From depressed to euphoric. The mood of global stock markets could change rapidly during the third quarter of 2024. To navigate through such volatile market conditions, investors need a long-term vision, patience, and perspective.

At the end of the day, the Morningstar Global TME index posted a positive return of 2.32% for the third quarter, bringing the year-to-date performance to an impressive 17.37% by the end of September. So, those who took an extended summer holiday or hadn’t checked their investment account for three months managed to ride out the turbulent market climate worry-free.

Concerning geopolitical developments, recession fears, worries about the U.S. labour market, shocking developments in the U.S. presidential elections, (un)expected interest rate hikes by central banks, and the long-anticipated announcement of China’s stimulus bazooka to revive its sputtering economy are just a few of the events that have significantly impacted market sentiment over the past three months.

The first weeks of the second half of 2024 started with a lot of turmoil. Not only in the context of the U.S. elections, where presidential candidate Donald Trump survived an assassination attempt and Joe Biden, under pressure, withdrew from running for another term in the White House, leaving Kamala Harris to lead the Democrats. A lower-than-expected U.S. inflation figure boosted expectations of upcoming rate cuts by the Fed, which turned out to be a catalyst for small-cap stocks that typically have more financial leverage, making them more sensitive to changes in financing costs. The revival of small caps coincided with a correction among large caps, with semiconductor companies and the Magnificent Seven no longer being the favourites among investors, shifting the focus to the lagging value sectors.

Nikkei

The start of August was possibly even more turbulent. An unexpected rate hike by the Bank of Japan shook the Nikkei index to its core. The stock market index tumbled nearly 20% in just a few days. Additionally, a weak U.S. jobs report, disappointing economic growth, and worrying figures on economic activity and unemployment brought the recession scenario back into investors’ minds. Shortly thereafter, an impressive rally followed, fuelled by hopeful economic data and growing expectations for stimulus measures from central banks.

Jay Powell didn’t disappoint the market and cut the policy rate by half a percent, indicating that the time had come for rate cuts now that inflation seems more under control and economic growth and employment deserve support. However, the biggest boost for investors came from the Far East, where Beijing announced a large and decisive stimulus package that should finally lift the world’s second-largest economy out of its slump. This resulted in an impressive sprint finish for Chinese stocks, which have suddenly reappeared on investors’ radar. For various reasons, they had fallen so far out of favour that fund houses in recent years launched “ex-China” investment funds. With such an explosion in returns, the question now is whether investors can continue to ignore China and if interest in “ex-China” investment funds will diminish.

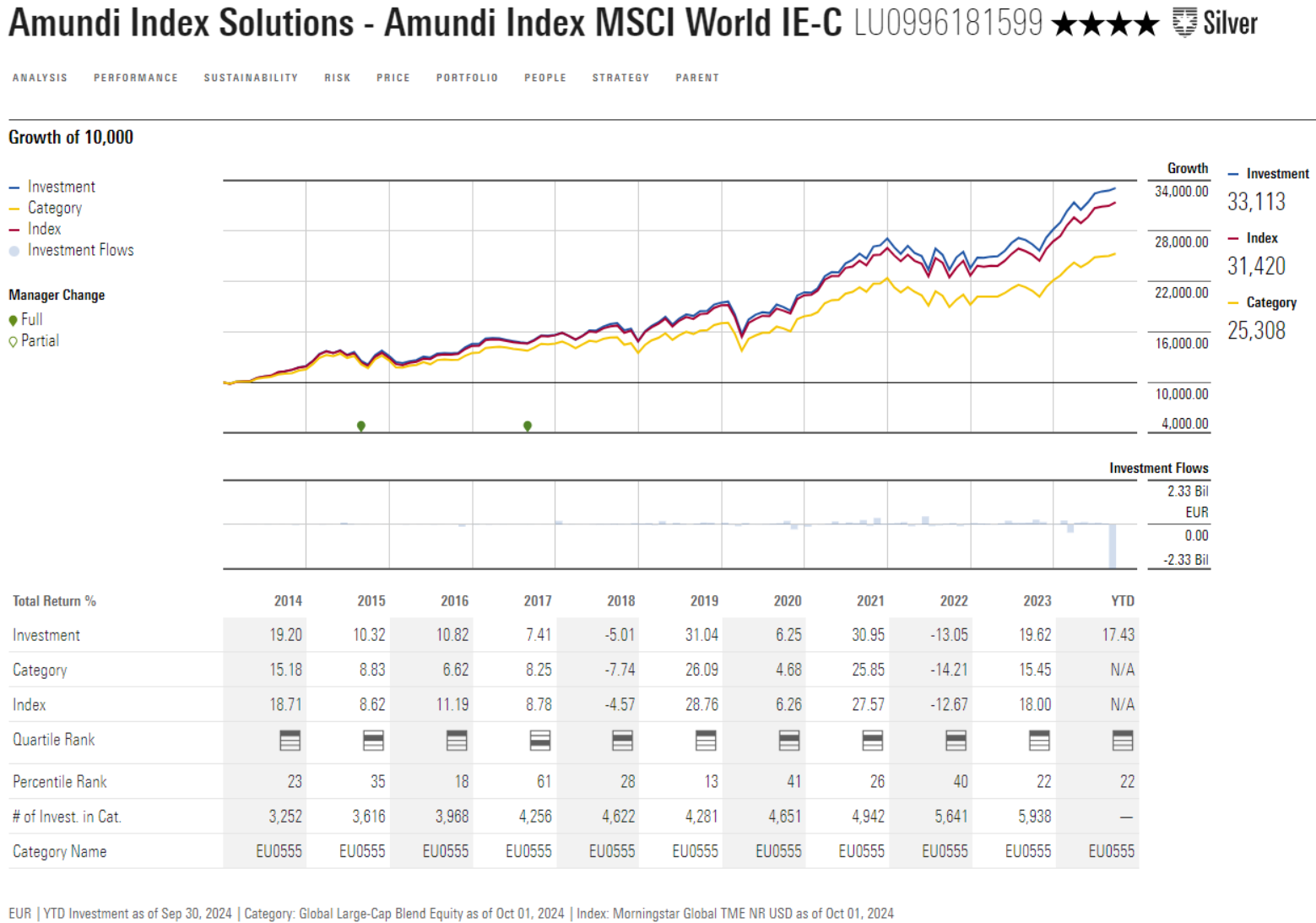

Passive exposure globally

The strategies that prominently appear on Morningstar’s radar are judged to have a solid management team and a sound investment process, either based on the qualitative judgment of fund analysts or via an algorithm that evaluates investment funds based on the same framework used by the analysts. In this edition, we highlight a fund that meets these criteria within the Morningstar category Global Equity Large-Cap Blend.

For those seeking passive exposure to global equity markets, the Amundi Index MSCI World index fund could be a good option. Morningstar analysts have awarded the fund a Silver rating.

Amundi IS MSCI World has consistently proven to be a reliable tool for investors seeking exposure to the global stock market. The index offers a high degree of diversification in large- and mid-cap companies across 23 developed markets and represents about 85% of the free float-adjusted market capitalisation in each country. The market capitalisation-weighted index places an emphasis on large-cap stocks and ensures low turnover. This makes the fund a strong competitor in its category, making it difficult for active funds to outperform.

The portfolio management team of Amundi’s passive funds is among the most experienced and stable in Europe. The team approach to managing passive funds minimises the risk of key personnel loss since managers can replace each other, ensuring continuity and stability in the fund’s performance.

US overweight could become a risk factor

The index tends to have a larger weighting in U.S. companies compared to the average peer in the category and indices such as MSCI ACWI IMI, which offers broader geographical coverage. This overweight has been a key factor in the fund’s recent strong performance. However, while the emphasis on U.S. stocks has been a benefit, it could become a risk factor if market conditions change.

The index also doesn’t cover the smaller end of the market capitalisation spectrum, which can either benefit or hinder performance, depending on market conditions. Investors looking to maximise their exposure might consider passive alternatives tracking the MSCI ACWI IMI.

Regardless, this fund remains an attractive option within the Morningstar Global Equity Large-Cap Blend category. It has a strong track record of outperforming the average peer in the category and consistently delivers favourable cumulative returns across various time horizons.

However, it is worth noting that the Luxembourg domicile places the fund at a disadvantage compared to Ireland-based funds, as it pays higher withholding taxes on dividends from U.S. companies, which make up two-thirds of the fund’s holdings.

Jeffrey Schumacher is Director of Manager Research at Morningstar Benelux. Morningstar analyses and rates investment funds based on quantitative and qualitative research. Morningstar is part of the expert panel at Investment Officer.