With the restoration of the negative correlation between equities and bonds, the structure of strategic asset allocation is once again under debate among asset owners and asset managers. Was the shift away from the traditional 60/40 portfolio towards a permanent allocation to private markets a lasting course correction — or merely a temporary response to an extraordinary period? Investment Officer spoke to four leading investment professionals.

“The 60/40 portfolio is no longer relevant. Full stop,” says Wouter Sturkenboom (pictured), CIO at Providence Capital, a Netherlands-based multi-family office serving high-net-worth families. Private markets have secured a permanent place in the portfolios of the Bussum-based multi-family office. “We are outspoken proponents of private investments, which allow you to add assets with a different return profile to the portfolio, such as infrastructure and factoring. It makes portfolios more robust. That said, we only consider them suitable once a portfolio has reached a certain scale, given the illiquidity they introduce.”

“The 60/40 portfolio is no longer relevant. Full stop,” says Wouter Sturkenboom (pictured), CIO at Providence Capital, a Netherlands-based multi-family office serving high-net-worth families. Private markets have secured a permanent place in the portfolios of the Bussum-based multi-family office. “We are outspoken proponents of private investments, which allow you to add assets with a different return profile to the portfolio, such as infrastructure and factoring. It makes portfolios more robust. That said, we only consider them suitable once a portfolio has reached a certain scale, given the illiquidity they introduce.”

Roelof Salomons, investment strategist at BlackRock Netherlands, describes the 60/40 portfolio as “not a law of nature, but rather a reminder of a calmer era”. In a world where uncertainty has increased, investors need to combine assets that do not correlate with one another. “In 2022, investors were hit in both equities and bonds; bonds failed to perform the buffering role they had long fulfilled. Investors realised that private markets could offer additional diversification and risk dispersion.”

Not everyone shares that conviction. Renco van Schie (pictured), CIO at Dutch asset manager Valuedge, argues that the traditional anchor portfolio is “still performing perfectly well”. According to him, the negative correlation between equities and bonds has already been restored for some time. “Once inflation fell below 3 per cent, the negative correlation returned. That has been the case for a while now. In our view, private markets add complexity and risk rather than genuinely improving the risk profile.”

Not everyone shares that conviction. Renco van Schie (pictured), CIO at Dutch asset manager Valuedge, argues that the traditional anchor portfolio is “still performing perfectly well”. According to him, the negative correlation between equities and bonds has already been restored for some time. “Once inflation fell below 3 per cent, the negative correlation returned. That has been the case for a while now. In our view, private markets add complexity and risk rather than genuinely improving the risk profile.”

ABN AMRO, the Dutch-headquartered bank with operations across the Netherlands, Belgium, Germany and France, also does not fundamentally deviate from the classic model, maintaining a strategic allocation of 55 per cent equities and 25 per cent high-quality bonds. Nevertheless, the bank is exploring the possibility of incorporating private markets into portfolios. “That would be done gradually,” says CIO Richard de Groot. “An initial allocation of around 10 per cent via ELTIFs, for example.”

Disrupted correlation

In 2022, equities and bonds simultaneously posted negative returns for the first time since 1977. The traditional 60/40 portfolio declined by approximately 16 to 18 per cent — its worst performance since 1937.

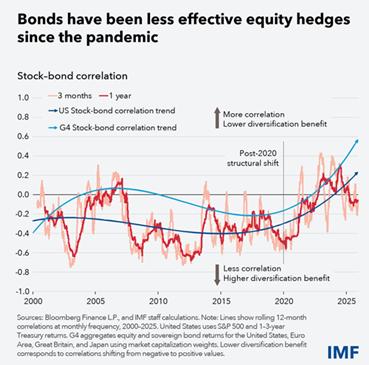

The key question is whether the shift in correlation was temporary or structural. A recent IMF analysis suggests the turning point already occurred towards the end of 2019. With the outbreak of the pandemic the following year, the historical relationship changed markedly, making simultaneous sharp declines in both equities and bonds more frequent. The IMF argues that investors should consider alternatives such as commodities or private assets to compensate for reduced diversification.

Salomons (pictured) believes that, at least in the near term, portfolios benefit from incorporating a private markets allocation. “We are in the build-out phase of an industrial revolution driven by artificial intelligence. That build-out requires substantial energy and labour. Shortages exist on both fronts. Deglobalisation is also pushing up costs. The combination of deglobalisation and supply constraints is more likely to result in inflation surprising on the upside rather than the downside. In that scenario, private markets can serve as an important shock absorber within a portfolio.”

Salomons (pictured) believes that, at least in the near term, portfolios benefit from incorporating a private markets allocation. “We are in the build-out phase of an industrial revolution driven by artificial intelligence. That build-out requires substantial energy and labour. Shortages exist on both fronts. Deglobalisation is also pushing up costs. The combination of deglobalisation and supply constraints is more likely to result in inflation surprising on the upside rather than the downside. In that scenario, private markets can serve as an important shock absorber within a portfolio.”

Alternative to bonds

Sturkenboom seeks part of the bond alternative outside public markets, through private debt. Higher yields are a key motivation. Evergreen structures — funds without a fixed end date — ensure that capital largely remains invested.

De Groot adopts a more cautious stance. “It is not as though there are double-digit differences in returns,” he notes. “For investors, the key consideration is whether they understand and are willing to accept the illiquidity inherent in private markets.”

De Groot adopts a more cautious stance. “It is not as though there are double-digit differences in returns,” he notes. “For investors, the key consideration is whether they understand and are willing to accept the illiquidity inherent in private markets.”