The Iran war has broken the trend toward greater convergence between yields on European government bonds. Yields rose particularly sharply in Italy and the United Kingdom, while countries such as the Netherlands and Spain managed to limit the damage somewhat.

Belgium, France, and Germany formed the middle group in the bond market over the past two months. Since the start of the attacks on Iran at the end of February, yields on 10-year government bonds in those countries have risen by more than 16 percent. The Netherlands and Spain remain just below that level, while Italy has seen the largest increase among these six euro area countries at nearly 20 percent. The United Kingdom follows with an increase of more than 18 percent.

Dependence on fossil energy partly explains this, said Rob Dekker, portfolio manager for fixed income at Achmea Investment Management. “Italy and the United Kingdom have higher gas consumption than other European countries, which leads to larger inflation shocks. Italy has also introduced a support program that includes, among other measures, a 25 cent reduction in fuel excise per liter. Measures like these ultimately put more pressure on government debt.”

Investor positioning is also highly influential, Dekker added. “Italy has been an attractive option for bond investors in recent years, and many expanded their positions there. But what do you do in a crisis? You first sell the positions where you are overweight.” As a third factor for Italy, the portfolio manager points to economic growth, which already weakened last year.

Yield increases in Europe since the start of the Iran war

Michiel Tukker, European rates strategist at ING, also points to positioning. “In recent years, the carry trade has focused on Italy. Borrowing cheaply from the ECB for a short period and then investing in Italian government bonds was a strategy that delivered strong returns for a long time. But you want to be sure that your short-term funding will not become more expensive in the future.”

That outlook has now reversed: interest rate expectations have turned 180 degrees since the start of the Iran war. Tukker: “At the beginning of this year, the market expected rate cuts for this year, making the outlook for the carry trade favorable. But now the average expectation is that the ECB will raise rates at least twice this year. For these investors, mainly hedge funds, this is the main driver to reduce their Italian positions.”

Italy was particularly attractive for the carry trade because, among the major European economies, the yield spread with German government bonds was the largest. That spread did narrow due to this strategy, as did differences with other European countries, but the Iran war has now put an end to that trend.

“Peak has passed”

Analysts nevertheless assume this is temporary. “We have already seen the peak,” Tukker said. “The Germany-Italy spread fell to around 60 basis points in February and then quickly rose to 95 basis points in recent weeks. But it has since fallen back to below 80.”

Dekker (Achmea Investment Management) also believes this is a temporary disruption of the convergence trend. “That trend is not only driven by better performance in peripheral countries, but also by the fact that Germany is building up larger government deficits. That pushes up yields on German government bonds.” In addition, a large volume of German bonds is coming to market as the ECB winds down its purchase programs, Tukker notes.

Countries such as France and Belgium only need to stabilize their government debt to become more attractive to investors relative to “anchor” Germany. France appears to be supported by its greater reliance on nuclear energy, Dekker said. “Moreover, the French government is now managing to implement measures that keep budget deficits under control.”

Top of the class

Meanwhile, the Netherlands appears to be playing the role of the top student in the class. The spread with Germany has not increased over the past two months but has even declined slightly, to around 6 basis points. Tukker: “That is the discussion on the trading floor: how long will it take before the Netherlands can borrow more cheaply than Germany? For 30-year bonds, that is already the case, and it is certainly conceivable that this will also happen for 10-year bonds in the foreseeable future.” The reason? “The Netherlands is one of the few euro area countries with government debt below 60 percent of GDP. A defining feature of recent years is that there are always investment plans, but in the end not much happens. The Netherlands consistently spends less than budgeted, as investors see it. That is positive for creditworthiness.”

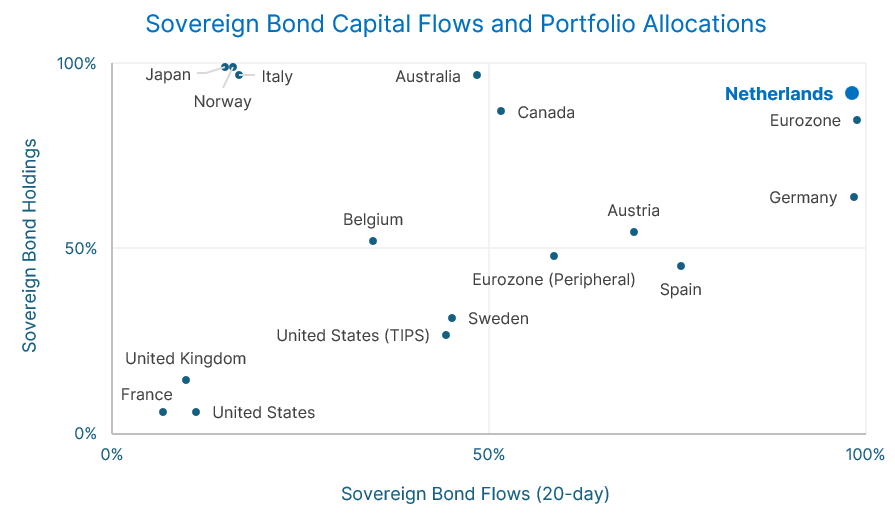

State Street: increasingly selective demand for European government bonds

Differences in investor confidence across European countries are widening again, according to the latest Sovereign & Institutional Investment View from State Street, which tracks the portfolios of institutional investors worldwide.

On the y-axis of the chart below, it can be seen that these investors are significantly overweight (close to the highest level of the past five years, according to State Street) in Dutch and Italian government debt, while the underweight in French and UK government bonds has reached nearly a five-year low.

On the x-axis, flows are shown: the net buying position of institutional investors in Dutch and German debt is very large, while they are selling Italian, French, and UK government bonds en masse. This net selling position has rarely been this large over the past five years. Belgium and Spain occupy middle positions in this respect.