Private equity’s model is coming under strain as exits slow, capital remains tied up, and investors are waiting longer for distributions. Rather than resolving these pressures, the industry is increasingly passing them on to individual investors, said Lucas Crasborn, chief investment officer at Optimix Vermogensbeheer, an independent wealth manager overseeing around 2.5 billion euros.

The core logic of private equity relies on capital circulating: invest, exit, reinvest. That cycle is slowing. Holding periods are extending, exits are delayed, and capital is returning to investors more slowly.

“It takes much longer to get money back. So investors can commit less new capital,” Crasborn told Investment Officer. In response, the industry is turning to new sources of capital, particularly among individual investors.

“The average holding period has doubled from four to eight years. That makes it much harder to achieve strong IRRs,” Crasborn said. As capital stays locked up longer, internal rates of return measuring annual performance over an investment’s life come under pressure.

Billionaire factory

What began as a niche strategy, where investors improved underperforming companies, has evolved into what Oxford economist Ludovic Phalippou calls a “billionaire factory.” In 2021 alone, around 1,000 billion dollars was raised globally. That capital has competed for a limited pool of deals, often through auction processes with dozens of bidders, pushing valuations higher and compressing returns.

The shift has pulled the entire industry toward private assets, including traditional asset managers. “Private assets are the Holy Grail. They have two major advantages: extremely high fees and strong client loyalty. Once a client is invested, they cannot easily leave. From a business perspective, it is a no-brainer,” Crasborn said.

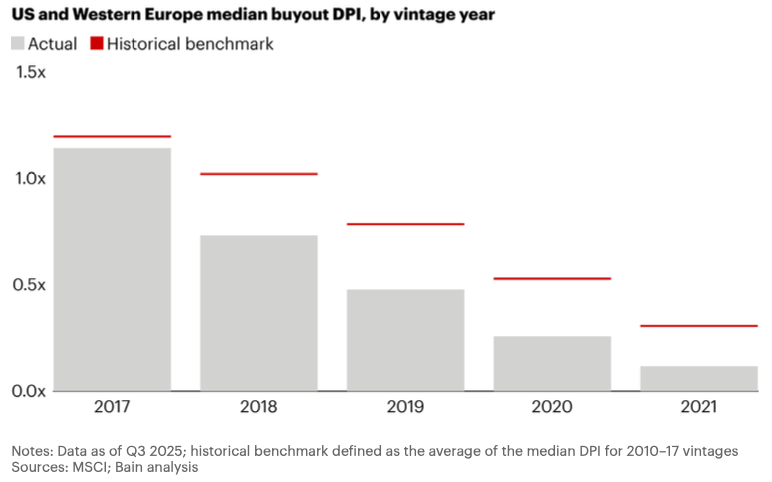

Underperformance in recent vintages

The consequences are now becoming visible. According to Bain & Company’s February 2026 Global Private Equity Report, distributions to investors have remained below 15 percent of net asset value for four consecutive years, marking a historic low. The industry is holding roughly 32,000 unsold companies, with an estimated value of 3,800 billion dollars. Average holding periods at exit have nearly doubled.

Phalippou’s research highlights the implications for returns. Between 2010 and 2019, private equity delivered only marginal outperformance relative to public markets, with a public market equivalent of 1.03. That translates into around 3 percent excess return over ten years, despite illiquidity, high fees, and limited transparency.

Norway avoided $80 billion in fees

Norway’s sovereign wealth fund, which chose not to invest in private equity following Phalippou’s advice around 2010, is estimated to have avoided approximately 80 billion dollars in fees.

Since 2019, performance may have deteriorated further, Crasborn said. “That means investors effectively received no illiquidity premium.”

Phalippou also estimates that private equity funds launched between 2006 and 2015 generated around 230 billion dollars in carried interest. That amount accrued to a relatively small group of individuals during a period when net returns broadly tracked public equity markets. The number of private equity multibillionaires rose from 3 to 22 over that period.

Volatility masking

Institutional demand for private assets remains strong, in part due to what Crasborn describes as “volatility washing.” Private assets are valued infrequently, which smooths reported performance without changing underlying risk.

That dynamic extends to private credit. Reported default rates remain close to zero, while comparable high-yield markets show default rates of around 4 percent. Crasborn argues this reflects accounting rather than credit quality. “If a company cannot pay, a new deal is structured. Terms are adjusted, maturities extended, and upside is shared. In practice, that is a default.”

In public markets, such events would be recognized as defaults. In private credit, they are often absorbed through restructuring until losses become unavoidable.

Extending the model

To manage delayed exits, firms are increasingly using continuation vehicles, which allow them to hold assets beyond the original fund life. These vehicles are typically managed and priced by the same sponsors, raising questions around valuation and governance.

Many of these structures are now being marketed to individual investors. Leverage at the fund level can boost projected returns, while also increasing risk.

At the same time, operating costs across the industry are rising. What was once a relationship-driven business has developed into a large-scale distribution effort.

Bain sees need for material improvement

Management fees are under pressure, while investors who committed capital during peak years such as 2021 and 2022 face constraints as distributions remain weak. Bain notes that general partners will need to improve value creation materially, although evidence of such improvement remains limited.

“You now see a market where liquidity is disappearing, and those products are being sold to private investors,” Crasborn said. Semi-liquid structures such as Eltifs are expanding across Europe, offering periodic redemption windows.

Recent developments in US private credit funds show how quickly those limits can be reached. Redemption requests have exceeded thresholds, forcing funds to cap withdrawals. In some cases, investors received less than half of the amount requested.

“When assets cannot be sold, the industry turns to the retail market,” Crasborn said. “Investors are told they are gaining access to opportunities previously reserved for institutions. In reality, the industry’s problems are being transferred to them.”