A large share of the bond markets currently offers yields that look attractive, above the magical threshold of 4 percent. But the war in the Middle East is fueling fears that inflation could move in that direction as well, which would erode much of the real return.

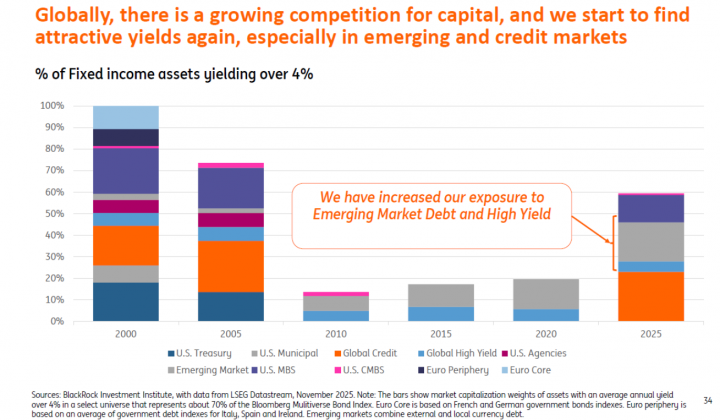

Vincent Juvyns, market strategist at the investment office of ING Belgium, points to a remarkable change in the bond markets compared with five, ten, or fifteen years ago: about 60 percent of the market capitalization in fixed income markets currently offers a yield of 4 percent or more. That has not been seen in twenty years. In 2020, barely 20 percent of the market climbed above a yield of 4 percent.

“Everyone always pays a lot of attention to the equity markets, but attractive returns are currently possible in the bond markets. That is especially the case for corporate bonds (investment grade and high yield) and debt from emerging markets. We are currently considering both high-yield bonds and emerging market debt.”

Psychological threshold

According to Juvyns, 4 percent is an important threshold in the minds of investors. In the summer of 2024 Belgian banks competed for the billions released from the government bond. ING Belgium therefore launched a time deposit offering 4 percent gross interest. Other banks had to follow. The investment office of ING is currently working on the development of a new product based on fixed income securities.

ING is not alone in its enthusiasm. “Bonds are back,” wrote the American asset manager Vanguard at the end of last year in its outlook for 2026, pointing out that returns for high-quality US securities are projected to come out at around 4 percent in the coming decade. “That offers a comfortable margin over expected future inflation.” That comment was written before the Israeli-American attack on Iran last weekend.

German asset manager Flossbach von Storch also launched an offensive bond fund last month, flagging bond high conviction. “Bond markets are once again attracting strong attention. Bonds are again generating attractive returns and are doing what they are supposed to do: offering relevant diversification for mixed investment portfolios,” the asset manager said in a note. Its new fund is mainly aimed at professional and institutional investors and family offices in Germany, Belgium, Luxembourg, Switzerland, Liechtenstein, Italy, and Spain.

“Whether a yield of 4 percent is truly ‘magical’ depends on inflation expectations, duration risk, and regulatory or mandate constraints.”

Lars Conrad, Flossbach von Storch

Is 4 percent also the magical number for those clients? “Four percent has often functioned as a psychological reference point for bond investors, especially after the long period of near-zero interest rates, because it represents a return that feels ‘meaningful’ in nominal terms and can compete with dividend yields or conservative assumptions for equity returns,” said Lars Conrad, portfolio director fixed income at Flossbach von Storch.

“For many institutional investors… a gross yield of 4 percent can indeed appear to be a minimum threshold return, because it may better align with liability discount rates and long-term return targets. That said, whether it is truly ‘magical’ depends on inflation expectations, duration risk, and regulatory or mandate constraints, rather than the number itself.”

Expected inflation

The US ten-year yield currently stands at 4 percent, while inflation there is about 2.4 percent. Until recently, most economists considered the chance small that US inflation would also rise to 4 percent, which would reduce the real interest rate to zero.

The war in the Middle East is changing the calculations. Strategists at Degroof Petercam this week referred to a study by the Dallas Federal Reserve during the tensions between Israel and Iran in June 2025. At the time, central bankers said that a closure of the Strait of Hormuz would push US inflation up by nearly 130 basis points. That would mean US inflation could climb toward 3.7 percent.

“Volatility in government bond yields is likely”

Lombard Odier

From a rapid de-escalation and a corresponding easing of oil markets to a brutal oil shock and stagflation, market players are taking different scenarios into account. It is also unclear to what extent central banks will adjust their interest rate policy. “Volatility in government bond yields is likely, as markets reassess their expectations regarding inflation, growth risks, and central bank interest rate responses,” analysts at Lombard Odier said in their reaction to the war.

“In a week or two, or three, there will probably be more clarity,” is a commonly heard prediction among economists and investment strategists. For now, the market is waiting for the dust to settle before new forecasts about real bond yields (nominal interest minus inflation) can be made.