Corporate Bond and Morningstar Eurozone High Yield Bond indices rose by 2% and 4.2%, compared to just 0.3% for the Morningstar Eurozone Treasury Bond Index.

Bond funds were the most popular asset class among European investors over the past seven months. According to Morningstar data, inflows exceeded 200 billion euros, with bonds from developed markets being particularly favoured. Morningstar analysts Mara Dobrescu and Shannon Kirwin have already noted the popularity of fixed-maturity bond funds, but funds investing in euro and US dollar corporate bonds have also caught the attention of investors.

Are corporate bonds expensive?

It’s tempting to argue that corporate bonds are now quite expensive. Spreads on bonds issued by companies relative to government bonds are at historically low levels, depending on credit quality. The question is how much further they can fall.

Not much further, one would expect, since unlike equities—where returns can theoretically be unlimited—fixed-income securities pay a coupon. If the spread, or the compensation for credit risk, becomes too small relative to the interest rate risk, investors might simply switch to safer government bonds.

A commonly cited counterargument is that initial yields are high, and it’s those yields, not the spreads, that ultimately account for the bulk of total bond returns. The question for investors is whether the volatility associated with a sudden change in spreads is acceptable for an investment-grade bond portfolio. After all, the risk of permanent losses due to defaults is low, unlike with high-yield bonds.

USD investment-grade fund

The strategies that prominently appear on Morningstar’s radar are those that, according to the qualitative judgement of our fund analysts, possess a strong management team and a robust investment process, or those identified by an algorithm that assesses funds based on the same framework. In this article, we highlight a fund within the USD corporate bond Morningstar category that meets these criteria and is covered by Morningstar analysts.

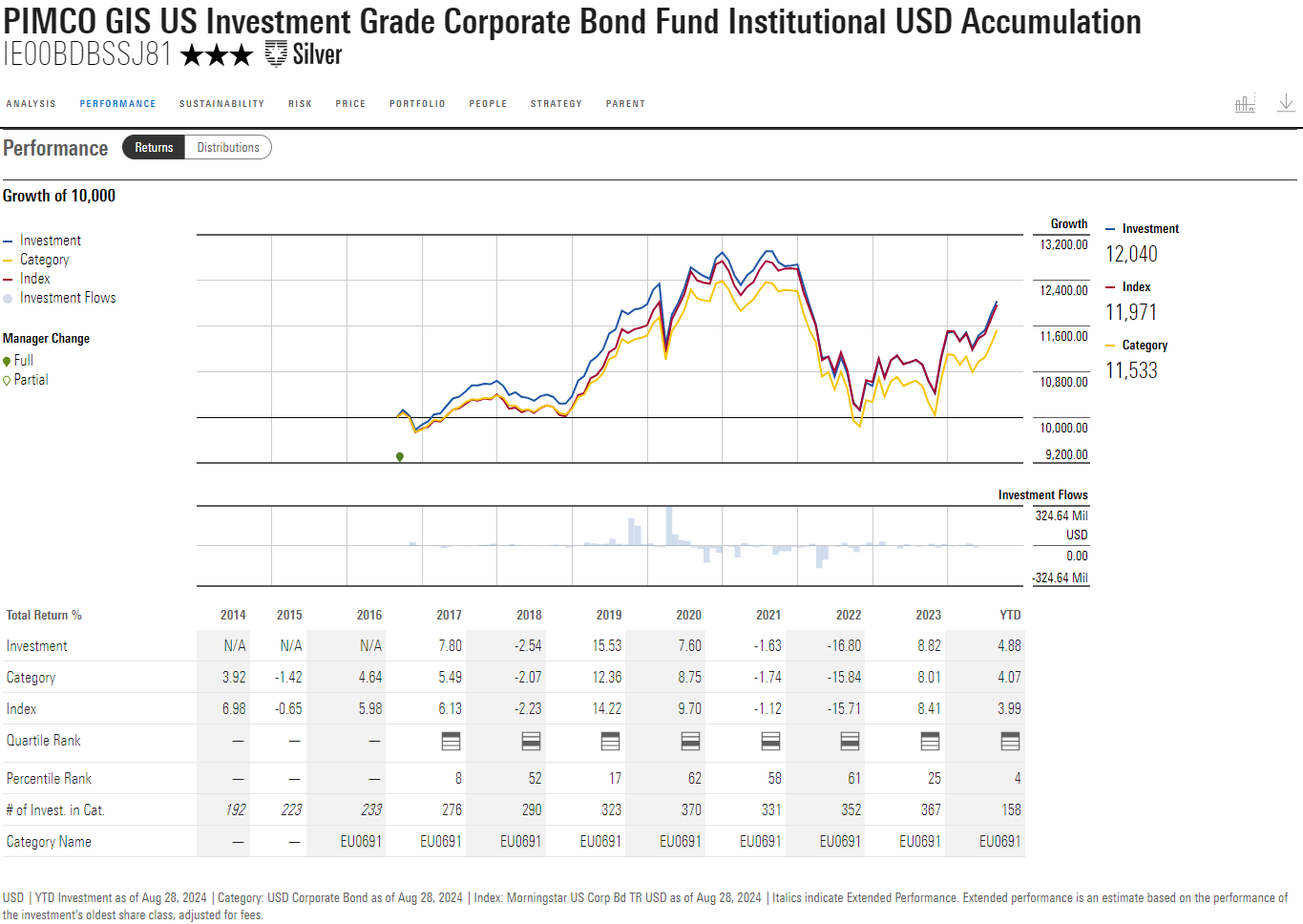

The Pimco GIS US Investment Grade Corporate Bond Fund focuses on investment-grade corporate bonds but can also take smaller positions in high-yield bonds, government bonds, and currencies. It benefits from the expertise of an experienced manager, the support of an impressive team of corporate bond specialists, and a versatile process built on Pimco’s robust macroeconomic and fundamental research.

After years of success, the strategy faced a challenging period from 2020 to 2022, which put relative returns under pressure. However, Morningstar analysts do not see this as a reason to abandon the strategy. A closer look at this period is reassuring. Rather than overly aggressive positioning, the weak performance in 2020 was due to significant exposure to sectors heavily impacted by the COVID-19 pandemic, as well as an underweight in technology and healthcare sectors. The analyst team’s assessment was, as always, the driving force behind this positioning. In 2021, the team’s stock selection results were strong, but interest rate- and currency positions negatively impacted average performance, while exposure to Russian and Chinese bonds was somewhat offset by adept interest rate management and credit selection in 2022.

The strategy appears to have turned a corner and outperformed both the competition and its Morningstar US Corporate Bond category index in 2023 and 2024. Moreover, under Mark Kiesel’s leadership, the fund has generated excellent long-term returns and benefits from an impressive team of managers and analysts, earning it a ‘High’ People rating. A range of analytical tools helps managers quickly spot opportunities and assess the relative value of bonds. Combined with thoughtful macro analysis and price awareness, this ensures the fund receives an Above Average Process rating.

Thomas De Fauw is a manager research analyst at Morningstar. Morningstar analyses and rates investment funds based on quantitative and qualitative research. Morningstar is one of the expert panel partners of Investment Officer.